My latest MoneySense Retired Money column looks at the dilemma many retirees and would-be retirees face these days: that with sky-high stock prices and interest rates seemingly bottoming and headed up, there’s no such thing as a truly “safe” investment. Click on the highlighted headline for full column: Is the All-Weather portfolio the answer to the shortage of “safe” investments?

Even supposedly safe bonds, bond funds or ETFs largely suffered losses in 2021 as interest rates seemed poised to rise: now that various central banks are starting to hike rates, such pain seems destined to continue in 2022 and beyond.

Yes, short-term bank savings accounts and GICs seem relatively safe from both stock market meltdowns and precipitous rises in interest rates, but then there’s the scourge of inflation. Even if you can get 2% annually from a GIC, if inflation is running at 4%, you’re actually losing 2% a year in real terms.

But what about those Asset Allocation ETFs that have become so popular in recent years. This site and many like it are constantly looking at products like Vanguard’s VBAL (60% stocks to 40% bonds) or similar ETFs from rivals: iShares’ XBAL or BMO’s ZBAL.

The nice feature of Asset Allocation ETFs is the automatic regular rebalancing. If stocks get too elevated, they will eventually plough back some of the gains into the bond allocation, which indeed may be cheaper as rates rise. Conversely, if stocks plummet and the bonds rise in value, the ETFs will snap up more stocks at cheaper prices.

But are these ETFs truly diversified?

True, any one of the above products will own thousands of stocks and bonds from around the world. They are geographically diversified but I’d argue that from an asset class perspective, the focus on stocks and bonds means they are lacking many other possibly non-correlated asset classes: commodities, gold and precious metals, real estate, cryptocurrencies, and inflation-linked bonds to name the major ones.

