By Jordan McCaleb

Special to Financial Independence Hub

Financial Independence (aka Findependence) is a dream many hope to achieve, the freedom to live the life you’ve always dreamed of, pursuing passions or simply choosing to work on your own terms. While these are all great reasons, what about achieving this earlier?

This article will explore key investment strategies and asset allocations to accelerate your path to early financial freedom, including the role of precious metals investments.

Traditional Investments & their Limits

It’s important to acknowledge that traditional investments (stocks, bonds, mutual funds, and ETFs) will always be the building blocks when it comes to financial independence.

However, when it comes to achieving Findependence earlier in life, traditional investments may have potential limitations and risks involved.

Potential Limitations and Risks:

- Inflation: Inflation erodes the real value of your accumulated savings over time.

- Market Volatility: Unpredictable swings and downturns can threaten your gains and potentially delay your FI (financial independence) timeline.

- Economic Uncertainty: Geopolitical risks and unforeseen crises can increase risk and cause market corrections, impacting even the safest portfolio.

While traditional investments form a crucial base for any Findependence strategy, they may not be enough to achieve the resilience and growth required. Achieving financial independence early requires specific and powerful assets to drive your portfolio, providing a balance to your financial ecosystem.

Accelerating your FI Timeline: Beyond just Investing

Accelerating your Findependence timeline requires additional steps. A crucial part is increasing your savings rate, aiming for 50% to 75% of your income, creating a powerful snowball effect that reduces your time horizon. This pairs with increasing your income through career advancement, salary raises, or profitable side hustles.

Simultaneously, optimizing expenses and embracing a frugal lifestyle in areas like housing, transportation, and food can further boost investment growth over time. A key step is defining your (FI Number) typically 25 times your desired annual expenses ($50,000). This lifestyle-specific figure provides a clear target.

Diversifying for Resilience: Beyond the Basics

Beyond traditional investments and accelerating your timeline, diversification involves not just different stocks, but asset classes as well (equities, fixed income, real estate, and alternatives). Each behaves differently under various economic challenges. Diversifying across geographies and industries can protect against downturns in a market or sector.

