Retirement is a close second to home ownership, according to a LendEDU survey of American saving priorities

While having enough money saved for Retirement is narrowly behind buying a home, more than a third of Americans don’t expect they’ll ever be able to retire, according to a survey released Tuesday from LendEDU.com.

Retirement saving was cited by 19% of 1,000 respondents, versus 20% prioritizing “buying my own house or apartment.” Paying off credit-card debt was cited by 14% and building an emergency fund by 10%.

While there was only a minor lack of confidence about paying off credit cards and building an emergency fund, 17% don’t believe they’ll ever become homeowners and but almost four in ten Americas (39%) don’t believe they’ll ever be able retire.

Of those doubting their ability to retire, 52% were over age 54, 30% were between 45 and 54, and 15% were 35 to 44.

As for emergency savings, 33% said a major bill resulting from an injury would destroy their savings and therefore their long-term financial goals; another 14% cited some form of debt that could quickly get out of hand. However, 28% felt “relatively secure” and did not believe their financial goals could be derailed.

Secondary priorities

After home ownership and retirement, the most cited financial priorities were some form of getting out of debt: 14% cited paying off credit-card debt, 7% paying off student-loan debt, and 4% cited paying off other forms of debt apart from credit cards or student loans. 6% answered “Building my credit score,” 5% wanted enough saved to move out of their parents’ homes and rent a home or apartment, 4% said “Buying a car,” and 3% wanted to start a business.

1% wanted to invest in real estate, another 1% wanted to buy a second home and yet another 1% wanted to buy a second or third car. 3% want to “create a retirement account” and 2% want to “invest in the market outside my retirement account.”

Money a bigger priority than Love?

Of the 37% who were not currently in a long-term relationship, 72% were more focused on their financial targets, versus a minority 23% who prioritized finding a romantic partner. (The rest preferred not to say). The survey sees this as a “glass half full” finding: “It is good that Americans are quite serious when it comes to realizing their personal finance goals. But, on the glass empty side, sometimes one’s finances can’t buy happiness, or in this case love, and it is always important to understand what is truly important in life.” Continue Reading…

Finance professor Moshe Milevsky welcomes industry’s implementation of academic longevity insurance theories

My latest MoneySense Retired Money column looks at two longevity-related financial products that the industry may develop after the road to them was paved in the March 2019 federal budget. You can access the full column by clicking on the highlighted headline: A new kind of annuity designed to help Canadian retirees live well, for longer.

Once they are created by the industry, hopefully in the next year, these new products will introduce an element of what finance professor Moshe Milevsky has described as “tontine thinking.” In the most extreme example, a tontine — often depicted in fictional work like the film The Wrong Box — features a pool of money that ultimately goes to the person who outlives everyone else. In other words, everyone chips in some money and the person who outlives the rest gets most of the pot. As you can imagine at its most extreme, this can lead to some nefarious scenarios and skulduggery, which is why you occasionally see tontines dramatized in film, as in The Wrong Box, and also TV, as in at least one episode of the Agatha Christie TV adaption of Miss Marple.

Fortunately, the Budget doesn’t propose something quite as dramatic as classic tontines but get used to the following two acronyms if and when the insurance and pension industries start to develop them: ALDA is an acronym for Advanced Life Deferred Annuity. As of 2020, ALDAs could become an investment option for those currently with money invested in registered plans like RRSPs or RRIFs, Defined Contribution (DC) Registered Pension Plans and Pooled Registered Pension Plans (PRPPs).

The other type of annuity proposed are Variable Payment Life Annuities (VPLAs), for DC RPPs and PRPPs, which would pool investment risk in groups of at least 10 people. Not quite tontines in the classic academic sense but with the pooling of risk VPLAs certainly have an element of “tontine thinking.”

The budget says a VLPA “will provide payments that vary based on the investment performance of the underlying annuities fund and on the mortality experience of VLPA annuitants.” That means – unlike traditional Defined Benefit pensions – payments could fluctuate year over year.

There is precedent for pooled-risk DC pensions: The University of British Columbia’s faculty pension plan has run such an option for its DC plan members since 1967.

The budget said Ottawa will consult on potential changes to federal pension benefits legislation to accommodate VPLAs for federally regulated PRPPs and DC RPPs, and may need to amend provincial legislation. But it’s ALDAs that initially captured the attention of retirement experts, in part because of its ability to push off taxable minimum RRIF payments.

