ETFs aim to provide broad market exposure with low cost and our Best ETFs for Canadian Investors advisory covers ETFs like no other publication in North America.

Notably, we recently released our top ETF to buy in 2024 in this newsletter. However, you’ll need to subscribe to find out what that top ETF to buy in 2024 is!

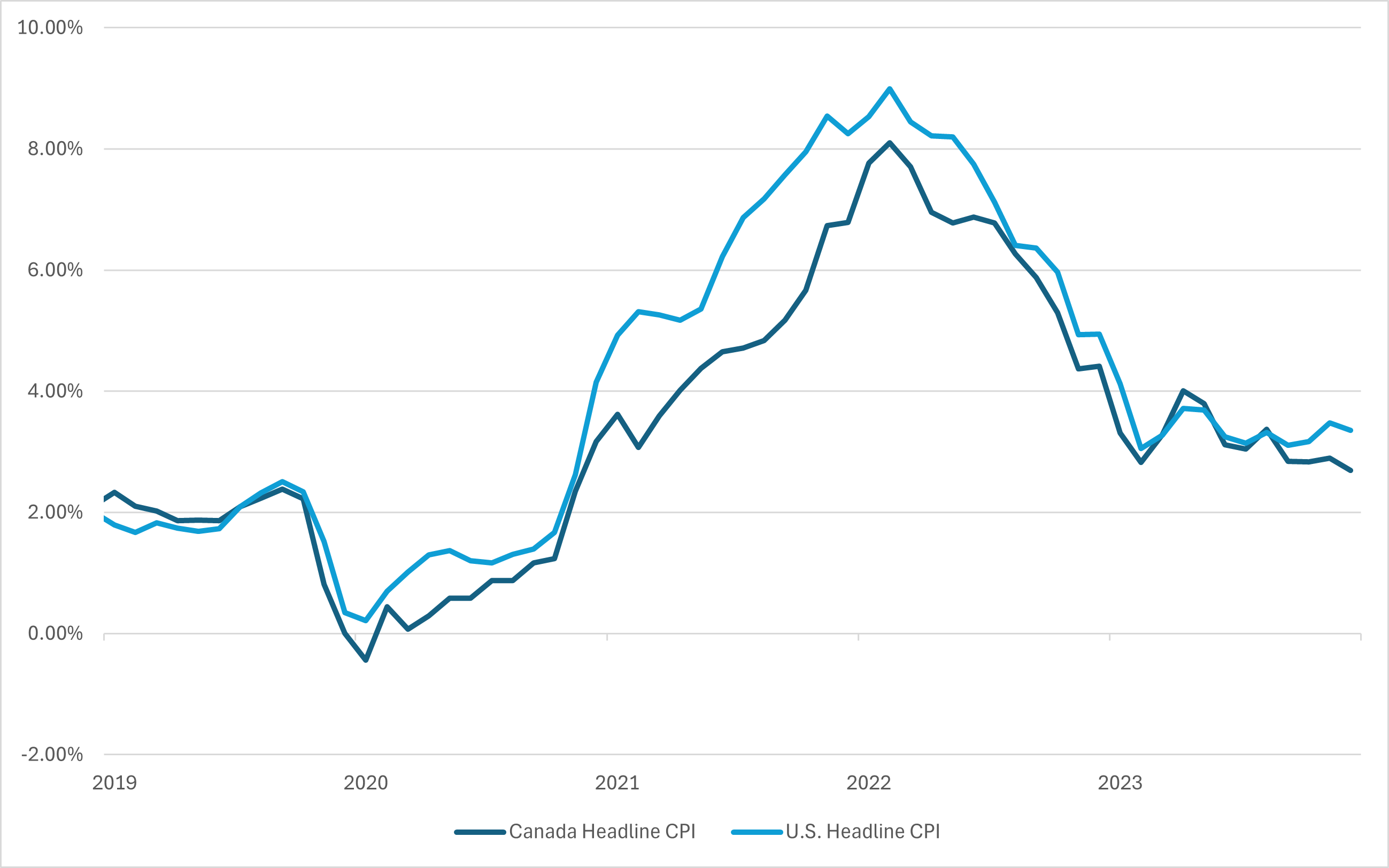

This ETF offers a solid 1.4% yield, while at the same time charging you a very low 0.0945% MER. Going forward, the fund — and its investors — should gain from an expanding U.S. economy. Plus, the ETF’s U.S. dollar exposure provides valuable currency diversification for Canadian investors; that’s a long-term positive.

When it comes to ETFs, we take a close look at the following criteria:

6 Important considerations for choosing ETFs to invest in:

- Know how broad the ETF’s stock holdings are, so you can determine its volatility. The broader the ETF, the less volatility it may have. A sector-based ETF, like one that tracks resource stocks, may be more volatile.

- Know the economic stability of countries that an international ETF invests in. It’s also worth mentioning that foreign leaders may not be your ally when it comes to passing laws or imposing regulations that can affect your investments

- Know the liquidity of ETFs you invest in; look at the volume of shares that trade hands on a daily basis.

- Consider buying ETFs in a lump sum rather than with periodic small amounts, so you can cut down on brokerage fees.

- ETFs can still be volatile, even with the diversification they offer.

- Don’t invest in ETFs that show wide disparities between the stocks they hold and the investments that the sales literature describes. Despite the increased attention for ETFs, many ETF managers continue to describe their investing style in vague (or sometimes misleading) terms.

Meanwhile, rather than using the six criteria above, some investors decide when to buy an ETF using technical analysis.

Technical analysis is a useful tool in deciding when to buy ETFs, but only if you recognize it as one of many tools. Before making any recommendations or transactions in client accounts, I always look at a chart. However, I don’t look at the chart for a prediction of what’s going to happen. I look to see if the pattern on the chart seems to support the view I’ve formed of the stock/ETF based on its finances and other fundamental factors. Continue Reading…