By Dale Roberts, CutTheCrap Investing

Special to the Financial Independence Hub

Data shows that Canadians continue to embrace low-cost ETFs. That said, more monies continue to flow into high-fee mutual funds. As you likely know, Canadians pay the highest mutual fund fees in the developed world. Of course, those high fees are wealth destroyers and can eat up 50% of your investment returns over the decades.

But here’s the good news: more Canadians are moving more monies to low-cost ETF portfolios by the way of self-directing or through Canadian Robo Advisors or by way of those One Ticket Asset Allocation Portfolios.

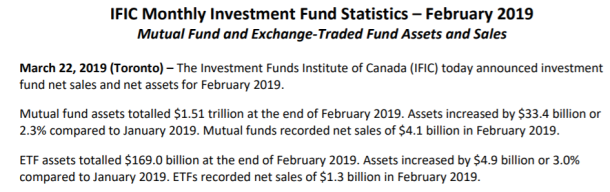

Here’s a look at the flow comparisons for Mutual Funds and ETFs courtesy of the IFIC site:

Here’s the sales figures for mutual funds in what we would typically call the usually robust RRSP season, January and February:

And here’s the sales figures for the ETF industry for RRSP season:

And here’s the sales figures for the ETF industry for RRSP season:

If we want to be optimists, that is more than promising. While 2019 was a soft RRSP season for money flows into mutual funds and ETFs (compared to 2018 figures) there was an acceleration of flows to ETFs compared to mutual funds, year over year.

- In 2019 35% of new monies went to ETFs.

- In 2018 27% of new monies went to ETFs

That is certainly something to celebrate. While the total mutual fund industry is almost 10 times the size of the ETF industry, they did not even double the size of inflows for January and February of 2019. That aligns with the findings of Nest Wealth, which conducted a poll in RRSP season. Respondents suggested one third of all new account openings would be by way of one of the Canadian Robo Advisors: also known as digital wealth managers. For more on that please have a read of There will be a tipping point for ‘Robo Advisors’ suggests Randy Cass of Nest Wealth. Keep in mind the poll was reading account openings, not the move of assets or amounts of assets.

Here’s another way to frame that more than ‘good news’. Continue Reading…