Franklin Templeton’s Investment Outlook for 2026 and beyond was largely positive, judging by the three speakers who presented to advisors and the media at Toronto’s Ritz Carleton Hotel on Tuesday (Nov. 25). In fact, UK-based Global Investment Strategist Michael Browne declared the year now closing, 2025, to be “the Year that the Bear cried Wolf.”

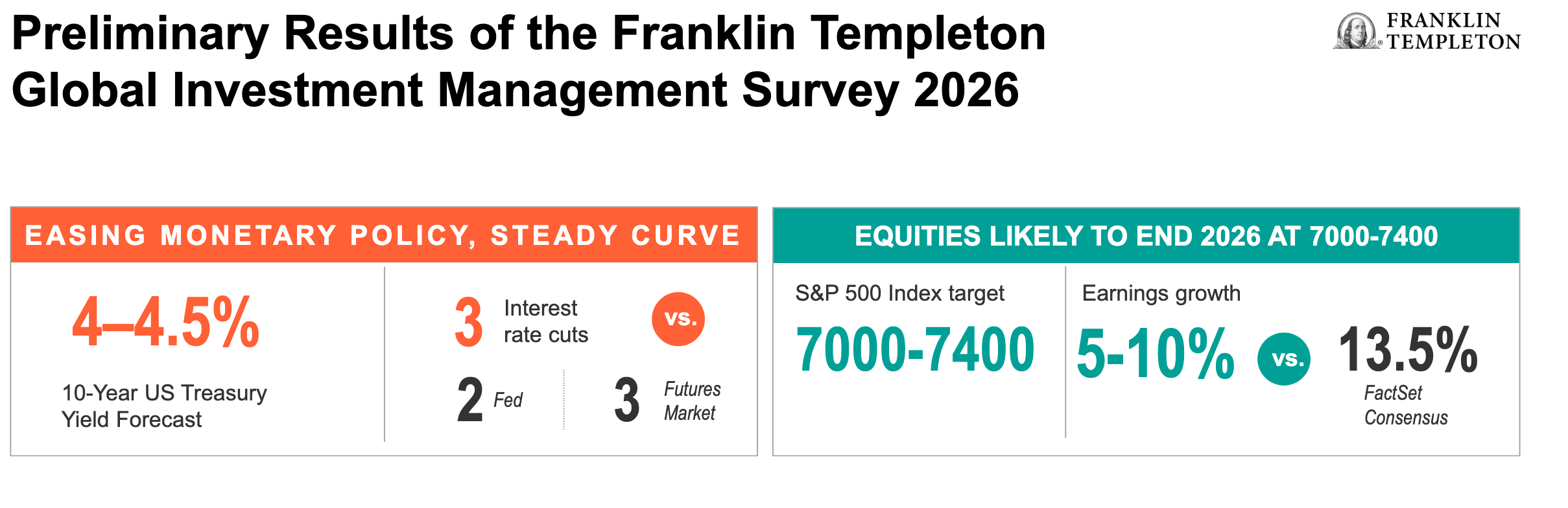

Browne, who is with the Franklin Templeton Institute, released the following preliminary results of Franklin Templeton’s Global Investment Management Survey 2026, shown below:

Browne expects three Fed rate cuts next year and foresees U.S. equities as measured by the S&P500 to end as high as 7400 by the end of 2026.

Like other Templeton executives, Browne expects to see rises in stocks outside the United States. This year, the story has been about growth in the U.S. market and Value in the rest of the world, he said. But even though there are no “Magnificent 7” stocks in Europe or the Emerging Markets — the Mag 7 and their innovation mindset seem unique to the U.S. — he expects a widening and broadening of global markets, with “opportunities in all asset classes.” He expects earnings growth of 5 to 10%, somewhat below the 13.5% Factset consensus.

Corporate margins keep rising, housing markets are weak, and the High-Yield Default Rate is near historically low levels, Browne said, with slides illustrating each point: “Stress indicators do not

point to a severe default cycle in the near term.”

However, Tariff revenue for the U.S. is “unfortunately” high, he said.