Up to $150,000 of registered funds can go into an ALDA

An ALDA lets you put up to 25% of qualified registered funds into the purchase of an annuity. The lifetime maximum is $150,000, indexed to inflation after 2020. Beyond that limit you are subject to a penalty tax of 1% per month on the excess portion. Continue Reading…

Robo-Advisor NestWealth.com today announced it is acquiring Alberta-based Razor Logic Systems (makers of RazorPlan financial planning software.) NestWealth.com founder and CEO Randy Cass is positioning the combined entity as the first (and only) “B2B digital wealth management platform to offer both professional investment solutions and sophisticated financial planning capabilities.”

The acquisition is Nest Wealth’s first, Cass said in an email. In a press release embargoed till Wednesday morning, Cass said both firms “have always shared a common goal to make life better for the individual investor so this seems like a very natural fit … Because of what our two companies are able to accomplish together our users will be able to offer personalized financial plans integrated with their actual investment portfolios.”

Founded in 2011 by Certified Financial Planner and Chartered Life Underwriter Dave Faulkner, Razor Logic Systems is the developer of RazorPlan, the popular financial planning software that lets thousands of financial advisors quickly analyze a client’s needs, generating full financial plans in as little as 15 minutes. Its Financial Plan Advantage Ltd. (FPAdvantage) was expanded in 2012 to become Razor Logic Systems. In the press release, Faulkner — Razor Logic’s co-founder and CEO — said the deal with Nest Wealth will help enhance the value financial advisors create for clients: its tools help make complex financial planning easier to accomplish for advisors and understandable for their clients.

Fintech startup’s first acquisition

Nest Wealth is actually the newer company, a “fin tech” (financial technology) firm founded by Cass in 2014. It was one of the first Canadian robo-advisors on the market, although it prefers the term “digital wealth management platform.” Nest Wealth is the trade name of Nest Wealth Asset Management Inc. Continue Reading…

While indexing giant Vanguard Group and its Canadian unit are best known for their pioneering work in passive investing, both through index mutual funds and ETFs, they are also significant players in active fund management.

On Monday, it educated Canadian financial advisors at its 2019 Investment Symposium in Toronto, with the focus on two of the four actively managed mutual funds it first announced last summer.

Vanguard Investments Canada Inc. head Kathy Bock, who took over the position on January 1st, reminded the (mostly fee-based) financial advisors in attendance that Vanguard actually started life as an active manager over 40 years ago, and the firm now actively manages more than US$1.6 trillion globally, which is about a quarter of the firm’s total assets under management of more than US$5.3 trillion. That makes Vanguard the third largest active fund manager in the world. See also this Hub blog on this from last September: Vanguard, the Hidden $1.3 Trillion player in active management. (As you can see, the figure has risen with the markets since then).

Vanguard Canada head Kathy Bock

These mutual funds do not pay advisors trailer commissions: they are F series funds, which means fee-based advisors are free to set whatever additional fee they negotiate with their clients, just as they do with ETFs. They can also be purchased at some, but not yet all, discount brokerages

The management fees on these actively managed mutual funds are a maximum 0.5%; but in the first year, the fee ranged from 0.34% to 0.4%, which makes them only marginally more costly than Vanguard’s popular asset allocation ETFs that were unveiled just over a year ago (and which spawned several imitators). This is partly achieved through a management fee waiver that can apply, depending on manager performance, as explained at the bottom of this blog.

These mutual funds are managed for Canadians, although the actively managed subadvisors are global active giants, as outlined below. Because they are new funds, they have not disclosed the Management Expense Ratios (MERs).

True, at least one advisor in the question period seemed ambivalent about how fee-based advisors can reconcile such an approach to the indexing gospel that Vanguard has so thoroughly dispensed over the years. The answer, according to one of the sub advisors featured, is that the two approaches can complement each other, potentially reducing overall volatility. Buying exclusively ETFs means that over the coming ten years you’re “dooming yourself to a lot of failing businesses,” said Nick Thomas, partner with Baillie Gifford, one of two sub advisors to the Vanguard International Growth Fund, together with Schroder Investment Management North America Inc.

