Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

In my role as a Portfolio Manager, Financial Planner and President at TriDelta Private Wealth, the number one question that people ask is “Will I run out of money?”

This question comes from people with a $10 million net worth, a $3 million net worth, and a $300,000 net worth. There may be different levels of angst involved but they still wonder.

The fundamental issue is fear. Even if it isn’t rational, there is always a bit of fear about running out of money. Even if running out may mean different things to different people.

Of course, for those with more wealth, the related question is almost always “Am I paying too much in tax?” and “Is there tax smart things that I should be doing that I am not?”

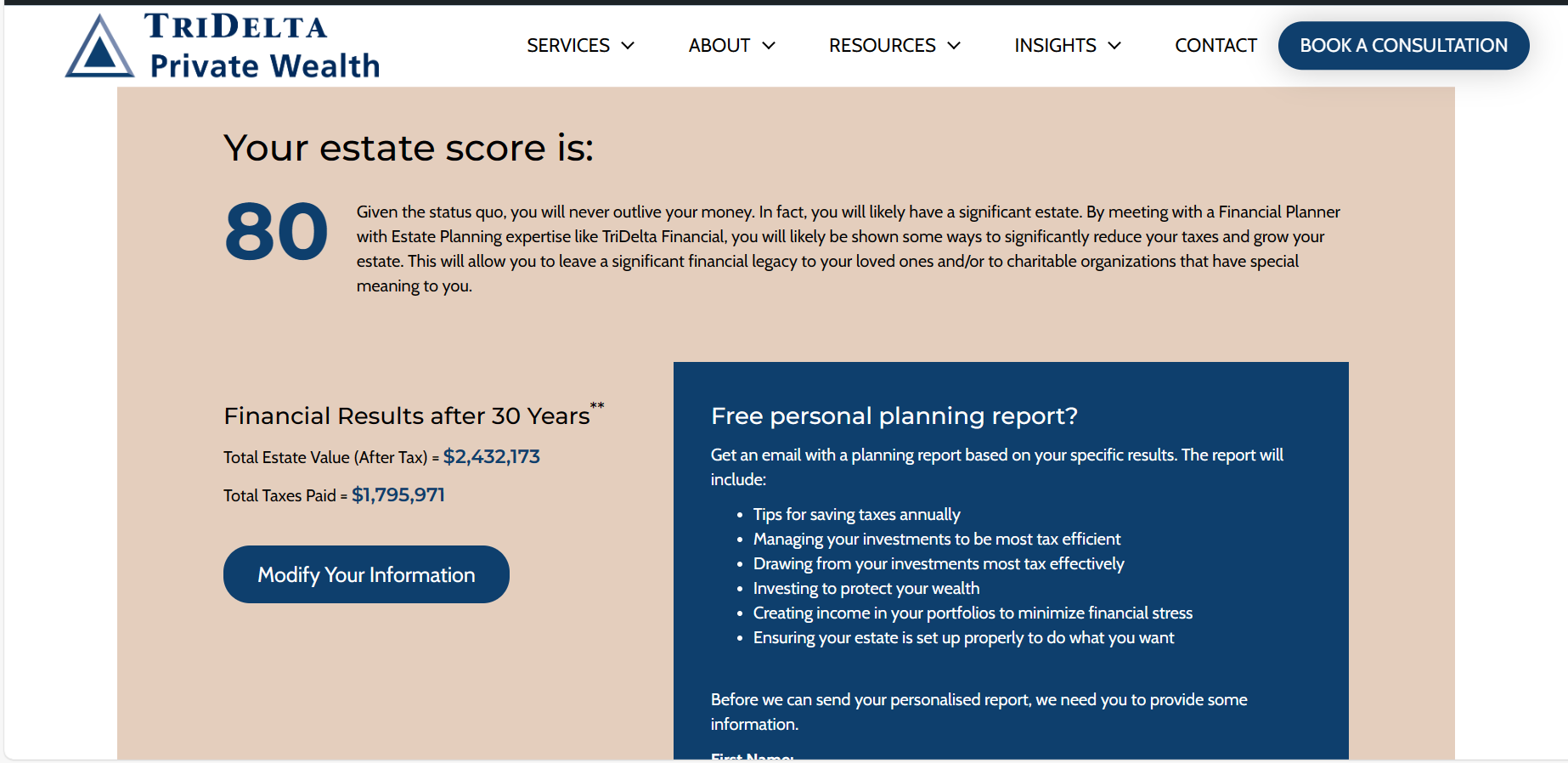

While we do a lot of work in each area with Canadians, we decided to build a free tool to help answer that number one question. We have done this through our TriDelta My Estate Value calculator. By someone entering in several core pieces of financial information, the calculator does some pretty heavy lifting. Behind the scenes are actuarial tables to show life expectancy, tax tables, and a variety of stated assumptions around inflation, real estate and investment growth expectations.