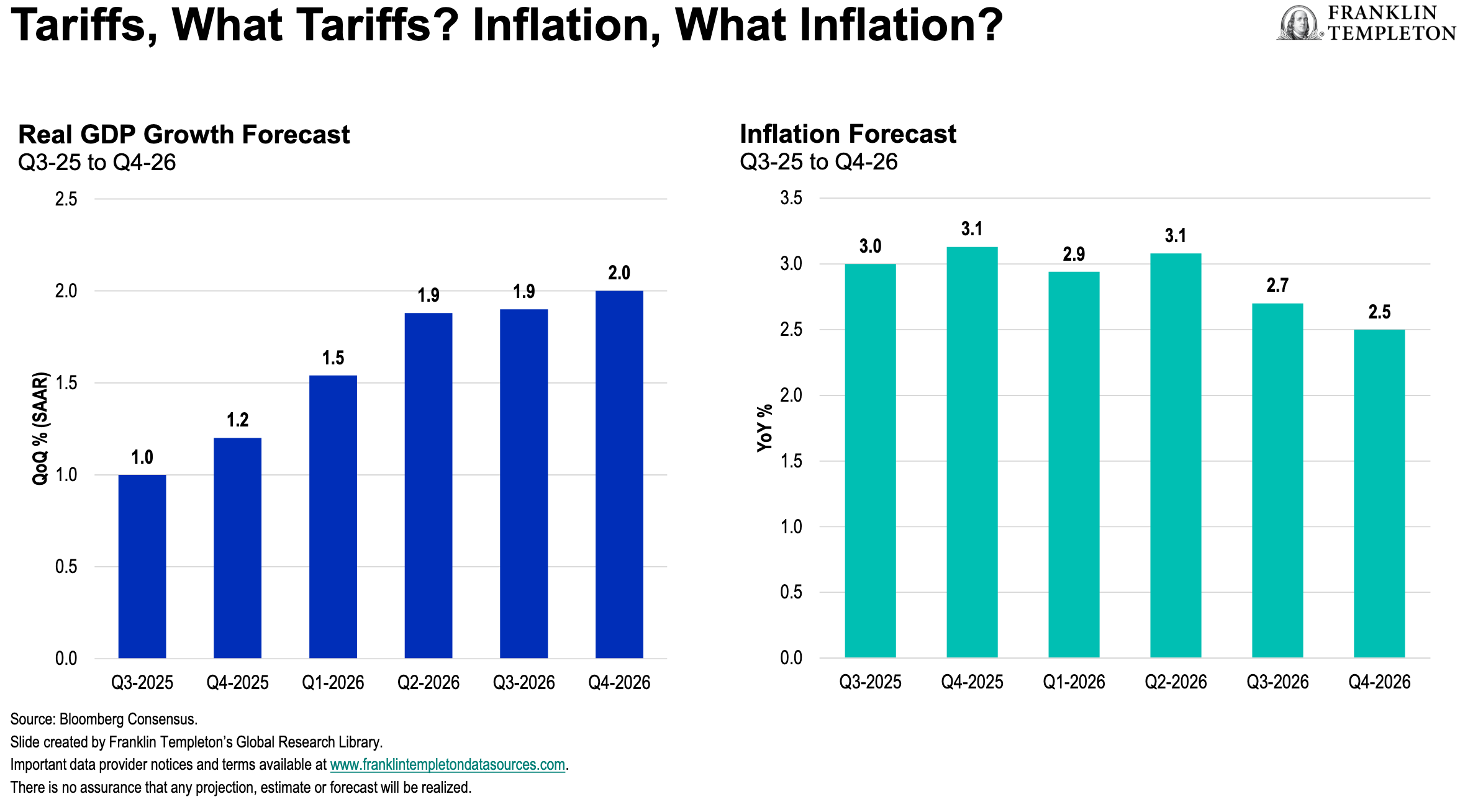

Even so, as the chart below demonstrates, real GDP (Gross Domestic Product) is forecast to rise over 2026 and inflation is expected to be flat to down next year.