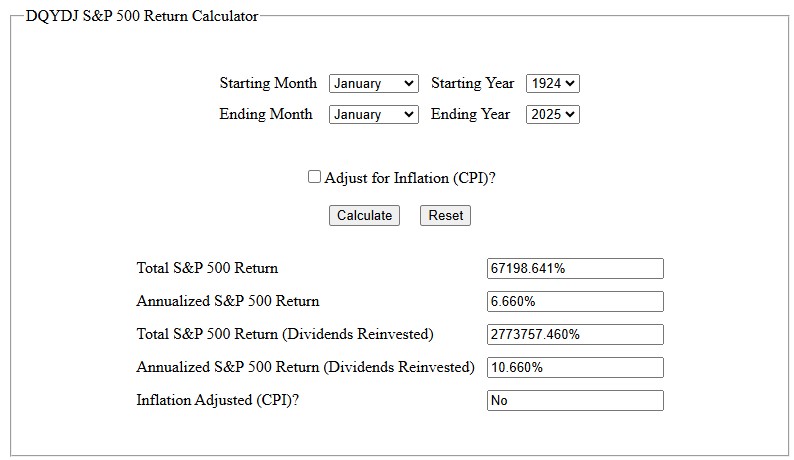

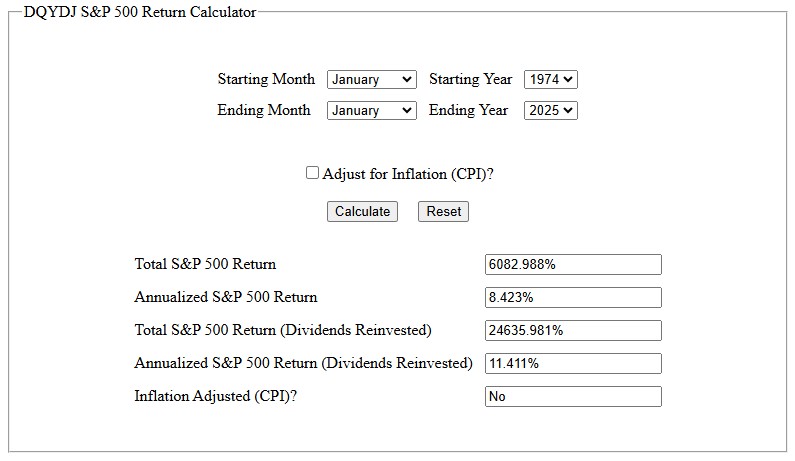

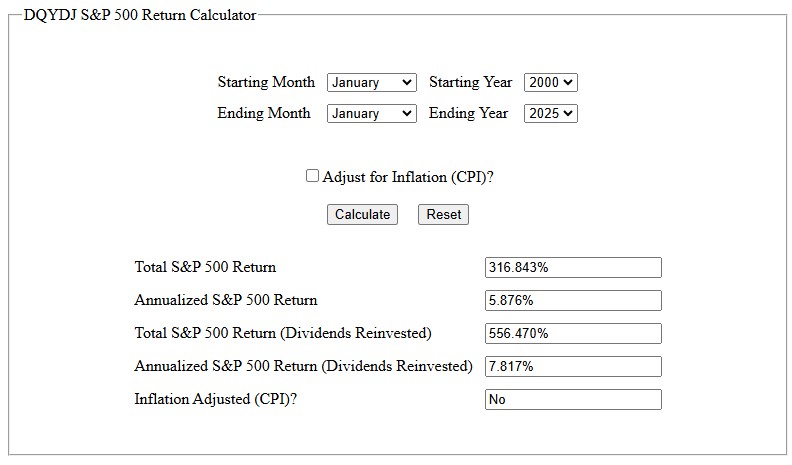

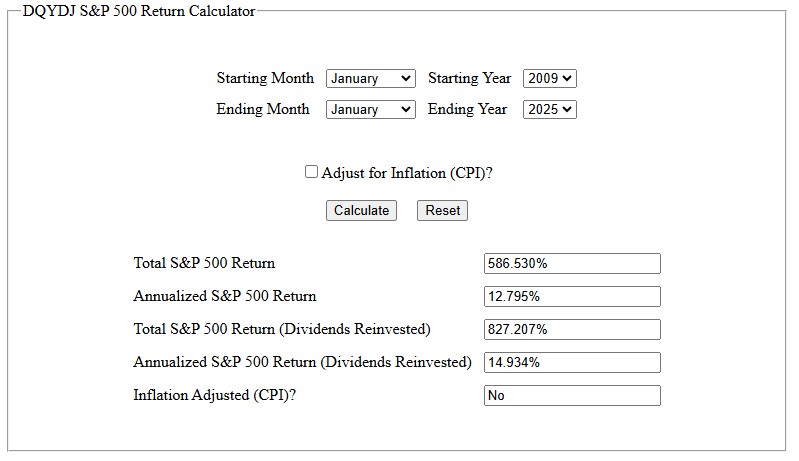

A crucial concept to know is asset correlation: You want your assets to not run in the same direction. According to Stock Rover, this reduction in volatility can significantly impact overall returns. For example, a portfolio experiencing wild swings of +20% then -20% loses money, while reducing it to +10% then -10% swings leads to a healthier outcome. In essence, a low correlation portfolio better withstands economic turbulence.

Strategic Allocation: The Role of Precious Metals

When aiming for early Findependence, strategic alternative assets are crucial. Gold and silver stand out as a hedge against inflation and economic uncertainty due to their low correlation nature. Historical data from Investopedia reveals that while the S&P 500 dropped almost 10% (2007-2010) during the 2008 financial crisis, a 1971 gold investment significantly increased in value. Gold IRAs also offer tax advantages for those interested in physical metals. Continue Reading…