By Ted Rechtshaffen, CFP

By Ted Rechtshaffen, CFP

Special to Financial Independence Hub

In my role as a Portfolio Manager, Financial Planner and President at TriDelta Private Wealth, the number one question that people ask is “Will I run out of money?”

This question comes from people with a $10 million net worth, a $3 million net worth, and a $300,000 net worth. There may be different levels of angst involved but they still wonder.

The fundamental issue is fear. Even if it isn’t rational, there is always a bit of fear about running out of money. Even if running out may mean different things to different people.

Of course, for those with more wealth, the related question is almost always “Am I paying too much in tax?” and “Is there tax smart things that I should be doing that I am not?”

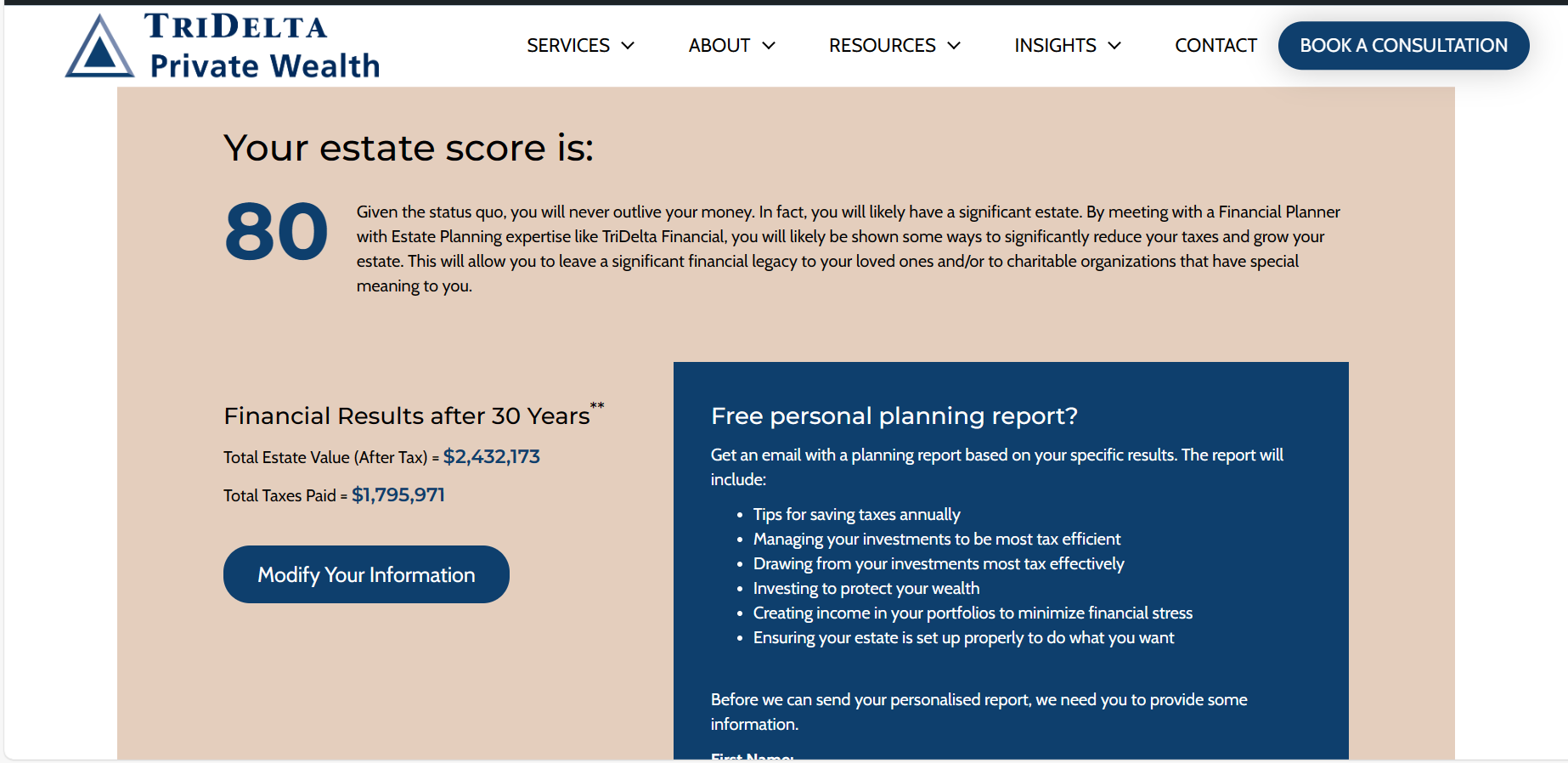

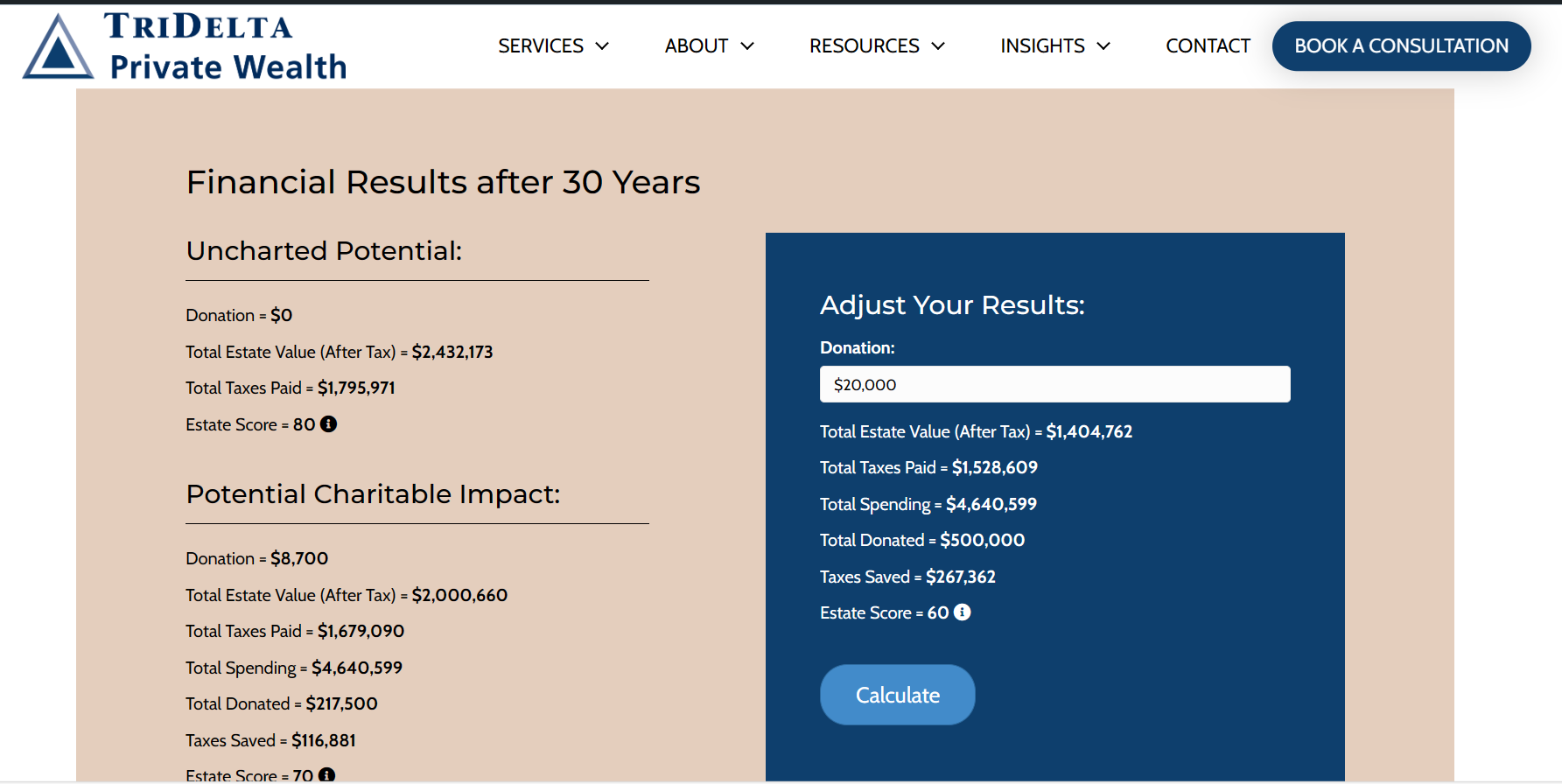

While we do a lot of work in each area with Canadians, we decided to build a free tool to help answer that number one question. We have done this through our TriDelta My Estate Value calculator. By someone entering in several core pieces of financial information, the calculator does some pretty heavy lifting. Behind the scenes are actuarial tables to show life expectancy, tax tables, and a variety of stated assumptions around inflation, real estate and investment growth expectations.

The output is an estimate of your likely estate value in future dollars, along with a lifetime estimate of your income taxes paid.

You will find the calculator here:

My Estate Value Calculator – TriDelta Private Wealth

Donation Calculator

One other tool we have put together is a donation calculator. It takes the information from the My Estate Value calculator and provides some ability to see the impact of annual charitable giving. What if you gave $5,000 a year? What would be the impact to your likely estate value and to your lifetime tax bill? What if you gave $10,000 or $20,000 a year? One of the reasons that we put this together is that many Canadians would give more to charity of they felt confident that they could afford to do so. This calculator helps to show in real time the impact of higher levels of giving. The link is here: Donation Planner – TriDelta Private Wealth

One other tool we have put together is a donation calculator. It takes the information from the My Estate Value calculator and provides some ability to see the impact of annual charitable giving. What if you gave $5,000 a year? What would be the impact to your likely estate value and to your lifetime tax bill? What if you gave $10,000 or $20,000 a year? One of the reasons that we put this together is that many Canadians would give more to charity of they felt confident that they could afford to do so. This calculator helps to show in real time the impact of higher levels of giving. The link is here: Donation Planner – TriDelta Private Wealth

We have found that even among the free tools online, most are focused on retirement savings, and deliver a monthly savings target. The My Estate Planner calculator is focused on the years after retirement, and what potential estate you will be leaving to your family and/or charity. Continue Reading…