The output is an estimate of your likely estate value in future dollars, along with a lifetime estimate of your income taxes paid.

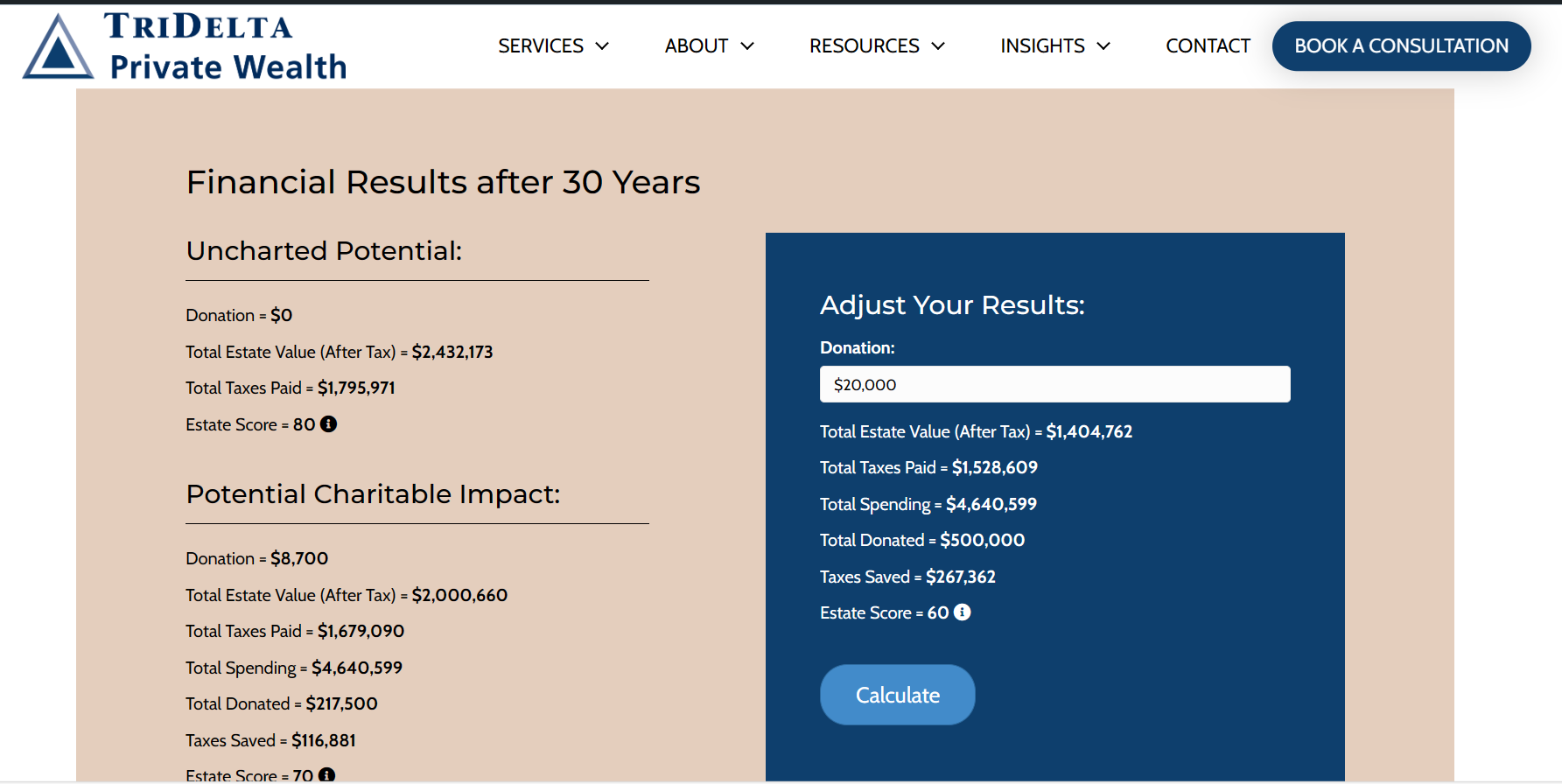

One other tool we have put together is a donation calculator. It takes the information from the My Estate Value calculator and provides some ability to see the impact of annual charitable giving. What if you gave $5,000 a year? What would be the impact to your likely estate value and to your lifetime tax bill? What if you gave $10,000 or $20,000 a year? One of the reasons that we put this together is that many Canadians would give more to charity of they felt confident that they could afford to do so. This calculator helps to show in real time the impact of higher levels of giving. The link is here: Donation Planner – TriDelta Private Wealth

We have found that even among the free tools online, most are focused on retirement savings, and deliver a monthly savings target. The My Estate Planner calculator is focused on the years after retirement, and what potential estate you will be leaving to your family and/or charity. Continue Reading…

Canada’s aging population means more retirees but most Canadians contemplating retiring say they would keep working if they could reduce their hours and stress. That was the top line of a Statistics Canada Daily release issued early in August. It was also the subject of a CBC Radio interview I conducted that aired in multiple cities on Thursday, Nov. 2. Here’s the link. Go to Episodes, then Nov. 2nd, then click on the line that says Canadians would choose to work past 65 under certain circumstances.

The interviewer is CBC Business columnist Rubina Ahmed-Haq, who focuses on money, workplace and financial wellness. The 4-minute interview with me and others touched on most of the topics this site does, including semi-retirement, entrepreneurship, Findependence and Victory Lap Retirement (the latter a book I co-authored with ex banker Mike Drak.). At the outset I clarified that I myself am still working at at 70, albeit self-employed through this web site and regular writing and editing for MoneySense.ca.