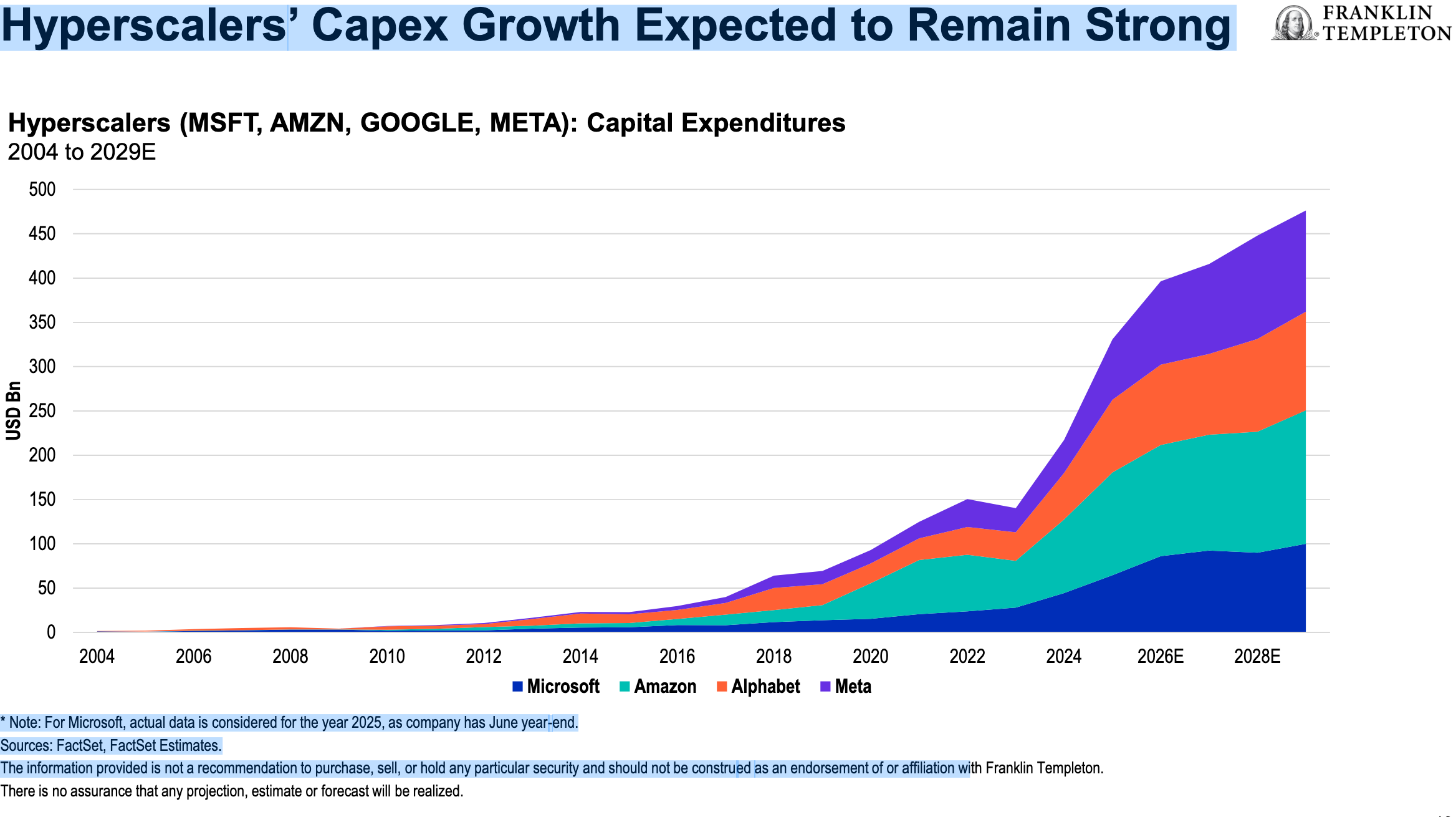

Meanwhile, there is more than US$7 trillion in cash still sitting on the sidelines and capex growth for the big hyperscalers is expected to remain strong, Browne said. They will spend US$3 trillion by the end of the decade and may generate significant returns for the four hyperscalers investing from Cash: Meta, Microsoft, Amazon and Google.

How to spot a Bubble … and a Crash

Browne provided past examples of historic bubbles, ranging from Dutch Tulipmania of 1637 to the American railway mania of the early 1850s, which crashed in 1873, and severe stock market declines in 1907, 1929, 1987, 2001 and 2008.

Bubbles usually end after 7 developments: Debt, Rate rises, a “First Failure,” Confidence fails Reverse Velocity, Margin Calls, Forced or Panic Selling and finally Fraud.

Comparing the 2020s to the 1990s, one of Browne’s slides said “The dot-com bubble burst in 2000: more than five years after the release of Netscape.”