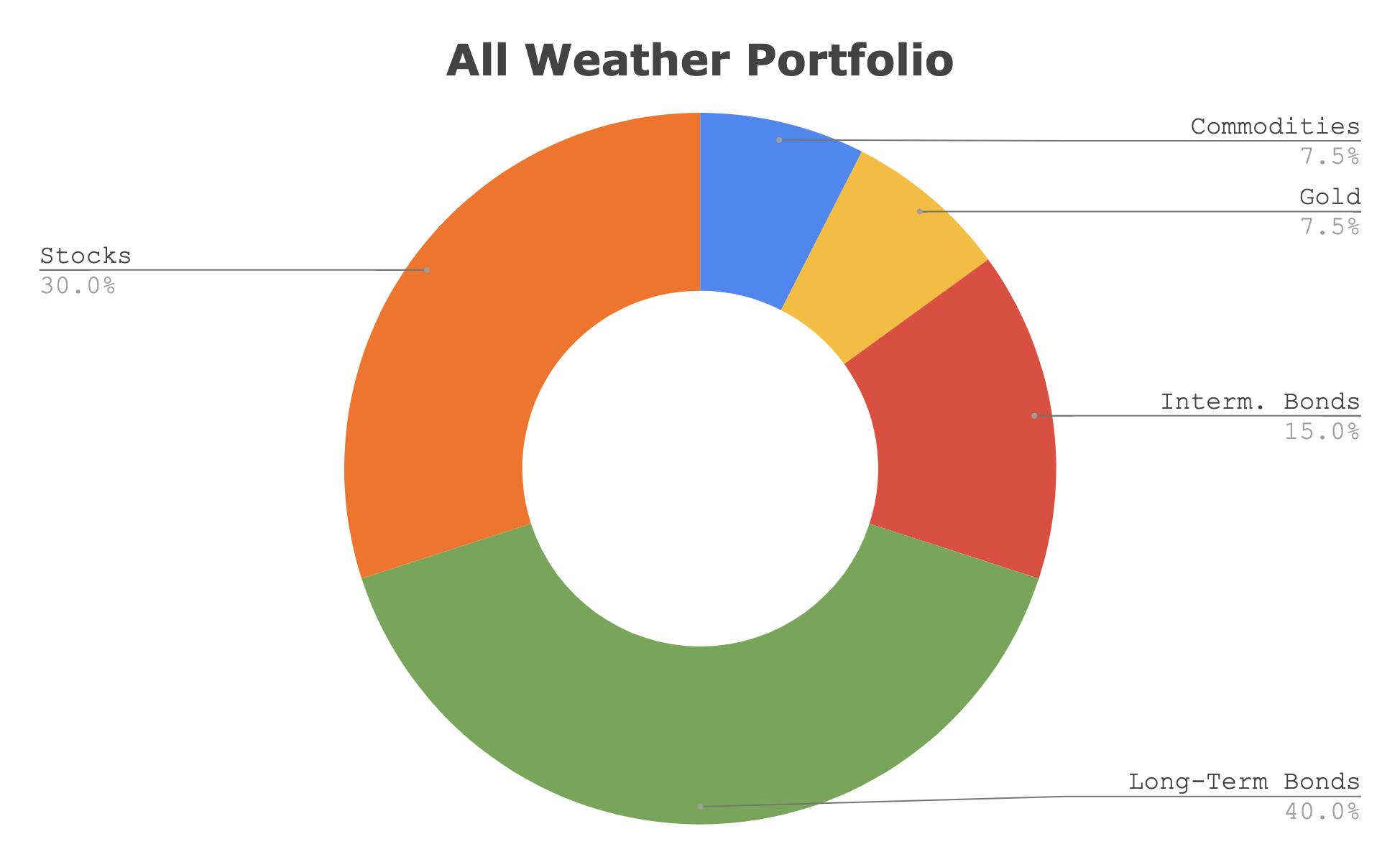

The Permanent Portfolio and the All-Weather Portfolio

I’ve always kept in mind Harry Browne’s famous Permanent Portfolio, which advocated just four asset classes in four 25% amounts: stocks for prosperity, long-term bonds for deflation, gold for inflation and cash for recessions.

A bit more complicated is the more recent All-Weather portfolio, from American billionaire and author Ray Dalio, founder of Bridgewater Associates. You can find any number of variants of this by googling those words, or videos on YouTube.com. There’s a good book on this, Balanced Asset Allocation (by Alex Shahidi, Wiley), which makes the All-Weather portfolio its starting point. Continue Reading…

A quick note to say Happy 2022 to all the Hub’s readers and supporters. We’ll be back to our regular blog-a-day rotation on Tuesday.

In the meantime, I’ll point readers to Dale Roberts’ excellent year-end market wrap for MoneySense, which was published Friday.

Click on the highlighted headline to access, but settle down with a coffee before you do: it’s quite a long read: Making Sense of the Markets: 2021.

It’s a thorough long read that looks at all the major market developments each month in 2021 and you’ll also see a number of prescient market calls made by Dale over the last few years, including an early call on Covid-19 itself, an early call on the Energy and Commodities recovery, and several others.

I’ve followed Dale for some years now: he famously tweets as @67Dodge and I now help edit his weekly MoneySense market wrap, seeing as I became MoneySense’s Investing Editor at Large a few months ago.

In normal years, I would move new money into the TFSA on January 1st but there’s probably no rush this year until Tuesday, Jan. 4, seeing as the Canadian market is closed Monday. (The US will be open that day though).

I’ve not decided exactly what to invest in but it will likely be inflation-related. Going back to Dale Roberts, you can glean a few ideas from his 2021 market wrap: things like short-term TIPS ETFs, or the Purpose Real Assets ETF, or energy/commodity plays.

Personally, I’ve been researching Ray Dalio’s All-Weather portfolio (google it for videos and articles, or try this Seeking Alpha link on it). I’ve concluded that our own family has sufficient US equity exposure but not enough in commodities or TIPS [Treasury Inflation Protected Securities] plays.

Dalio is a bit heavier on fixed-income than most, with a mix of long-term and short-term bonds. His recommended equity exposure is a bit lower, and he suggests 7.5% commodities and 7.5% in gold. Readers may therefore find Friday’s Hub article on gold of interest: A perfect storm for gold.

Every case is different of course. IF I were looking to boost US equity exposure, I’d certainly be considering the new Canadian Depositary Receipts (CDRs), more on which you can read on the Hub early in the new year. If we didn’t already own Berkshire Hathaway, I’d be tempted to add to it with the CDR version of Berkshire, seeing as it pays no dividends and would be a good value counterbalance to high-priced US tech stocks.

So by all means get your $6,000 (if available) into your TFSA early in 2022 but take a few days to figure out how to invest it.

The wild card is certainly Omicron. If you’ve not yet gotten your booster, I highly recommend it.

So again, have a happy, healthy and profitable 2022!

My latest MoneySense Retired Money column describes the first New Year’s Resolution most of us can accomplish on or soon after January 1, 2022.

And unlike resolving to go to the gym or to buy (and use) that new Peloton, this is one you can tick off your to-do list within minutes of changing the calendar to 2022.

I refer of course to making your annual TFSA contribution — $6,000 this year — and you can read all about it by clicking on the highlighted text here to go to the full MoneySense column: Why contributing to a TFSA is a Good Resolution.