I was asked about the FIRE movement (Financial Independence/Retire Early) and I explained that while there are many FIRE proponents who claim to have “retired” in their 30s, in my experience these people have not really retired: rather, they have ceased to be salaried employees with the commuting grind, bosses and meetings and all that comes with it. Most have in reality become self-employed or semi-retired entrprepreneurs: in fact, many of the FIRE bloggers I have read are running web sites that accept advertising, and/or writing books that pay royalties and in some cases are on the speaking circuit accepting speaking fees. Having done all of these myself over the years, that’s not my idea of full retirement!

10% of 70-plus cohort still working at least part-time

Statistics Canada

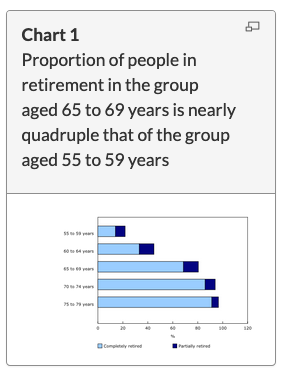

Going back to the Statistics Canada Daily, it reported that in June 2023, 21.8% of Canadians between ages 55 and 59 were either completely or partially retired. That doubles to 44.9% for those aged 60 to 64, and doubles again to 80.5% for those 65 to 69. By the time Canadians reach my age (70), it plateaus around 90% who are at least partially retired.

Interestingly, as I may have alluded to on-air, I can think of several people who are working well past 70, including some prominent journalists and financial gurus. I guess both are seen by proponents as a relatively satisfying occupation, particularly those who like myself do both by writing (or editing) about money.

Not surprisingly, for those who are completely retired, the main factor in determining the timing was financial: usually having qualified to start receiving pension benefits. This was cited by 35% of the men and 28.2% of the women who reported being completely retired.

Aspiring homeowners and families looking to invest in property often seek expert advice. To provide a range of perspectives, we’ve gathered sixteen pieces of advice from CEOs, founders, and other industry professionals. From understanding the market rather than chasing it, to securing a property warranty, this article offers a wealth of insights for property investment.