Historically, Global Equities have delivered double-digit gains following Rate cuts and have supported P/E expansions, Browne said. All markets except China are more correlated to the U.S. than in the past. In Emerging Markets, Browne likes India and China: “When the Fed cuts, Emerging Markets fly.”

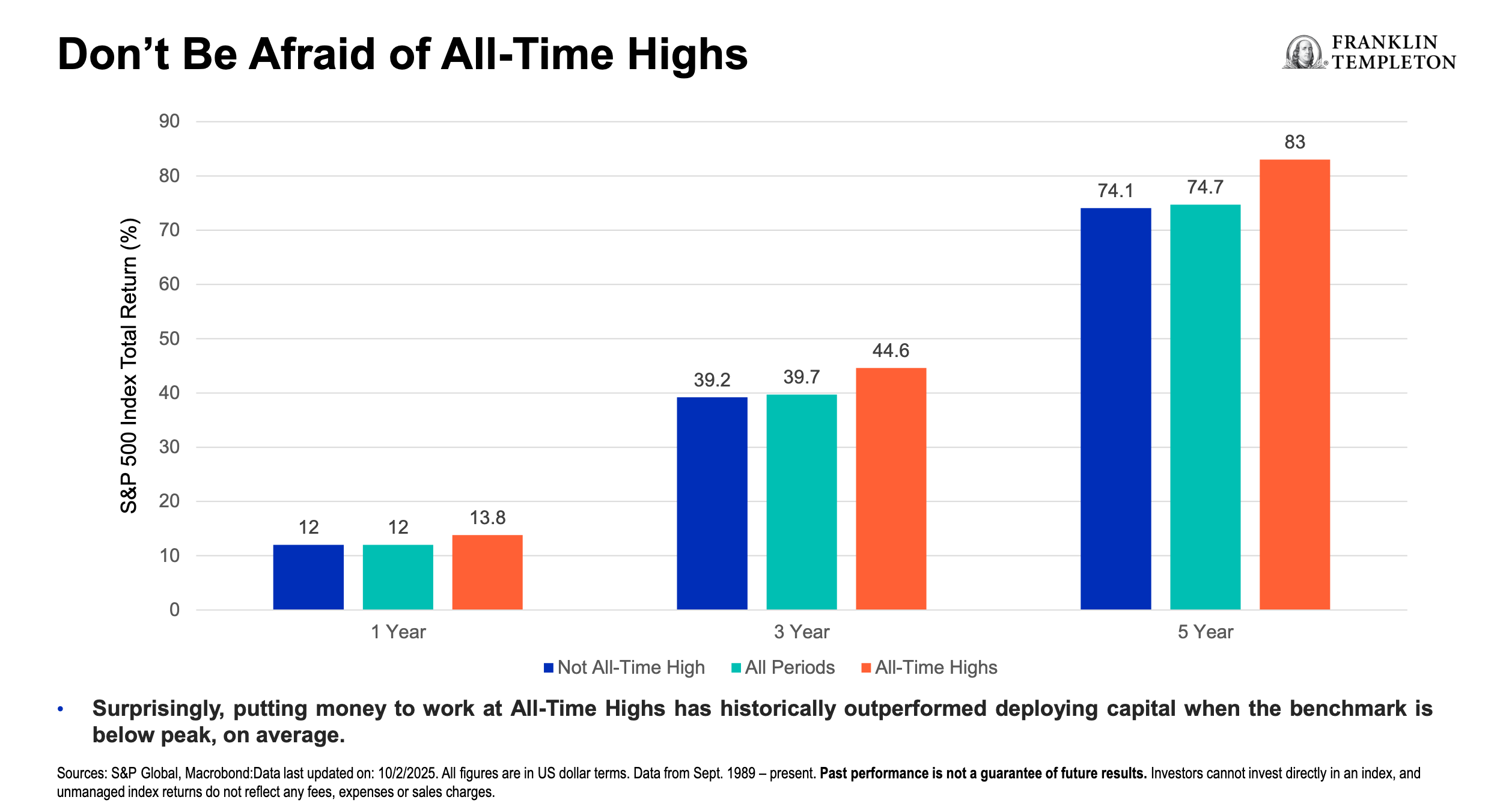

The last scheduled speaker was Jeff Schulze, CFA, Managing Director and Head of Economic and Market Strategy for ClearBridge Investments, who reassured attendees they don’t need to fear the All-Time Highs the U.S. has been experiencing throughout much of 2025:

Schulze says that with possible Tariff Refunds, “we think the economy next year will outperform consensus expectations … We’re buyers of Dips.” While valuations are “full” right now, with the Fed cutting we don’t see multiples going down … for the first time in a long time, diversification will be more additive as we see a broadening out.” The previous laggards will become leaders, including small- and mid- caps and the S&P493 (all but the Mag 7).

