Once you achieve Financial Independence, you may choose to leave salaried employment but with decades of vibrant life ahead, it’s too soon to do nothing. The new stage of life between traditional employment and Full Retirement we call Victory Lap, or Victory Lap Retirement (also the title of a new book to be published in August 2016. You can pre-order now at VictoryLapRetirement.com). You may choose to start a business, go back to school or launch an Encore Act or Legacy Career. Perhaps you become a free agent, consultant, freelance writer or to change careers and re-enter the corporate world or government.

The task of retirement income planning can be overwhelming for Canadians as they get closer to leaving the workforce. Making the right decisions can be difficult with all the possible sources of income they might have, including Old Age Security (OAS) and Canada Pension Plan (CPP), and of course, Canada’s complex tax codes don’t make it any easier. People need help.

Cascades is a Canadian retirement income calculator that takes the difficulty out of retirement income planning. In many cases it saves retirees hundreds of thousands of dollars in income tax, while showing a year-over-year road map guiding them through retirement. Who wouldn’t want to save money? But in some cases, like the one highlighted below, it’s not about extra tax savings: it’s about having enough money to last your entire retirement.

Bob and Ann’s story is based on a real-life case we came across last week, and it’s a great example of why proper retirement income planning is so important.

Meet retiree Bob, 65, and Ann, 56, still working

Bob is currently 65 and has been retired for 2 years. He was self-employed as a cabinet maker and still has his shop at home where he works part time bringing in $12,000 annually. Because he was self- employed, Bob has no defined benefit or defined contribution pensions. He currently holds about $250,000 in his RRSP, $15,500 in his TFSA, and $50,000 in a non-registered account. Bob receives close to max CPP at $12,600 and $7,248 from OAS.

Ann is originally from the United States and met Bob while he was vacationing in Florida. She is currently 56 and plans on retiring at 63 from her job as a logistics coordinator for an auto parts manufacturer. Ann brings in $57,500 annually and has a defined contribution pension currently worth about $140,000. Ann has no other savings apart from her defined contribution pension, but will receive $4,800 in CPP that she plans to start receiving as soon as she retires at 63. Because Ann hasn’t been in Canada for 40 years since the age of 18, she will only receive $3,500 annually from OAS.

It’s a fear or suggestion that we hear repeated quite often. The massive cohort of retiring baby boomers will need to sell their stocks to create income and that will crash the stock markets.

Or let’s just say it could cause a slow bleed, taking down or suppressing the stock markets over the coming decades. As you may know the the stock market is, well, a market: it simply lines up the buyers and sellers and when there are more sellers than buyers the price of the stocks will decline.

When we hear the numbers on the baby boomers and more specifically how many boomers will retire each day, it’s often the US numbers that are repeated. When it comes to financial markets it is often very US-centric.

There were 77 million Baby Boomers born between 1947 and 1964, roughly 4.5 million per year. Some doomsayers are predicting the Boomers will drain the equity markets of their capital once they retire. Should you worry? Are your equity portfolios at risk?

It’s now predicted that there are 10,000 baby boomers retiring (in the US) each day. Now when the AARP releases figures such as that they simply use age 65 as a retirement date. Perhaps that’s not a bad benchmark but so many will retire well before age 65, and many more will not retire until well into their 70s and beyond. Many will not retire at all; they’ll continue with part time work. Baby boomers are known for being quite entrepreneurial.

And then, not all retiring baby boomers are going to go out and sell all of their stocks on their 65th birthdays. The public and private pension managers are not going to aggressively sell out of their US stock positions. Pensions hold well-diversified portfolios of US and International stocks and bonds and that also includes massive exposure to private equity: assets that are not ‘in’ the stock markets.

Why the boomers won’t crash the markets

The markets are mostly efficient and they factor in all available information with respect to individual stocks, economies and larger trends. It’s not news that North America is getting ‘older.’ That’s already priced in to the markets.

There is a heavy concentration of US stock ownership by more wealthy US citizens. The challenge for many may not be how fast can they sell their stocks but what to do with all of this wealth. Also, baby boomers are about to inherit over $15 trillion over the next 20 years. That will reduce or eliminate the need to sell those stock shares. You’ll find that, and some other interesting baby boomer stats in this Fool article.