Understand, Don’t Chase, the Market

Consider Property’s Rentability

Diversify Your Real Estate Investments

Seek Immediate Return on Investment

Research and Plan Your Investment

Leverage Home Inspection Power

Invest in a Fixer-Upper

Consider Total Cost of Ownership

Have a Clear Exit Strategy

Start Small in Property Investment

Diversify Your Real Estate Portfolio

Think Long-Term for Value Appreciation

Look into Emerging Neighborhoods

Define Your Investment Goals

Establish a Clear Budget

Secure a Property Warranty

Understand, don’t chase, the Market

If there’s one piece of advice I consistently circle back to, it’s this: don’t just chase the market, understand it. Now, that might sound a bit cliche, but let me unpack that for you with an example and a personal anecdote.

Many aspiring homeowners or investors get drawn into this frenzy of buying property anywhere there’s a buzz. You know, a new major employer coming into the area, a big infrastructure project announcement, or maybe where there’s a sudden spike in property values. But here’s the twist: not every “hot” market is suitable for every investor. — Shri Ganeshram, CEO and Founder, Awning.com

Consider Property’s Rentability

I’d suggest considering the “rentability” of the property. If your circumstances change and you need to move, having a property that’s attractive to renters can provide a steady income stream.

Look for properties with features that are in high demand in the rental market, such as a good layout, modern amenities, and proximity to employment centers. I’ve seen clients turn unexpected relocations into opportunities by choosing properties that are easy to rent, thereby securing a secondary income source. — Alexander Capozzolo, CEO, SD House Guys

Diversify your Real Estate Investments

Different types of real estate investments, such as residential properties, commercial properties, or vacation rentals, can react differently to market fluctuations. By spreading your investments across various property types, I’ve seen how it can reduce the overall risk associated with real estate investing.

I’ve witnessed that diversification can provide a more stable income stream. For instance, while one property might experience a vacancy, another may continue to generate rental income.

I’ve found that different markets may perform differently at various times. By advising clients to invest in properties in different geographic locations, I’ve seen them benefit from a broader range of market conditions. — Ritika Asrani, Owner and Head Broker, St Maarten Real Estate

Seek Immediate Return on Investment

One piece of real estate investment advice I’d give is to focus on buying property that can give you a return on investment (ROI) immediately. That’s because when interest rates are high, property prices decrease, making it harder to know what kind of appreciation you can expect in the future.

As a bonus tip, invest where there are median-priced homes to maximize your returns. For example, if you invest in a $300,000 house with an 8% versus a 4% interest rate, the mortgage difference would be just $615 per month.

On the other hand, if you invest in a $1 million property with the same interest rates (8% versus 4%), the mortgage difference you’d pay would be over $2,000 per month.

Ultimately, to maximize your returns and minimize risk as an investor, buy properties that will give you cash flow from day one and limit your mortgage payments. — Ryan Chaw, Founder and Real Estate Investor, Newbie Real Estate Investing

Research and Plan your Investment

Thoroughly research the local real estate market dynamics. Understand not only current property values but also potential growth or decline in the area. In our global property management experience, we’ve seen the value in choosing properties located in areas with growing job opportunities, infrastructure development, and a strong community presence.

Additionally, always factor in the long-term perspective: real estate typically appreciates over time, so patience and a well-planned strategy can yield returns. Consider your investment goals and financial capabilities carefully. Determine whether you seek rental income, capital appreciation, or both. Calculate a budget, including property purchase, maintenance, and potential vacancies.

Finally, don’t underestimate the significance of a property management company, especially if investing in different locations or operating remotely. Their expertise can help navigate property investment complexities and ensure your investment thrives. — Johan Hajji, CEO and Founder, UpperKey

Leverage Home Inspection Power

One tip I’d offer is to leverage the power of “home inspection” before finalizing any deal. A thorough inspection can reveal potential issues like structural damage or outdated electrical systems, allowing you to either negotiate the price or avoid a money pit.

I‘ve had clients who saved thousands by using the findings of a home inspection to negotiate a lower purchase price, turning what could have been a costly mistake into a savvy investment. — Gagan Saini, CEO, JIT Home Buyers

Invest in a Fixer-Upper

My career in remodeling and carpentry started with a real estate investment. I bought a home in disrepair for very little money and began piecing it together, learning how to perform various construction tasks along the way.

At first, I just got one room livable. Then, at night and on weekends, piece by piece, I finished the kitchen, then the bathroom, then the basement. If you enjoy problem-solving and working with your hands, you’ll enjoy a fixer-upper much more than a property that you paint and resell. — Rick Berres, Owner, Honey-Doers

Consider Total Cost of Ownership

One piece of advice would be to think long term and consider the “total cost of ownership,” not just the purchase price. This includes property taxes, maintenance, and potential homeowner association (HOA) fees.