Every year since the program commenced in 2009, as close to January 1st as possible, each member of our family faithfully adds the maximum contribution amount (initially $5,000, briefly $10,000 and currently $6,000) to our TFSAs. And because we view them not as tax-free savings accounts but as tax-free Investment accounts, they have all grown substantially: to the point my family members do not wish the exact balances to be divulged to this broad readership. Arguably, TFSA is a misnomer: they should have been called TSIAs.

The column describes Robb Engen’s blog, titled “A sensible RRSP vs TFSA comparison” which reprises David Chilton, who said it all depends on:

If you go the RRSP route, don’t spend your refund.

If you go the TFSA route, don’t spend your TFSA.

Whatever route you go, save more!

How about the Cash Flows & Portfolios blog entitled Can you retire using just your TFSA? It begins with this glowing commendation for the TFSA: “The opportunity for Canadians to save and invest tax-free over decades could be considered one of the greatest wonders of our modern financial world.”

The blog’s authors (known only as Mark and Joe) conclude that if you start early enough (like our daughter) you could indeed retire using just a TFSA.

To recap the rules: the cumulative contribution amount as of Jan. 1, 2022 is now $81,500. If you believe in the time value of money, it follows that you should contribute the full $6,000 the moment the new year begins, which is why I always call it “New Year’s Resolution Number 1.” Unlike joining fitness clubs, you can tick this one off your To-do list moments after you sing Auld Lang Syne (assuming you use an online discount brokerage).

Because of the long time horizon, young people could well put only equities into their TFSA, and if they do so from the get-go they will far outstrip the performance of the sadly all-too-common default option of parking TFSA funds in GICs that pay almost nothing relative to inflation.

Not only does an 18-year old have a good 47 years until the traditional retirement age of 65, keep in mind that unlike RRSPs, you can keep contributing to TFSAs well into your 90s or 100s, if you live that long. I knew a lady who was contributing to hers past age 100! Those near retirement could ratchet it down to a conservative Asset Allocation ETF like VBAL, ZBAL or XBAL, all of which cover the world of stocks and bonds in C$ in a traditional 60/40 asset mix of stocks to bonds.

I do try to avoid putting US-based dividend paying stocks or ETFs in the TFSA: put those in your RRSP or RRIF. Canadian dividends and interest belong in a TFSA, as do speculative US or foreign stocks that don’t pay dividends.

Speaking of RRSPs, what about the perennial question of which to fund first: TFSA or RRSP? My short answer is to do both but if you really have to choose, I’d pick the TFSA in most situations. Certainly, young people in a low tax bracket and older folk who are in danger of seeing OAS or GIS benefits clawed back should prioritize the TFSA.

Those in top tax brackets by virtue of high employment income should maximize their RRSPs but if you’re in the top tax bracket then you can probably also afford to maximize your TFSA. If despite such a high income you are encumbered by a lot of mortgage debt and/or credit card debt, I’d even suggest liquidating some of your TFSA to eliminate some of that debt: you can always regain your lost TFSA contribution room in future years and once you are debt-free there should be few obstacles to maximizing retirement savings in all such tax-optimized vehicles.

Almost since the Hub’s inception in 2014, the principals behind the popular RetireEarlyLifestyle.com have provided in-depth coverage of global travel and the tips to achieve early Financial Independence they used themselves to “retire” in their early 30s.

The following email interview was between myself and Billy and Akaisha Kaderli. Our intention is to publish it on both sites. Here’s the link to their version, which ran Dec. 14th.

So without further ado:

JC Q1: Akaisha and Billy, you are about the same age as myself and my wife Ruth and apart from being American and Canadian, we appear to have several things in common: we both run sites focused on Financial Independence, have written some books on same, and continue to be working at least on our own terms even though we have achieved Findependence years ago: more than 30 in your case, seven in ours. One difference is you travel a lot more, while we are content to stay in our Toronto home near Lake Ontario and take just a few weeks abroad, preferably if it’s a business expense. So let me start with the provocative statement that I think travel is expensive and over-rated. I have no doubt you can rebut that!

A&B: First, let us clarify that the time we spend on our website is what we consider to be our volunteer time. Yes, there are products that we sell, but 99% of our information is free because we are passionate about teaching financial literacy to those who want to learn.

In regards to your comment about travel being expensive and over-rated, it depends.

We think that there are differing styles of travel. There are tourists, visitors and travelers. There is no one-right-way to journey around, and we love it that people get out and about, expanding their minds.

Tourists tend to go on vacation for a week or two, spending a good deal of money on lodging, transport, entertainment and meals. Every day must be “perfect” and if the weather doesn’t cooperate or if service is not great, then there is this sense of disappointment. They tend to go to resorts or even exotic locations, but the lodging and amenities have a sense of Disneyland unreality, and are often over-priced.

