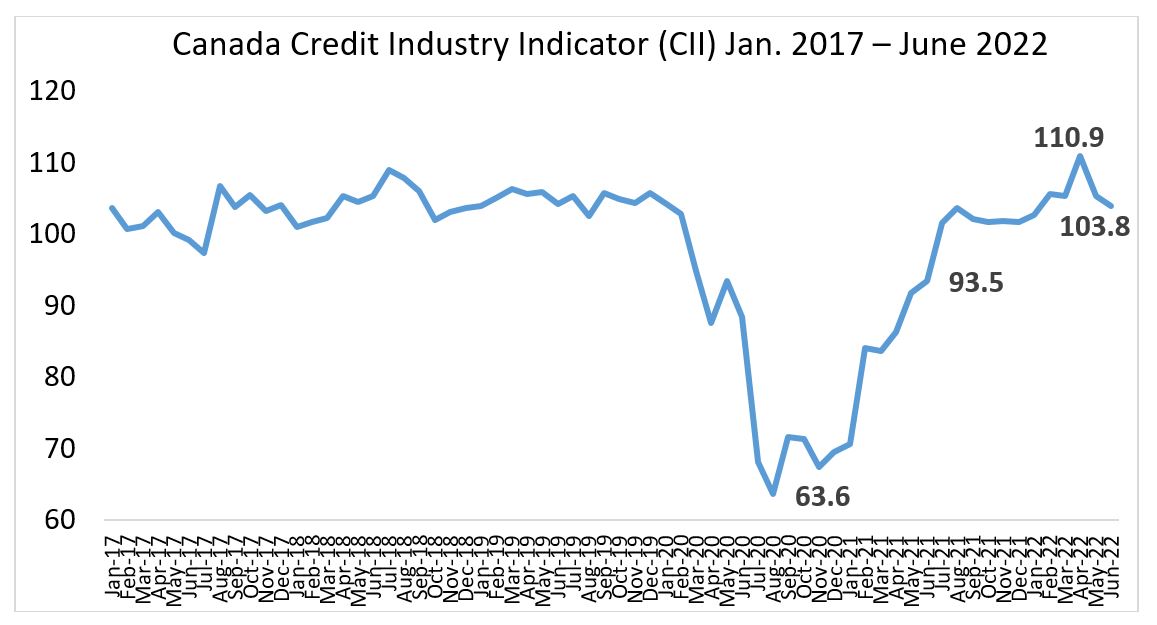

A revolutionary new approach to preserving portfolio longevity through a modern “Tontine” structure was unveiled Wednesday by Guardian Capital LP and famed author and finance professor Moshe Milevsky.

GuardPath™ Longevity Solutions, created in partnership between Guardian and Schulich School of Business finance professor Milevsky, is designed to address what Nobel Laureate Economist William Sharpe has described as the “nastiest, hardest problem in finance” 1

Announced in Toronto on September 7, a press release declares that the “ground-breaking step” aims to “solve the misalignment between human and portfolio longevity.” See also this story in Wednesday’s Globe & Mail.

Over the years, I have often interviewed Dr. Milevsky about Retirement, Longevity, Annuities and his unique take on how the ancient “Tontine” structure can help long-lived investors in their quest not to outlive their money. Milevsky has written 17 books, including his most recent one on this exact topic: How to Build a Modern Tontine. [See cover photo below.]

Back in 2015, I wrote two MoneySense Retired Money columns on tontines and Milevsky’s hopes that they would one day be incorporated by the financial industry. Part one is here and part two here. See also my 2021 column on another pioneering Canadian initiative in longevity insurance: Purpose Investment Inc.’s Longevity Pension Fund.

Addressing the biggest risks faced by Retirees

In the release, Milevsky describes the new offering as a “made-in-Canada” solution that addresses “the biggest risks facing retirees and are among the first of their kind globally. Based on hundreds of years of research and improvement and backed by Guardian Capital’s 60-year reputation for doing what’s right for Canadian investors, I am confident these solutions will revolutionize the retirement space.”

In an email to me Milevsky said: “You and I have talked (many times) about tontines as a possible solution for retirement income decumulation versus annuities. Until now it’s all been academic theory and published books, but I finally managed to convince a (Canadian) company to get behind the idea.”

In the news release, Guardian Capital Managing Director and Head of Canadian Retail Asset Management Barry Gordon said that “for too many years, Canadian retirees have feared outliving the nest egg they have worked so hard to create.” It has answered that concern by creating three solutions that aim to alleviate retirees’ greatest financial fears: The three solutions are described at the bottom of this blog.

With the number of persons aged 85 and older having doubled since 2001, and projections suggesting this number could triple by 2046,2 Guardian Capital says it “set out to create innovative solutions that this demographic could utilize when seeking a greater sense of financial security.”

Tontines leap from Pop Culture to 21st Century reality

Tontines were one of the most popular financial products for hundreds of years for individuals willing to trade off legacy for more income, Guardian says. Once in a while the tontine shows up in popular culture, notably in the film The Wrong Box, where the plot revolves around a group of people hoping to be the last survivor in a tontine and therefore the recipient of a large payout.

Tontines were one of the most popular financial products for hundreds of years for individuals willing to trade off legacy for more income, Guardian says. Once in a while the tontine shows up in popular culture, notably in the film The Wrong Box, where the plot revolves around a group of people hoping to be the last survivor in a tontine and therefore the recipient of a large payout.

“With our modern tontine, investors concerned about outliving their nest egg pool their assets and are entitled to their share of the pool as it winds up 20 years from now,” Gordon says, “Over that 20-year period, we seek to grow the invested capital as much as possible to maximize the longevity payout. Along the way, investors that redeem early or pass away leave a portion of their assets in the pool to the benefit of surviving unitholders, boosting the rate of return. All surviving unitholders in 20 years will participate in any growth in the tontine’s assets, generated from compound growth and the pooling of survivorship credits. This payout can be used to fund their later years of life as they see fit, and aims to ensure that investors don’t outlive their investment portfolio.” Continue Reading…