I recommend it to create a detailed budget that accounts for these ongoing costs to ensure the investment is sustainable in the long run. Clients who’ve taken this holistic approach have been better prepared for the financial responsibilities of property ownership, avoiding unexpected financial strain down the line. — Erik Wright, CEO, New Horizon Home Buyers

Have a Clear Exit Strategy

Have a solid exit plan from the get-go. It’s not just about buying a property; it’s about understanding how you’re going to profit from it. Are you looking for long-term rental income, or do you plan to flip the property for a quick return?

Having a clear strategy helps you make informed decisions and ensures that your investment aligns with your financial goals. Real estate can be a fantastic wealth-building tool, but knowing your exit strategy keeps you on the right path to success. — Loren Howard, Founder, Prime Plus Mortgages

Start Small in Property Investment

Start small. For aspiring homeowners or families looking to invest in property, it is important to start small. While it may be tempting to jump into a larger, more expensive property as your first investment, starting with a smaller and more affordable property can be a smarter financial decision in the long run.

By starting small, you will have less risk and financial burden, allowing you to learn and gain experience in the real estate market without being overwhelmed. Additionally, starting small will also give you a better understanding of your financial capabilities and help you make more informed decisions for future investments.

Furthermore, starting with a smaller property can also provide potential for quicker returns on investment. With lower purchase prices and potentially lower maintenance costs, you may be able to see profits sooner than with a larger, more expensive property. — Keith Sant, CMO, Eazy House Sale

Diversify your Real Estate Portfolio

I would advise diversifying your portfolio if you’re searching for real estate investment tips. Think about making investments in a variety of real estate, including commercial, residential, and even holiday rentals. This diversification can create several income streams while reducing risk. Continue Reading…

When it comes to investment strategies, dividend or income investing holds a special place in the hearts of many investors, especially retirees. It’s not surprising, considering that dividends often constitute a substantial portion of a portfolio’s total return. Let’s dive into this popular approach and understand how Exchange-Traded Funds (ETFs) can be a game-changer.

The Dividend Advantage

Now, let’s dissect the significance of dividends in the realm of equity returns. Looking over the long-haul equity return expectations, the S&P has returned an average of around eight per cent over a 40+ year period[i]. In historical context, dividends have accounted for a significant portion of this return, ranging from three to four per cent. This underscores how dividends contribute almost half of the total equity market return annually[ii]. However, their true power lies in compounding. While you collect dividends each year, reinvesting them into equities sets the stage for exponential growth. This compounding effect is what propels your portfolio to higher echelons of growth.

Moreover, dividends are more than just monetary gains; they serve as a vital indicator of a company’s financial health. While not the sole indicator, companies with robust dividend policies often signal financial stability. It’s crucial to note, however, that not all dividends are created equal, a distinction we’ll explore further.

The Art of Portfolio Construction

We’ve witnessed a surge of interest in dividends: evident in the significant influx of investments into the dividend space. But what are the actual benefits of incorporating dividend investments into your portfolio?

From a portfolio construction perspective, the benefits of including dividend-paying stocks are evident. We’ve examined 32 years of returns across various companies in the Canadian equity market. Dividing them into dividend growers, dividend payers, dividend cutters, and non-dividend payers, a clear pattern emerges.

The standout performers are the dividend Growers, showcasing the potential of quality dividend-paying stocks. Over this period, they have consistently outperformed the broad index, offering a higher average return. Moreover, when it comes to managing risk, dividend Growers and high-quality dividend payers exhibit a slightly lower level of volatility compared to the broader market. This suggests that a focus on sustainable, high-quality dividend stocks can lead to both enhanced returns and a controlled risk profile, making them a compelling addition to a well-rounded investment portfolio. It’s worth noting that not all dividends are created equal, and a discerning approach is crucial for maximizing the benefits of dividend investing.

Ensuring Sustainable Dividends

One of the crucial aspects of dividend investing is ensuring the sustainability of the payouts. Stepping into the shoes of a prudent investor, it’s imperative to avoid falling into yield traps: companies offering high yields but lacking the financial backing to sustain them. Enter the analysis of a company’s overall health, a task made easier by assessing key metrics.