The advisor who posed the question was understandably perplexed by the many studies indexing proponents often cite about how most actively managed funds fail to beat the indexes net of their own additional costs. But the Vanguard managers replied that there are cases where active management can outperform, at least outside the highly liquid U.S. market. Portfolios will be more concentrated than the broad indexes and if an investing thesis pans out, there is an opportunity to “pick” winners at the outset of major trends like A.I. and the cloud, and avoid losers. Presumably managers with skills in combination with good financial advisors can add the kind of “Advisor’s Alpha” to client returns that Vanguard has pioneered.

And if active management makes a good complement to equity portfolios, that should also go for balanced mandates. Indeed, the other highlighted fund was Vanguard Global Balanced Fund, with a 65%/35% equity/fixed-income split managed by Wellington Management Canada ULC, headquartered in Boston. The proportion can move to 60/40 or 70/30, depending on market view. It was launched with the other three mutual funds on June 20, 2018.

China tech big focus of Vanguard International Growth Fund

Baillie Gifford’s Nick Thomas

Most of the discussion centered on the Chinese holdings of Vanguard International Growth Fund: China accounts for 20% of the fund’s geographic allocation. The top ten holdings include three Chinese web giants: Alibaba Group Holding Ltd., Tencent Holdings Ltd and Baidu Inc. It also holds Amazon.com Inc. and MercadoLibre Inc. among its top holdings.

Schroders manager John Chisholm is slightly underweight Emerging Markets and market weight China. Baillie Gifford’s Thomas is slightly more enthusiastic, being overweight both Emerging Markets and China. But both see promising long-term growth prospects for the major Chinese web giants. Asked about the current Trump trade war and accusations of theft of American intellectual property, the managers downplayed this as a U.S. interpretation of the facts. Thomas said he views both Tencent and Alibaba as “superior to Facebook or Amazon.”

