By Nick Barisheff

Special to the Financial Independence Hub

Global stock markets suffered the worst first quarter in their history in 2020, as the COVID-19 pandemic rattled markets. After slowing 5% in the first three months of 2020, the U.S. economy shrank by a whopping 33% in the second quarter. If you think these numbers are bad, it is only going to get worse. The second wave of the pandemic is forcing governments around the world to renew lockdown measures that will push the U.S. economy, and most western economies, to the brink.

Chaotic elections, a battered economy

This is all happening at a time when the U.S. just conducted the most chaotic presidential election in its history in November. Rioting and civil insurrection are occurring in U.S. cities, and crime is accelerating. Lawsuits over mail-in ballots have already started across the country. What’s more, the nomination of Amy Coney Barrett as successor to Ruth Bader Ginsburg promises to be hotly contested, as the choice of nominee will have huge implications following the election. If the election result is disputed [as it was within days of the November 3rd vote: editor] the U.S. Supreme Court may end up deciding whether Trump or Biden will be president for the next four years.

If the global pandemic, civil unrest in many U.S. cities, war looming in Armenia, thus pulling Russia, NATO and the European Union into a conflict were not enough, the U.S. economy, as well as most western economies — including Canada’s – are going to get a whole lot worse.

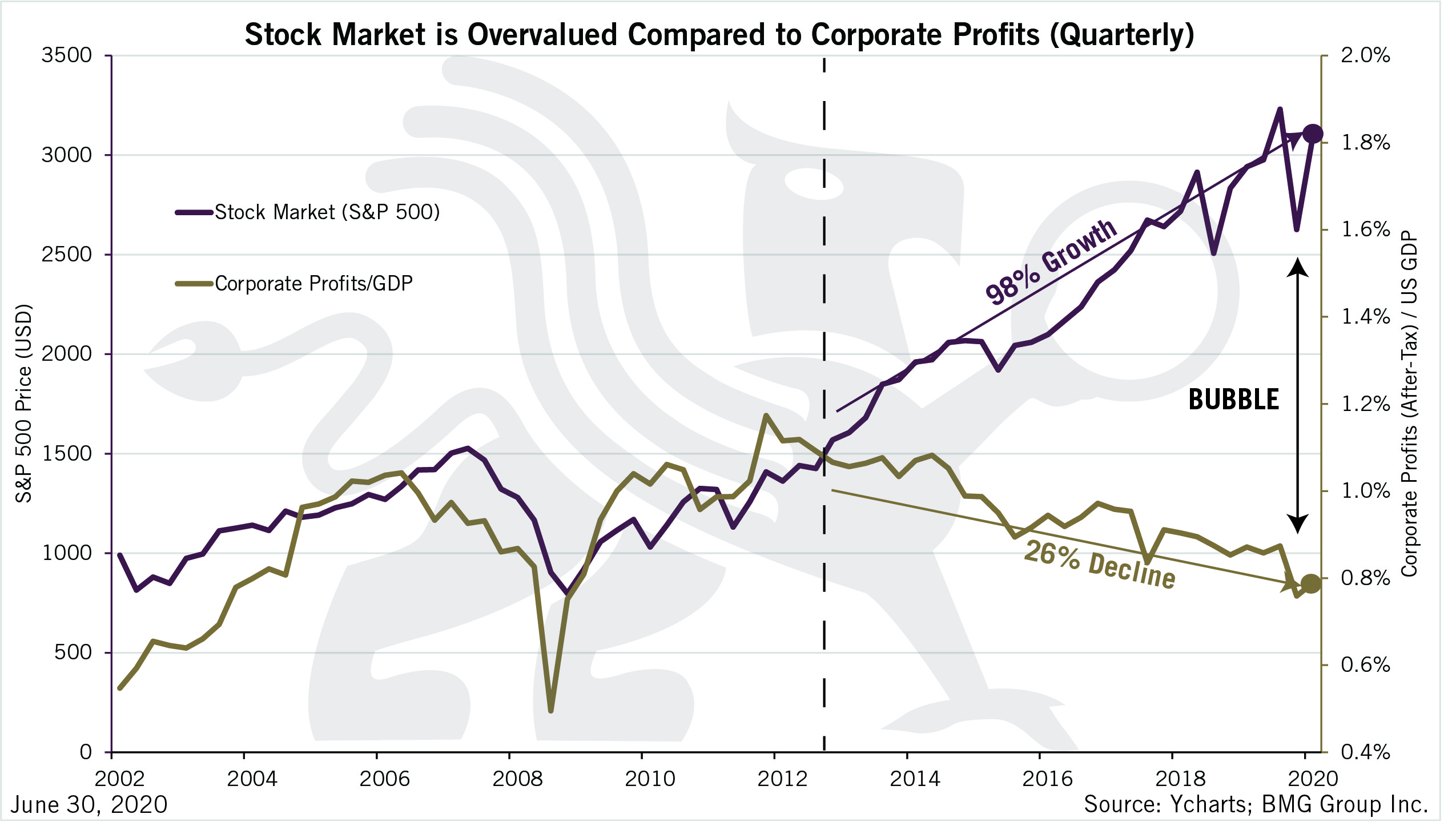

Overvalued markets, declining corporate profits

U.S. equity markets and corporate profits were already on a divergent path well before COVID-19 hit, and this trend will only continue – especially if the second wave forces more closures and lockdowns in the fall and winter. Restaurants, hotels, travel and tourism, airlines, and small businesses across the country are barely hanging on. Bankruptcies are set to skyrocket.

Coming defaults in the real estate sector

One of the biggest economic issues — one that hasn’t received a lot of attention — is the wave of defaults that will hit all areas of the real estate sector. Financial districts of major cities are ghost towns. It’s just a matter of time before large tenants terminate or default on their leases. Developers are stuck in a rut, as demand has collapsed.

Mortgage defaults and collapsing real estate markets will in turn lead to problems in the banking sector. In fact, mortgage delinquency rates in the U.S. climbed to 8.2% at the end of June – the highest level since 2011. More than 8% of all U.S. mortgages were past due or in foreclosure.

To keep the economy from collapsing, the U.S. Federal Reserve and other western central banks are going to have to print even more money, which will only exacerbate the bubbles in the financial markets and margin debt levels. What’s most worrisome is that all these factors — declining markets, a shrinking economy, and the second wave of the pandemic — are morphing together just as the U.S. is about to face one of the most chaotic presidential elections in history.

How should investors proceed?

What are investors to do? If you listen to the media or those in the industry, the mantra is to stay invested for the long term. That strategy works well during long bull markets. However, this strategy doesn’t make sense when you’re standing on the edge of a precipice — which we are today. Continue Reading…