Cash as a percentage of total assets and payout ratios are key indicators of a company’s financial fortitude. In recent times, the top quartile of companies has seen a surge in cash reserves, an encouraging sign of their resilience. Moreover, evaluating the payout ratio provides insights into the sustainability of dividends. A company paying out more than it earns in the long run is walking on thin ice, whereas those with ratios in the 40-50% range are on relative solid ground.

Dividends in an Age of Inflation

Amid the specter of inflation, dividend strategies have shone brightly. Companies with robust dividend policies, characterized by stable cash flows, have weathered the storm far better than their growth-oriented counterparts. Inflation, while posing challenges to certain sectors, has not dampened the dividend-driven approach. In fact, historical data (monthly excess returns over the MSCI World Index for the last 45 + years) indicates that dividend-paying companies fare even better in high CPI environments, providing a reliable anchor for portfolios.

At the heart of the resilience of dividend-paying companies lies their ability to generate steady and predictable cash flows. These companies often operate in industries with stable demand for their products or services, which provides a buffer against the uncertainties associated with inflation. By virtue of their financial stability, they’re better positioned to maintain and perhaps even grow their dividend payouts, providing a reliable source of income for investors.

Historical data, tracked against the Consumer Price Index (CPI) reinforces the notion that dividend-paying companies can act as a reliable anchor for portfolios during inflationary periods. These companies tend to exhibit a degree of insulation from the market volatility often associated with rising prices. By consistently delivering returns through dividends, they offer investors a source of stability in an otherwise uncertain economic environment.

Methodology Matters

In the realm of Dividend ETFs, the choices are vast, and not all ETFs are created equal. Each comes with its unique methodology, impacting performance. Factors such as weighting methodology, sector caps, and company quality screenings play pivotal roles in the outcome. This underscores the importance of understanding the underlying strategy before investing. Continue Reading…

Why Harvest ETFs chose to launch its own U.S. Treasury ETF that offers the security of U.S. Treasury Bonds and high monthly income

Image courtesy Harvest ETFs/Shutterstock

By Ambrose O’Callaghan

(Sponsor Content)

The early part of this decade saw the introduction of significant monetary interventions that rivalled the policies pursued by central banks following the Great Recession of 2007-2009. Policymakers were able to resuscitate markets in the face of a global pandemic. However, the end of the pandemic saw the beginning of a surge in inflation rates not seen in many decades.

Central banks responded to soaring inflation with the most aggressive interest rate tightening policy since the early 2000s. Policymakers are encouraged with the result of inflation coming down, but a highly leveraged consumer base has been squeezed by the upward revision in borrowing rates. Moreover, the higher interest rate environment has spurred stock market volatility. That has led to a shift investors’ focus, with investors focusing on capital preservation instead of capital appreciation.

Harvest ETFs’ investment management team believes that we are at or near the peak of the current interest rate tightening cycle. In this climate, the prudent investment strategy will factor in high interest rates while preparing for the eventual downward move that many experts and analysts are projecting for 2024.

Why should you consider exposure to U.S. Treasuries?

Canadian consumers might not be celebrating the rise of interest rates. However, the switch to higher rates could be good news for Canadian savers. Continue Reading…

By Ted Rechtshaffen, CFP

By Ted Rechtshaffen, CFP One other tool we have put together is a donation calculator. It takes the information from the My Estate Value calculator and provides some ability to see the impact of annual charitable giving. What if you gave $5,000 a year? What would be the impact to your likely estate value and to your lifetime tax bill? What if you gave $10,000 or $20,000 a year? One of the reasons that we put this together is that many Canadians would give more to charity of they felt confident that they could afford to do so. This calculator helps to show in real time the impact of higher levels of giving. The link is here: Donation Planner – TriDelta Private Wealth

One other tool we have put together is a donation calculator. It takes the information from the My Estate Value calculator and provides some ability to see the impact of annual charitable giving. What if you gave $5,000 a year? What would be the impact to your likely estate value and to your lifetime tax bill? What if you gave $10,000 or $20,000 a year? One of the reasons that we put this together is that many Canadians would give more to charity of they felt confident that they could afford to do so. This calculator helps to show in real time the impact of higher levels of giving. The link is here: Donation Planner – TriDelta Private Wealth