Sure, there might be a water buffalo in some rice fields, with “workers” wearing a “traditional clothing uniform” but the real locals are miles away. Tourists will pay $10 or more for a beer that the residents of the area would purchase for about a buck.

Also, Tourists might like the idea of a vacation or might not. Mostly, they like the comfort and routine of home, and a vacation is an interruption in their experience of the familiar. Many times, it borders on the feeling that “this is a waste of time. I’d rather be home.” They don’t know any local phrases in a foreign language except maybe Yes, No, Thank you, Bathroom and Beer. Tourists have more of a passive approach to their excursion and want to be entertained. Then they rate their experience with their friends when they return home.

In order to go on this vacation, they stop their mail, perhaps have a house sitter or family member/friend water their plants or watch their pet. They have probably cleaned out their refrigerator and have to stock up once again when they return home. And it all seems to be a hassle. “Would have been easier to just stay at home in the first place. Plus, now we have this credit card bill and all these souvenirs to give to friends.”

Visitors on the other hand stay in a location for a bit longer – maybe even a month or so. They know some survival phrases in the local language and choose lodging that is more middle range than a resort option. About half the time, they will eat outside of big chain restaurants with well-known names and take a chance on a local restaurant.

They are a bit more self-guided in their entertainment choices, perhaps utilizing Google maps or a local tour of the area to become familiar with their surroundings. They may select local transportation or hire a driver to go from archaeological ruins and museums or they might take a self-directed walking tour.

Using a daypack, they bring their own drinking water and perhaps some snacks to munch on as they go from place to place in their day.

Traveling for them is not necessarily a “vacation” but more of an experience, or a sabbatical. They could take cooking classes, language classes, painting courses and the like and they interact with the local people.

After their time away from home, their lives have altered in some way, perhaps expanding their perspectives or dropping an outworn routine. They look forward to their next adventure.

Then you have Travelers.

Billy and Akaisha at Chacala Beach, Nayarit, Mexico

These are the people who go from place-to-place with no itinerary other than their own style of meandering. They usually buy only one-way tickets, figuring out how to return – if they do – at another time. They communicate with the native inhabitants in their own language, purchase food, clothing and travel equipment from markets in the area and will often eat street food or dine in local restaurants.

These people travel for months, sometimes years at a time and rent apart-hotels, AirBnBs, house sit or bargain for a hotel room for a monthly rate. They may or may not have a home base for when they return from their wandering.

Travelers are more flexible mentally and are willing to have their routines interrupted. If the weather pattern is not to their liking, they might move on, or hunker down till the cold, heat, or rain stops. They do not live their traveling life as in “Today is Tuesday so it must be Belgium.” They speak with other travelers to get insight into their possible next stop.

Travelers employ digital equipment and apps to communicate with family and friends. They utilize email, sending digital photos or videos taken of their experiences, and they travel lightly. They throw their daypacks onto a bus or carry them on an affordable inter-country flight. Getting their cash in the currency of the country they are living in, they work the ATMs with a debit card that pays the withdrawal fee back.

They manage their lives online and have been receiving paperless mail for a long time. Photos are placed up in the cloud and they take care of business via Skype, WhatsApp or Signal, benefitting from medical tourism for their health care.

Travel does not cost them “more.” In fact, if they were spending their time “at home” they would still have a baseline of expenses – lodging, food, transport, entertainment for instance. But now they have incorporated these same expenses along with globe-trotting which creates memories for a lifetime and stories to share.

In general, travel has broadened their minds, giving them a unique perspective of the world and a confidence and self-reliance that pervades daily living.

We think it’s important to know one’s traveling style and enjoy who you are. There is not a one-size-fits-all, and we recognize that travel isn’t for everyone.

Someone has to stay home, attend the roses and mow the lawn!

Hub CFO Jonathan Chevreau

How does extensive travel differ from short vacations from full-time employment?

JC Q2: To clarify, we enjoy travel too; was just playing devil’s advocate. Before we switch to Findependence, do you think there’s a big difference between the expensive two-week vacations many salaried employees take, and actually renting a house or suite abroad for 3 or 4 months at a time in Semi-retirement?

A&B: Yes, there is a big difference, actually.

When one is still working, vacations are stress busters. Work hard, play hard.

These holidays tend to be results of pent up demand for luxury; things we have denied ourselves during our working life like splurging on fine meals out, visiting an exotic place far from home, a ski vacation, or a safari. Continue Reading…