Over the past few years, as hundreds of billions of dollars has flowed out of equity mutual funds and into exchange-traded funds (ETFs), a great migration of assets has been under way in the asset management business. This is occurring because of the changing business models of advisors and brokers-dealers and because of the unique benefits that ETFs can bring to investors, including relatively lower fees1, transparency of holdings, intraday liquidity and the potential for greater tax efficiency.

In many cases, “low-cost beta” ETFs, which track broad indexes, have outperformed the vast majority of active managers over time.2 This has made the decision to move assets from actively managed mutual funds into ETFs not just a decision based on cost, but also one based on performance.

But investors making this migration today have a choice that goes beyond just low-cost beta. For the past 10 years, WisdomTree has been showing investors ways to generate “low-cost alpha” in the form of fundamentally weighted ETFs that provide broad market exposure but that rebalance equity markets based on income, not market value. In recent years, other ETF managers have followed similar paths, creating narrower exposures that seek to tap into return premiums such as value, size, quality, momentum or low volatility—all of which have been associated with generating excess returns versus the market over time.

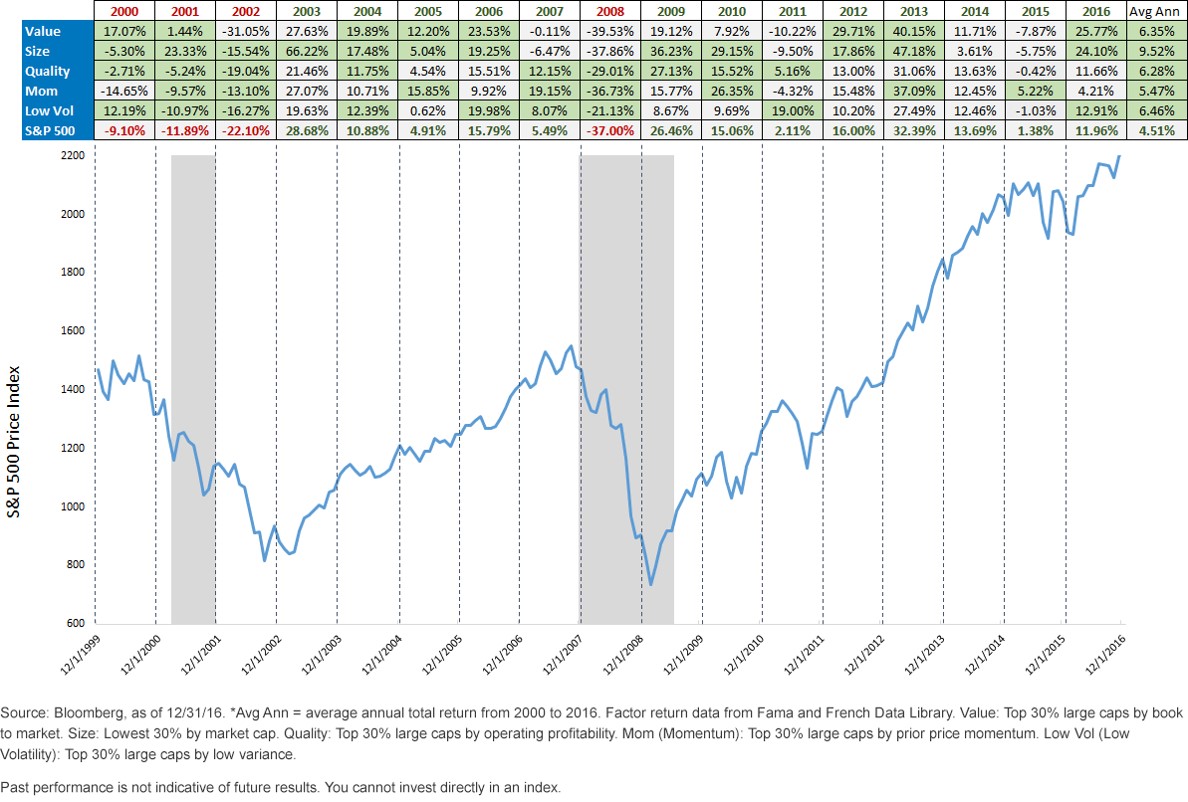

In the table above, we show how portfolios targeting value, size, quality, momentum and low volatility have performed compared to the S&P 500 Index in each calendar year since 2000. The last column on the right shows the annualized returns of these factor-based baskets over the 16-year period. Note that in each and every case, the annualized returns exceeded those of the broader market over the entire holding period.

Factors’ long-run performance

Yet, it is important to note that, despite all five of these factors outperforming the S&P 500 since 2000, they did not do so in each and every year. Factors are subject to the ebbs and flows of the business cycle, much like the sectors of the S&P. But, unlike factors, it is impossible for every sector of the S&P 500 to individually and collectively outperform the entire S&P 500 Index over time. The appeal of factor-based investing is that these major return premiums, based on decades of data, appear not to be subject to this same constraint.