Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

[Editor’s note: this blog originally appeared on the Hub in 2017 and is being republished in the wake of the Colonial Pipeline ransomware attack of 2021 and, just this week, JBS meat plants.]

In 2016 the University of Calgary got hacked. The university was hosting a conference with thousands of professors and on the first day problems started to appear with the databases.

The school’s IT department said this was due to a type of malware called ransomware. Before long, people on the campus had to communicate with one another via walkie-talkies, since the email system was suspended. Then it came back up again. How? The university paid the hackers a $20,000 ransom.

Both Windows and Mac PCs targeted

Although ransomware has been around for some time, it just now is becoming well known. It targets computer operating systems like Windows 7, 8 or 10 and Mac OS X, which means any organization using such operating systems is potentially vulnerable. And that’s a lot of organizations. Continue Reading…

What is one investment option that a small business should consider? Why?

To help your small business take on different investment options, we asked financial experts and small business leaders this question for their best investment ideas. From consulting a tax expert to getting into stocks and shares, there are several smart investment tips that may help your small business.

Here are eight investment options that small businesses should consider:

Learn About Objectives & Preferences

Consult an International Tax Expert

Invest in Your People

Help Fund Your Home Base

Find Companies That Improve Lives

Build Wealth with Index Funds

Think About Retirement Early

Get into Stocks and Shares

Learn About Objectives & Preferences

As any sound advisor will say, the best investment options for a small business truly are based on a personal situation. Some small businesses want more flexibility and control with their savings. Others are looking for less risk and fees. Before looking at investment options, small business owners should learn about their objectives and preferences. Then, they can see how investment options like life insurance or annuities can improve their financial position by safely growing their money while protecting it from tax and market risks. —Chris Abrams, Marcan Insurance

Consult an International Tax Expert

Investment options depend on a small business owner’s situation. Small business owners located overseas must understand that tax laws can differ considerably from country to country and impact their assets, financial accounts, and investments. That’s why consulting with an international tax attorney on issues like cross-border tax structuring, and compliance needs to be a part of the process. Investments aren’t just about the return; they’re also about the tax ramifications and savings by making the right choices. — Jason Kovan, International Tax Attorney

Invest in your People

Some of the most successful businesses tend to have a people-first mentality. An investment in people, whether that is putting in the time to make your customers happy or providing the resources necessary for happier employees, is an investment in your business’ success. If your customers are happy, they will recommend your business to their family and friends. If your employees are happy, they will be more willing to invest their time and efforts into the company’s goals and vision for the long term. — Brianna Vaughan, LendThrive

Help fund your Home Base

Invest in municipal bonds to help fund and develop your home base where most of your customers are located. These types of bonds offer a way to build interest while preserving your capital. They also have some tax benefits. Many municipal bonds are exempt from federal income tax as well as state and local taxes. — Rronniba Pemberton, Markitors

Find companies that Improve Lives

Investing in tech companies and products like ours helps to advance the industry and improve our daily lives. Predictive text and real-time spelling correction capabilities help to open doors for more opportunities not only for your business, but also your customers and employees who struggle with text. It also helps to improve overall productivity to maximize daily efforts. Continue Reading…

After the huge success of Cathie Woods and the ARK ETFs in 2020, rival investment managers have been quick to characterize technology funds as “Innovation” or “Disruption” products.

Such was the case on Thursday, as Invesco Canada Ltd. announced the launch of two new exchange-traded funds (ETFs) offering Canadian investors exposure to several relevant technology themes. This follows the February announcement from Franklin Templeton of the Franklin Innovation Fund (FINO), which appeared on the Hub under the headline Invest in Innovation, a Driver of Wealth Creation.

Both the words “Innovative” and “Disruptive” appear in the top of the press release for the debut of the Invesco NASDAQ Next Gen 100 Index ETF (QQJR and QQJR.F) and the Invesco NASDAQ 100 Equal Weight Index ETF (QQEQ and QQEQ.F. As the release says, these funds “build on the innovative solutions offered by Invesco and Nasdaq, allowing clients several distinctive entry points to own the disruptive companies listed on The Nasdaq Stock Market.”

Invesco also announced the launch of CAD Units of Invesco NASDAQ 100 Index ETF (QQC).

The Invesco innovation suite was launched in October 2020 and is just now expanding to Canada, with the following TSX-listed ETFs that started trading on the TSX today (Thursday, May 27). Of the three below, I find the equal weight Nasdaq 100 offering the most interesting:

Invesco NASDAQ Next Gen 100 Index ETF (QQJR and QQJR.F)

Invesco NASDAQ 100 Equal Weight Index ETF (QQEQ and QQEQ.F).

Invesco NASDAQ 100 Index ETF (QQC and QQC.F)

Pat Chiefalo

The innovation play was also highlighted in the following quote attributed to Pat Chiefalo, Head of Canada, Invesco ETFs & Indexed Strategies: “The launch of two new Invesco Nasdaq ETFs reaffirms the commitment of Invesco’s Canadian ETF business to providing our clients with products that access the themes and companies at the forefront of innovation … Now Canadian investors can choose several unique ways to gain exposure to the category-defining companies listed on The Nasdaq Stock Market.”

There are of course several existing rival plays on the top 100 Nasdaq companies apart from Invesco’s famous QQQs. Incidentally, Invesco says it recently changed the name of the Invesco QQQ Index ETF to the Invesco NASDAQ 100 Index ETF, dropping the management fee to 0.20% of NAV to “make it the most cost-effective ETF in Canada tracking the Nasdaq 100 Index.”

