By Mark Seed, myownadvisor

Special to Financial Independence Hub

It has been said bonds make bad times better.

Is this the reason to own bonds?

Welcome to another Then and Now post, a continuation of my series where I revisit some older blogposts and either rip them to shreds (because my thinking has totally changed on such subjects) or I’ll confirm my position on various personal finance topics or specific stock and ETF investments.

Since my last Then and Now post (whereby I shared I sold out of all Johnson & Johnson (JNJ) stock to buy other equities in recent years), I figured it might be interesting to review this post and update my thinking from a few years ago before the pandemic hit – on bonds.

Then – on bonds

Back in 2015 when the original post was shared, I referenced this quote that frames my own portfolio management approach when it comes to my bias to owning stocks over bonds:

“If you want to make the most money, you should invest in stocks. But if you want to keep the money you made in stocks, you should invest in bonds.” – Paul Merriman.

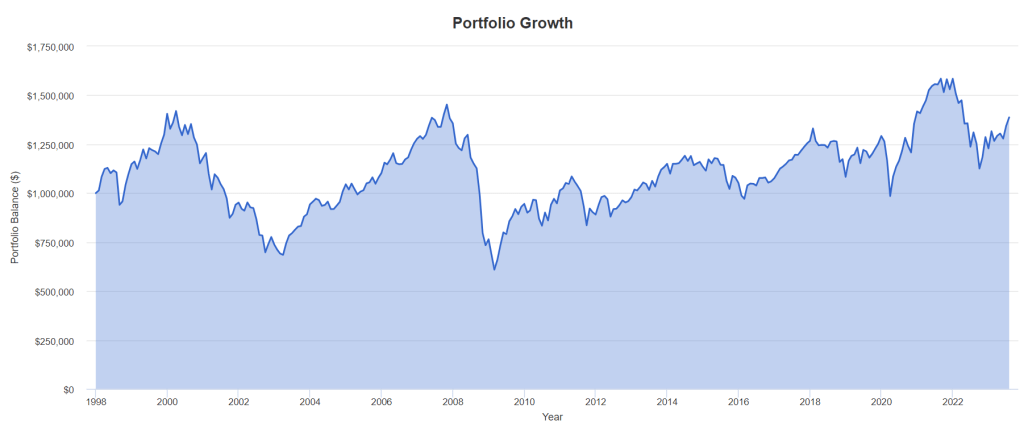

Bonds are essentially parachutes when equity markets fall; bonds will cushion the portfolio landing. And equity markets can fail big at times!

While I understand there are different ways to measure the “equity risk premium,” the summary IMO is the same: the risk premium is the measure of the additional return that investors demand or expect for taking on a particular kind of risk, relative to some alternative.

Buy a bond and hold it until it matures and you know what you will get back.

Invest in equities and the range of outcomes is wide.

With equities, you could make a lot of money, but you could lose a lot.

Equities have to have a higher expected return to compensate investors for taking on this risk.

Otherwise, if the risk premium is not there – why bother with stocks at all?

Now – on bonds

That’s the rub these days, for many investors. Why invest in stocks when interest rates are higher and you can earn 4-5% essentially risk-free?

Of course, there is no way of knowing how equities or bonds will perform until returns for each happen. You can consider rebalancing your portfolio from time to time between stocks and bonds because you expect equities will do better longer-term but that doesn’t mean they will short-term.

Which brings me back to this: risk is the price of the entry ticket to buy and hold stocks. Continue Reading…