Despite all of the evidence that low-cost passive investing outperforms actively managed portfolios, many investors still cling to the belief that an active approach can help steer them through turbulent times in the market.

Even investors who have taken the plunge into index funds and ETFs can’t help themselves when faced with uncertainty. Emotions take over, as do our instincts to tinker with our investments to try and optimize performance.

Despite Dan’s best efforts to explain that these new and simplified portfolios should be used as part of a long-term investment strategy, the overwhelming number of comments from readers suggests that it’s nearly impossible for indexers to simply set-it and forget it.

The preamble to the 3.5-minute video observes that If you have invested for any length of time, you will have heard the expression “Past results are not an indication of future performance.” The best minds in the investment industry not only agree with that but some feel that in the coming years we should prepare ourselves for lower returns than we are used to.

The corollary to this is that If the markets are indeed prepared to not be as generous, then keeping fees as low as possible has never been more important. We need to keep as much of the overall return as possible. Continue Reading…

The fifth video instalment in SensibleInvesting.TV’s How to Win the Loser’s Game has been posted here and at Findependence.TV.

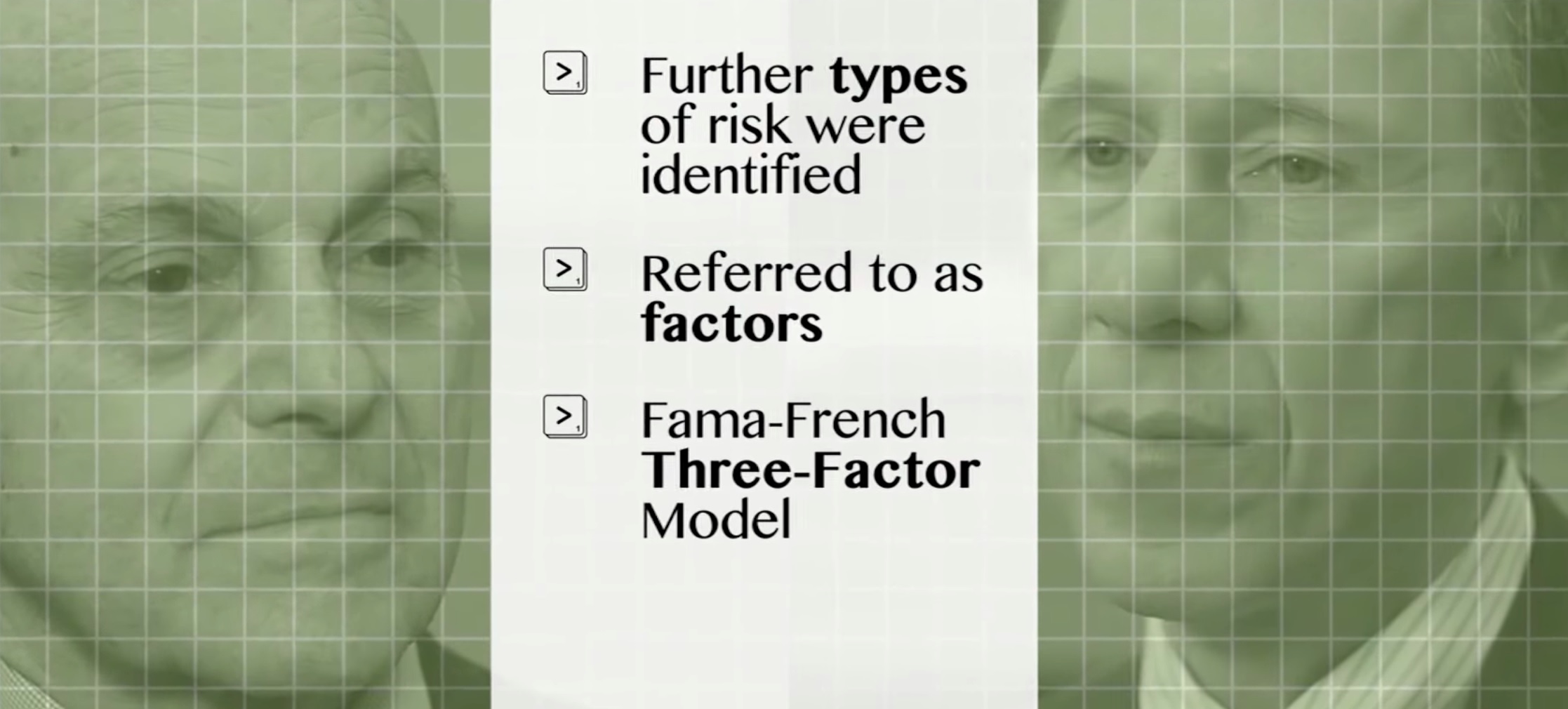

Often we hear say someone ask us the question, “Do you play the market?” The answer should be a resounding no, as the market is not a game. In fact, it’s quite scientific. A trio of Nobel Prize winning economists each have created a model that better helps us to understand the science behind the market.

This 8-and-a-half minute video features interviews with various executives from DFA and Vanguard and reviews the groundbreaking academic research on modern portfolio theory spearheaded by Harry Markowitz, William F. Sharpe and Eugene Fama. The screen shot above shows Eugene Fama on the left and DFA board member Ken French on the right. Continue Reading…

The three-and-a-half minute video covers what may be familiar ground to seasoned investors: timing the market and trying to get in or out of stocks in an attempt to avoid the next crash is usually a futile activity.

When we launched Wealthsimple 12 months ago, investors in Canada had just two options to manage their money: Do it yourself or hire an advisor.

Doing it yourself is low cost, but overwhelming for most investors. It requires a level of knowledge, interest, and confidence to manage your life savings completely solo. Hiring an advisor is easy, but can be expensive and intimidating, even if you have a large enough balance to meet high account minimums.

At Wealthsimple, we’re building a third category: automated investing with on-demand advice. This new category combines the low costs of doing it yourself (DIY) with the real advice and sophisticated approach of a full-service advisor. We built cutting-edge technology to automate a passive investing approach and digitize the entire account opening and reporting experience. It’s convenient, allowing customers to open an investment account in 10 minutes, with no paperwork or branch visits required. And it’s not just robo-investing or robo-advice, it’s real advice delivered by real Portfolio Managers by phone, email, video chat, or text message.

So who uses an automated investment solution? Definitely not your average investor!.

What an automated investment client looks like

In an industry where 90% of clients are over 50 years old, clients of automated investment services are almost half that age. The average Wealthsimple client is a first-time investor, just starting to put money aside for both short and long-term goals. Our clients range from 19 to 89, but 80% are under 40 years old and the average is under 30.Continue Reading…