Merry Christmas!

By Billy & Akaisha Karderl, RetireEarlyLifestyle.com

Special to the Financial Independence Hub

For most people in the United States and Canada, Tequila is a very misunderstood drink.

Images of college spring-break kids shooting shots, chanting “one tequila, two tequila, three tequila, FLOOR!” and wet T-shirt contests, with a headache the next morning usually prevent sophisticated people from pursuing the mysteries and finer pleasures that the National Drink of Mexico offers.

Let me help you with this, because there is so much to enjoy about this beverage. If you decide that you want to try tequila gently and possibly include it in your cabinet of fine liquors, take advantage of our simple guide below.

Your world will open.

Only choose 100% Blue Agave tequilas

Simply put, stay away from Mixtos and look for the 100% Agave denotation on the bottle.

A Mixto label might say “made from agave” but it won’t advertise 100% Agave. Mixtos have a lot of additives, other sugars, and impurities and these are the things that will give you a hangover the next morning.

If it doesn’t say 100% Agave, move on to the next bottle.

Three main styles – Blancos, Reposados, Anejos

Blancos: Generally, blanco tequilas are not aged, and have a fiery taste to them. Since all fine tequilas are meant to be sipped (like a fine cognac), if you are not inclined to a fiery POW! in the mouth, then for your initial purchase, we recommend that you move straight to the Reposados or an Anejo, for the smoother and sweeter flavor.

Reposados: These tequilas are aged in American or French white oak barrels for up to one year. Because of this aging, the intense fire of the drink has been somewhat mellowed, and you will taste the characteristics of the barrel. Most Reposados will have a golden color to them and a pleasing, slightly sweet flavor.

Anejos: Tequila that has been aged in a barrel for up to 3 years has been softened. It also will carry the distinguishing characteristics of the wooden barrel in the liquid and will be slightly sweet as well.

Sip / Don’t Shoot it down

Tequila is made from an indigenous plant unique to Mexico called agave. The soil in which the agave grows affects the taste of the end product. It can be sweet, spicy, fruity, earthy or woody. Also, if the agave has met with drought or weather variations, that can also affect the plant and therefore, the taste. This is similar to grape production for wine making.

Producing tequila is a centuries-old tradition handed down from generation to generation, and each distillery has their own way of accenting the flavor of their particular brand.

If you shoot down tequila in one open-throated gulp, you miss all the delicious complexity of the agave flavor. You are also disrespecting the centuries of hand-crafted quality that the Master Distiller has brought to his tequila.

Sipping is recommended.

First find a small wine glass, champagne flute or a brandy snifter.

By Mike Brown

By Mike Brown

Special to the Financial Independence Hub

Despite the financial harm it causes to many, tax debt, or the difference between taxes owed and paid, is an issue that does not receive much coverage compared to other forms of consumer debt like student loan, mortgage, or credit card debt.

At the end of fiscal year 2018, the Internal Revenue Service (IRS) reported that there were 13.1 million delinquent taxpayer accounts. The combined tax debt in the United States is an estimated US$527 billion, with US$381 billion of that coming from federal taxes and the rest from state-based taxes.

If a tax debt case goes unresolved, the consequences can be severe, including things like wage garnishment, asset seizure, or an international travel ban.

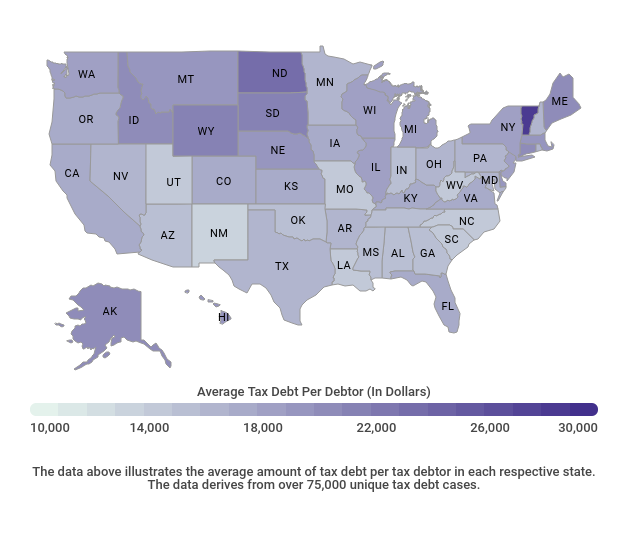

Even with its considerable size and consequences, tax debt goes under-reported, but hopefully a new report published by LendEDU and Solvable will help raise awareness. Analyzing over 75,000 unique cases of tax debt, LendEDU’s report broke down tax debt by state, in addition to the most common reasons for tax debt in each state.

New Mexico posts lowest average Tax Debt, Vermont the highest

The national average tax debt was US$16,489, and 16 states had a figure below the average, while 29 states and Washington D.C. had higher-than-average tax debt.

New Mexico’s average tax debt of US$13,878 was the lowest in the country; following closely behind New Mexico was West Virginia ($14,325), North Carolina ($14,657), and Louisiana ($14,731).

On the other end of the spectrum, Vermont’s average tax debt of US$28,862 was the highest and was in the same neighborhood as North Dakota ($23,671), Wyoming ($21,095), and South Dakota ($21,071).

Regionally, states in the Northeast, Midwest, and West generally had very high tax debt, while states in the South had average tax debt figures on the lower end.