One slide on the Tariffs said this: “The Supreme Court may decide that the administration’s IEEPA tariffs need to be refunded, which would be a windfall to corporate America next year. Secretary of the Treasury Scott Bessent has noted that approximately half of the incremental tariff revenue, which is on pace to near $200 billion by year-end, has come from IEEPA tariffs.”

Schulze closed with an upbeat assessment of the U.S. stock market: “The S&P 500 has continued to march higher with earnings expectations inflecting higher during 3Q. Although U.S. equities may need a period of digestion following a robust rally off the April lows, historical rallies of similar

magnitude and duration have given way to continued upside over the subsequent 12 months.

Market leadership has been a tug-of-war in 2025 from a regional and style perspective. We believe this dynamic may continue before giving way to a period of international and value outperformance.”

While Schulze largely focused on prospects for the coming year, another speaker tried to look out for the next ten years: Michael Greenberg, CFA, CAIA, Senior Vice President Head of Americas Portfolio Management for Franklin Templeton Investment Solutions.

“We think Growth is slowing but remains generally robust,” Greenberg said, and this will be enhanced by Technology and massive fiscal spending. That may be inflationary but will be fairly anchored and counteracted by productivity, demographics and technology. He expects growth in the rest of the world to catch up to the U.S.

On Asset Allocation, despite the optimism about Stocks, Greenberg said Fixed Income should remain an important part of portfolios and “we also need other asset classes.” While he doesn’t necessarily expect deglobalization he foresees “less globalization and more regionalization … We will see trade blocs being less exposed to the U.S. and the US dollar; we’re seeing the U.S. weaponize currency a bit.” While the U.S. dollar remains dominant in global reserves, the chart below demonstrates that over the last two and a bit decades, the U.S. dollar share has fallen from 72% to 56%:

Moving to Asset Allocation, Greenberg said AI and Technology investment remains a key theme. Despite the increasing characterization as being a bubble, the long-term capital investment spending will provide “real tangible benefits on productivity.” Canada and Europe are a bit more challenged than the U.S. in this regard but as productivity increases because of A.I. and Robotics, workers will be able to do more with less, which will unlock lower-valued markets like Europe and the Emerging Markets, Greenberg said.

But it’s not all rosy: one downside will be the displacement of “hundreds of millions” of workers, as the chart below shows:

All this has major implications for Asset Allocation. Equities remain key for real long-term growth, Greenberg said, and will continue to serve as a “pretty good inflation hedge.”

While Greenberg and other managers are not suggesting investors abandon U.S. stocks, over the long run he sees reducing U.S. exposure for those who are overexposed to it, and look more to Europe, Emerging Markets and “even Canada.” He showed year-to-date returns in Canada, the U.S. and EAFE in the chart below. As you can see the aquamarine bars show the best returns in each region: materials in Canada (chiefly Gold miners), the Mag 7 in the U.S. and Financials in EAFE:

Finally, Greenberg closed by reminding attendees that traditional multi-asset portfolios are far from dead. The traditional 60/40 stocks/bond mix continues to provide reasonable returns at reasonable risk but “it makes sense to evolve the 60/40.” Equity will still be relied upon for growth but this can be diversified beyond just the U.S. into the rest of the world, including Canada. Fixed income can still be relied upon for income and act as a recession hedge in case of growth shocks. Some investors could add private investments, infrastructure, real estate and real assets, keeping in mind liquidity and manager selection.

Greenberg’s formal presentation included the chart below on multi-asset allocation over the last 30 years, which illustrates the continued dominance of U.S. stock returns. 60/40 is illustrated in Red and is roughly in the middle of the pack. He closed by reminding investors the world is changing and they should not go overboard on any one theme, country or asset class.