Discover the Keys to Identifying Dividend ETFs that offer Consistency, Quality, and Long-Term Growth

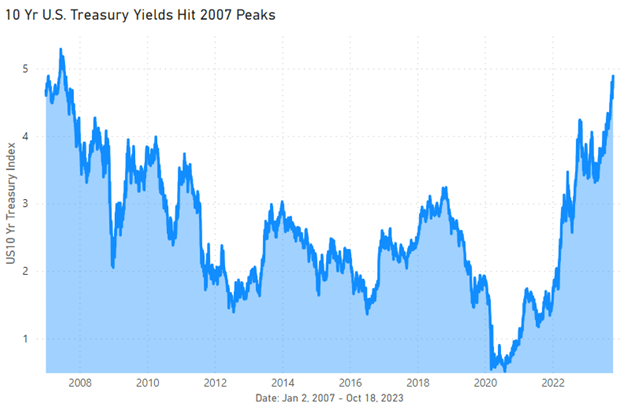

Higher interest rates mean dividend-paying stocks must increasingly compete with fixed-income investments for investor interest. However, sustainable dividends still offer an

attractive and growing income stream for investors.

Companies that pay regular and growing dividends have performed very well over the long run when compared to the broad market indices. For example, a simple strategy such as selecting stocks with an extended history of uninterrupted dividend growth, such as represented by the S&P 500 Dividend Aristocrats, has added 11.5% per year over the past 30 years. This compares to the 10.0% annual gain for the S&P 500 Index. And not only did the dividend payers beat the overall market, but they were also less volatile.

The superior long-term performance of the dividend growth companies can be attributed to a combination of several factors: Companies with long histories of regular and growing dividend payments generally have sound competitive business models and growing profits; these are also companies with experienced managements that make disciplined capital allocation decisions, strive for lower debt levels, and operate firms more profitable than their peers.

Notably, though, the Dividend Aristocrats’ performance lagged over the past 5 years against the S&P 500 index.

Most of this underperformance came over the last year and a half, as higher interest rates made fixed-income investments, such as GICs, more attractive for income-seeking investors when compared to dividend-paying equities.

The dividend sweet spot

Income-seeking investors who decide to take on the risk of the stock markets are faced with a wide range of options including “yield enhanced” dividend-paying ETFs, moderate-yielding companies with average growth rates, and low-yielding but fast-growing companies. Then there is also the group of companies that have very high dividend yields and may seem attractive but, unfortunately, come with elevated risk.

In many cases, a high yield may be a warning sign that all is not well with a company and that future dividend payments are at risk of being cut.

As well, a dividend cut, or even an outright dividend suspension, is often accompanied by a steep decline in the share price, as income investors dump their former dividend favourites.

A 2016 study by a group of U.S.-based academics provides some statistical guidelines for sensible dividend-based investing.

In reviewing the performance of almost 4,000 U.S. companies over 50 years, they found that dividend-paying stocks beat non-dividend payers.

In particular, the middle group of dividend yielders (i.e., those with an average yield of 4.3%) surpassed both the low yielders and the high yielders in terms of total return. Equally important, this superior performance was achieved with lower risk, as measured by the standard deviation of returns.

Based on this long-term study, it makes sense to avoid the highest-yielding stocks and rather look for companies with moderate yields and sound growth prospects. This safety-first approach will result in a lower yield but likely provide a better total return (dividends plus capital) at lower risk.

How to spot dividend ETFs worth investing in

When investing in dividend-paying companies through an ETF, here are key factors to consider: Continue Reading…