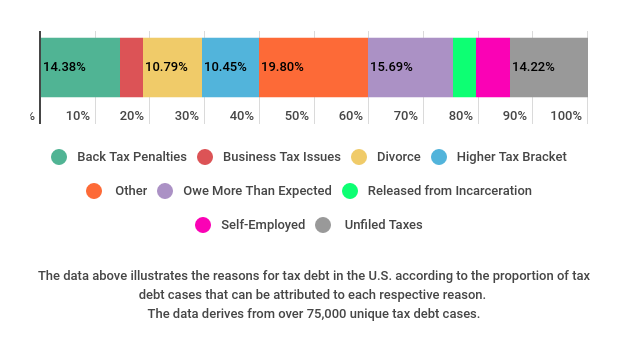

Main Reasons for Tax Debt include Back Tax Penalties and Divorce

A consumer can fall into tax debt for a variety of reasons, like underestimating how much in taxes he or she owes or not accounting for income made as a freelancer. Continue Reading…

By Penelope Graham, Zoocasa

Special to the Financial Independence Hub

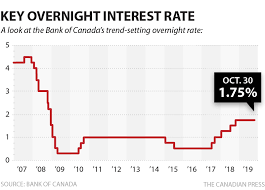

The final rate announcement from Canada’s central bank has come and gone: and it appears that the cost of mortgages and other forms of variable-rate borrowing are to remain stable well into next year.

The Bank of Canada (BoC) opted to leave its trend-setting Overnight Lending Rate (which consumer lenders use to set the pricing of their variable mortgages and lines of credit) at 1.75% on December 4th. The rate has held status quo since October 2018, and makes the BoC somewhat of an outlier when it comes to monetary policy; many central banks around the world, including the U.S. Federal Reserve, cut interest rates this year to counter growing U.S.-China trade tensions, as well as the growing threat of recession.

A positive take on the Canadian economy

However, the BoC has maintained all year that while global economic instability remains a key risk, it feels confident enough in both the international and domestic economies to avoid adding stimulus. Of course, tweaking interest rates is a key tool the BoC has at its disposal in times of economic need; by keeping the cost of borrowing lower, it encourages continued consumer spending and helps avoid a credit crunch.

While a number of economists and analysts anticipated at least one downward rate cut in 2019, that never materialized. In its December announcement, the central bank stated, “There is nascent evidence that the global economy is stabilizing, with growth still expected to edge higher over the next couple of years.” It also adds that while the risk remains, a potential recession has become less likely, and that there is reason for optimism as Canada’s economy is stabilizing.

The December report outlines that end-of-year growth has progressed largely in line with what was forecasted in October, with consumer spending rising 1.3%, as well as upticks in business investment and wage growth. As well, the BoC’s most important metric, core inflation, stayed near its 2% target, and is expected to remain in that range over the next two years. As long as that remains the case, it’s unlikely the BoC will be prompted to cut or hike rates in the near future.

Lower rates to spur Housing demand in the New Year

With little chance of rate movement in the short term, what does that spell for Canada’s housing market? In what is somewhat of a self-fulfilling prophecy, the BoC included strengthening real estate activity as one of the main contributors to economic growth, further supporting its platform to keep rates at their current historical lows. Lenders have been able to keep their variable-rate offerings deeply discounted, while fixed mortgage rates have been kept down by especially low yields in the bond market.

That’s led to a boom in cheaper credit and mortgages over the course of 2019, which has fueled growing home-buyer demand; while the federal mortgage stress test did help tamp down some borrowing activity by requiring applicants to qualify for higher rates, the shock impact of the measure has largely been absorbed.

Housing Agency calls for home sales and prices to rise through 2021

That’s a trend that will continue over the next 12 to 24 months, according to several analysts. For example, Capital Economics has forecasted national house price growth will rise at least 6% in 2020 due to low mortgage rates, as well as a growing gap between housing supply and demand. Continue Reading…

By Casey Milton

Special to the Financial Independence Hub

Sometimes loved ones can be judgemental and happen to measure your affection for them based on what you get them for Christmas! But jokes aside, Christmas is an occasion that is incomplete without colourful boxes of presents.

But what about the budget? Especially when there are numerous people that you want to gift!

Here are 10 unique gift items to inspire you, which can be special, utilitarian and affordable all at the same time.

Before we get on with the list, it’s a good time to acknowledge that while many of us search for the most special gifts to give to our loved ones, it is also around this time that we contribute a lot to the global pollution rate with our unconscious consumer habits. It is high time we understand that sometimes “affordability” is not all about OUR monetary budgets but also about the Environmental cost.

So let’s be minimalists, let our gifts and gift packaging be in sync with the environment, and let the whole world have a breath of fresh air after the festivities are over.

1.) DIY Gift Basket

Gift baskets are the coolest things that can fit just about any budget! You can create one without spending any money at all, with the help of a cardboard box or paper mache. Though the basket can make your presentation much special, it is still what goes into the basket that matters! If you can spend a little time to browse the local thrift stores, you may find some cool objects within your budget. Here are some ideas :

2.) Handmade “Gift in a Jar”

2.) Handmade “Gift in a Jar”

The gift in a Jar is certainly not about a jar of honey or pickle! It is something a whole lot sweeter and full of joy! And this has so much potential to be a no-money gift item, based on whether you are buying the jar, and what you fill in it. Simply, take glass jar (recommended, reused jar) and fill it up with one of the following things :

3.) Personalized Tech Accessories

Tech accessories can be the most forward-thinking gifts, but only when you know your gift will compliment your dear one’s tech stuff. When it comes to such accessories, what better way to make them unique, than personalization! It doesn’t have to cost too much money, just needs a bit of your creativity:

4.) Rugs & Runners

Rugs can be functional gifts on a budget for the winter season and they don’t always have to be fancy or expensive. Here are some of the practical options:

5.) Shelves of all kinds

You can never go wrong with shelves even if the person you are gifting lives in a rented space. The only condition is that you have to be careful about size and the installation process. Here are some ideas:

6.) Plants