By contrast, the new QQJR and QQJR.F are relatively unique: it tracks the Nasdaq Next Generation 100 Index, which includes the “next 100” non-financial companies listed on The Nasdaq Stock Market, outside of the Nasdaq 100 Index, in a mid-cap ETF. Continue Reading…

When considering life insurance, the first thing that comes to mind is coverage for a single person. While that is the most commonly used option, there are many variants of the policy that you can use.

One of these variants is the joint life insurance policy. It is an option that covers two people instead of the one offered by a standard policy. These policies are usually targeted towards couples.

While having two separate policies is better overall, joint life insurance can come in handy in certain circumstances.

There are some important reasons for choosing joint life insurance. One of these is if your spouse does not qualify for an individual policy. It can also come in handy if you have people who depend on you or if you want to leave an inheritance for your heirs.

Most joint insurance policies are permanent and last your entire life. They contain an investment component that earns interest.

There are also a few joint policies that can be set up to last a certain amount of time but are rare.

Differences between Single and Joint Insurance policies

A single-life insurance policy provides coverage for a single soul, which is usually you or your significant other. The policy pays out if that soul passes away.

Conversely, a joint insurance policy provides coverage for 2 souls. It pays out if one of the policyholders passes away.

Joint insurance policies pay out only once when one of the covered individuals passes. This leaves the other person without coverage. Joint insurance policies cost more but provide more protection.

How do Joint Life Insurance policies work?

Joint life Insurance policies provide coverage for 2 people within the same policy. This is a cheaper alternative to buying two different policies. It also has its own unique set of bonuses.

Since it is cheaper, a joint policy will pay out only once, usually when the first person dies. In some cases, the policy can also pay out if one person is diagnosed with a terminal illness. The doctor must specify that person has less than a year to live.

The policy ends instantly when it pays out once. This leaves the other partner uncovered. This can be a problem if the surviving person is old and cannot afford a new policy.

Both the partners in a joint insurance policy are usually insured for the same amount. This ensures the payout is also similar when either person passes. Continue Reading…

Franklin Templeton Investments: Licensed from GettyImages

(Sponsor Content)

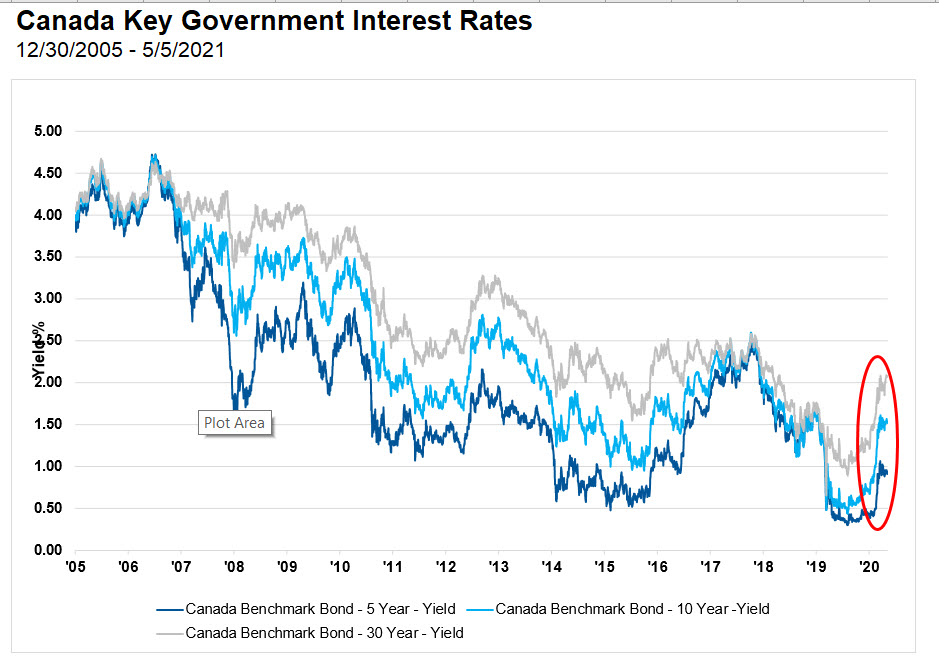

While many equity markets have performed well year to date, the last few months have not been as kind to fixed income investors. Last quarter, fixed income markets recorded some of the worst returns in 40 years as central banks and governments worldwide continued to rack up a mountain of debt in ongoing support of the global economy and consumers during the COVID-19 pandemic. But don’t despair; as Franklin Bissett fixed income portfolio manager Darcy Briggs points out in this Q&A, the market still offers value — if you know where to look.

Q: How would you describe the current environment for Canadian fixed income?

After seeing significant returns in Canadian fixed income last year, we expect more subdued performance in 2021. Given the year’s starting point of very low interest rates and tight credit spreads, we see corporate credit as offering the best risk-adjusted return opportunities in the current environment. As active, total return managers focused on generating income and capital gains, we know bond selection will remain important this year. Small interest rate moves can lead to significantly different outcomes for different fixed income sectors. Uncertainties remain high, and we are seeing a wide range of forecasts on how the balance of 2021 will unfold. Although interest rates have been up as much as 100 basis points so far this year, we think they may have overshot, as happens from time to time. We would not be surprised if they drifted lower later in the year. Realistically, we expect the path ahead to be a little messy.

Source: FactSet, Franklin Templeton

How so?

This recession/quasi-depression was prompted by a dramatic health crisis and the resulting government-mandated shutdown; it was not caused by normal business cycle dynamics. While fiscal and monetary policy have prevented a full-blown financial crisis, those tools have limited ability to solve the current recession. We believe it will end once the pandemic subsides and the economy fully opens, functioning in a more familiar pre-pandemic way. Vaccines are key to the pace of progress. Continue Reading…