I’ve been writing on Seeking Alpha for quite some time, and the readership is largely quite affluent. Many of these American boomer investors write more of accumulating more stocks in the retirement stage. In Retirees Don’t Say No When The Market Offers You A Nice Bonus I linked to a study that confirms that more affluent US retirees don’t spend down their retirement assets. They even become ‘savers.’

It’s a continual theme as well that many of these retirees ‘live off of the dividends.’ They’re not selling shares; they are simply collecting and spending the dividends. They will not put sell pressure on the markets.

New buyers

The millennial generation is even larger than the Baby Boomers and they will enter their accumulation stage and will be buyers of stock assets directly and by way of their pensions. There will be demand for stocks from younger generations. The Washington Post stated that the millennials will overtake the Boomers in 2019. We also have those echo-boomers and Gen-X’ers stepping in.

Bond yields are low; investors and pension managers know that they need those stocks for the longer term growth potential. Of course, we can often get greater income (and growing income) from stock dividends compared to bonds. The low yield environment also affects those newer and current accumulators as well as they may choose to shun low yielding bonds and embrace more stock exposure.

And if we look to the past and to studies, historically the correlation between age and asset prices is weak according to this white paper … Continue Reading…

Should you withdraw the Commuted Value of your Defined-Benefit Pension?

No. There are some exceptions, but the answer is almost always no. In fact, if a financial advisor is pushing you to pull out the commuted value of your pension, that’s a sign that you’re likely working with a bad advisor.

There is almost no chance that your advisor will choose investments that outperform a pension fund, mainly because the total fees you pay with an advisor are so much higher than the fees charged within a pension fund.

Some advisors will tell you that you won’t pay any fees because the mutual funds pay the advisor. Don’t believe this. Mutual funds and advisors get paid out of your savings.

Further, defined-benefit pensions have the advantage of handling longevity risk. Pension funds can afford to pay you based on your expected life span, and they’ll keep paying if you happen to live long. With an advisor managing your money, you need to hold back on your spending in case you live long.

Where it might make sense to take the commuted value

There are some cases where it makes sense to withdraw your pension’s commuted value. Here are a few:

1. Poor health makes you likely to die much younger than average. In this case, taking the commuted value allows you to spend more now or leave a larger legacy. Continue Reading…

By Billy and Akaisha Kaderli, RetireEarlyLifestyle.com

Special to the Financial Independence Hub

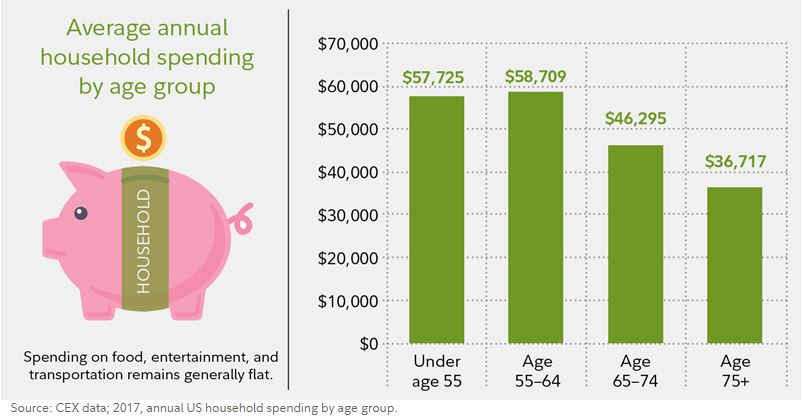

We know many of our readers are not “average.” However, if average Joe can support his retirement on as little as US$200,000 savings, imagine what you can do with the amount you have!

By reading the chart below, you can see that the average spending for retirement households age 65 – 74 is US$46,000.

It is tough to make that $46k amount with only Joe’s savings, so what should he do?

Social Security

The average recipient today (in the United States) collects US$1,461 a month, or US$17,532 a year. Joe’s SS check is average and he has a wife who also collects the average Social Security amount.

$17,532 times 2 (people) = US$35,000 per year.

Not quite the $46,000 that they need but getting closer.