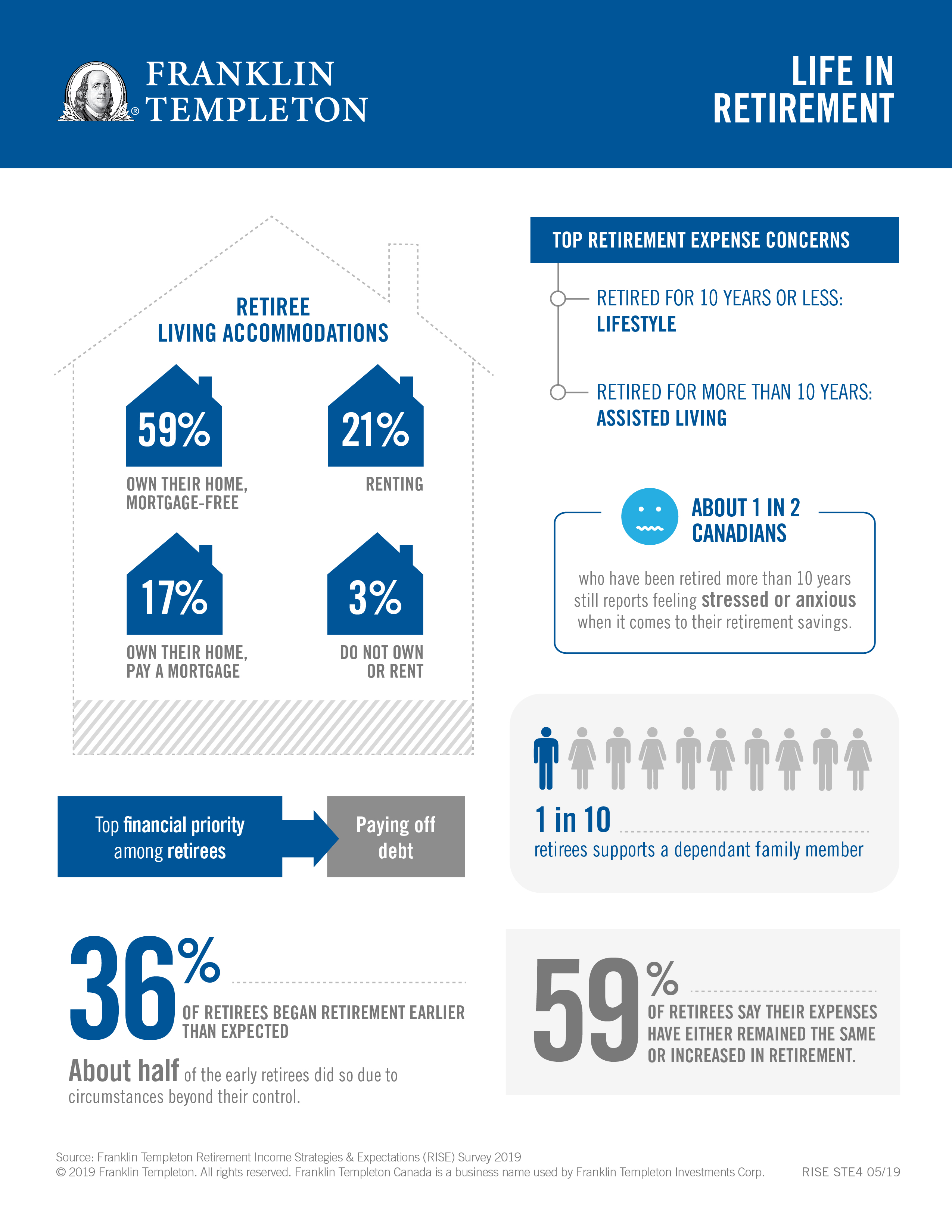

Almost half of North American’s young baby boomers would consider postponing retirement because of Savings concerns, a survey out Wednesday finds. Even so, more than half surveyed had to retire early, often because of circumstances beyond their control.

Franklin Templeton’s 2019 Retirement Income Strategies and Expectations (RISE) survey found that 21 per cent of Canadian young baby boomers (ages 55 to 64) in pre-retirement have not saved anything for retirement. And in the United States, 17 per cent of young boomers are in a similar predicament.

13 to 15% expect to work until they die

As a result, 46% of young Canadian boomers and 48% of young American boomers are considering postponing retirement, with roughly 15% of Canadians and 13% of Americans expecting to work until the end of their life. Furthermore, 22% of self-employed Canadians don’t ever plan to retire.

However, things don’t always go as planned: 54% of young Canadian boomers and 60% of their American counterparts retired earlier than expected, compared to 32% and 37% of Canadian and American older boomers aged 65 to 73.

More Canadian young boomers retired due to circumstances beyond their control than Canadian older boomers (34% versus 20%, respectively). There was a slightly wider gap amongst Americans: more American young boomers retired due to circumstances beyond their control than American older boomers (33% vs 17%, respectively).

Boomers in different life situations after post 2009 bull run

“In 2009, when equity markets started to recover, many young boomers were moving up the career ladder; whereas older boomers were approaching retirement at the top of their earning years,” said Duane Green, president and CEO, Franklin Templeton Canada. “A decade later, after a long bull market run, young and older boomers are in different life situations once again. We see many older boomers benefitting from the transfer of wealth from their parents, yet the young boomers have had a challenging experience balancing more expensive lives – due to caring for elderly parents and still having financially dependent children – all while saving for that increasingly elusive retirement.”

Nearly a quarter (24%) of Canadian young boomers in pre-retirement currently support a dependent family member, compared to 9% of retired older boomers. The top three sacrifices young boomers made for dependents were: saving less money, cutting back personal spending and withdrawing from personal savings. They were least likely to use employer vacation time or take unpaid time off work for caregiving.

“With life expectancy increasing and retirement savings becoming ever more challenging, due to the high costs of living, we are seeing increased concern over having enough money for retirement across all generations,” said Matthew Williams, SVP, Franklin Templeton Canada. “Although it’s never too late to start saving, the best time to start contributing to retirement savings vehicles is when a person starts out in their career and may not have big financial commitments like a mortgage or childcare costs: and to find a way to maintain healthy savings habits as they age.”

Those employed by companies offering group RSP or pensions that allows employees to make contributions directly from their paycheque — and perhaps receiving a company match to their contributions — should fully take advantage of this and potential ‘free’ money, as it will assist their retirement nest egg in compounding over time, Williams said.

Americans more concerned about medical expenses in Retirement

Of those Canadians who plan to retire within five years, 86% expressed concerns about paying expenses in retirement. 27% of these Canadians nearing retirement ranked lifestyle as their top concern, compared to 17% of Americans.