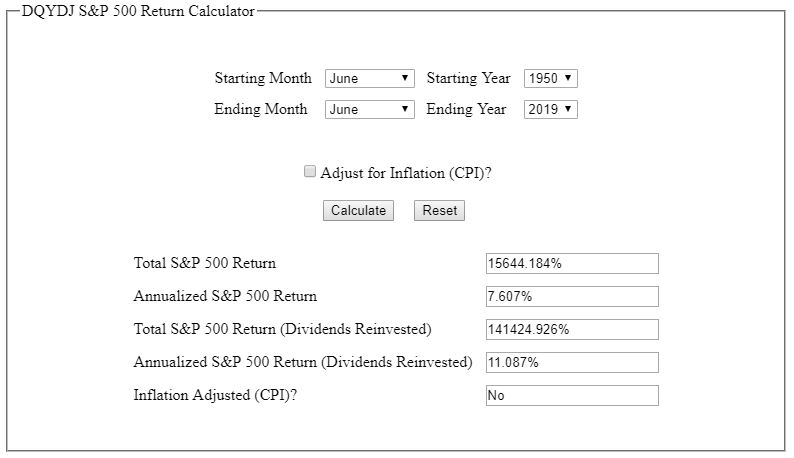

Hopefully, Joe has his retirement money invested in VTI (Vanguard Total Stock Market) or SPY (S&P 500 Index) and is making market gains equaling around 10% annually.

Here you can see that since the 1950’s — about when Joe was born — the S&P 500 has had an annualized return of over 11%, dividends reinvested, but let’s use 10% as a more conservative projection.

Remember, Joe has to make up $11,000 to match his average spending ($46,000). But let’s give Joe an extra one thousand dollars per year so he can pamper Mrs. Joe with occasional gifts and dinners out.

So, he needs $12,000 out of the $200,000 in savings per year to make up the difference in spending. That’s an extra $1.000 per month.

Invested in the S&P 500 — based on 69 years of returns and using 10% as the annual return — after his first year he would have $220,000 minus $12,000 withdrawal = $208,000.

Now Joe has $47,000 in annual income: $35,000 from Social Security and $12,000 from investments.

Plus, his $200,000 has grown to $208,000, a 4% gain outpacing inflation at the current rate of less than 2% per year.

Their Social Security payment is also indexed to inflation so as inflation rises, so will their Social Security. Continue Reading…

My latest MoneySense Retired Money column has just been published. It looks at the reversal the past year in interest rates, which impacts seniors who had started to look forward to at least half-decent GIC rates near 3%. You can find the full piece by clicking on the highlighted headline: Are GICs right for retirees looking for Fixed Income?

Short of embracing high-yielding dividend paying stocks, the more palatable alternative for conservative retirees might be fixed-income ETFs. The article focuses on a recent video by CFA Charterholder Benjamin Felix, an Ottawa-based portfolio manager for PWL Capital. Felix argues that at a minimum such investors should have a mix of both fixed-income ETFs and GIC ladders.

The latter let you sleep at night because they are invariably “in the green” in investment accounts. But while in the short term fixed-income ETFs can be in the red — just like equity ETFs — Felix makes a compelling argument for the higher potential returns of bond ETFs.

Felix believes that what really matters for investors is total return: “Holding a lower-rate GIC after a rate increase still results in an economic loss.” Bond returns consist of principal, interest payments and reinvested interest, so focusing only on return of principal misses the point. Individual bonds are not ideal for individual investors, as they require extensive research, are relatively expensive and tricky to trade.

Short-term GICs miss out on the term premium

But short-term GICs miss out on the term premium, which is substantial over time. Going back to 1985, Felix says short-term bonds returned 6.51% annualized versus 7.97% for the aggregate bond universe (which includes some short-term bonds). This shows how much mid- and long-term bonds bring up the overall return. To be clear, this period captures one of the greatest bond markets in history but Felix says it is still reasonable to expect a relationship between riskier longer-term bonds and higher expected bond returns. Risk and return should be related.

GICs are also illiquid, so even if an investor chooses to include GICs in a portfolio, they will generally also include bond ETFs, which – like stock ETFs – can be sold any trading day. Nor do GICs provide exposure to global bonds.

Of course, a nice alternative are those asset allocation ETFs we have often discussed on this site. See for example this excellent overview by CutthecrapInvesting’s Dale Roberts: Which All-in-One, One-Ticket Portfolio is right for you?

The Felix video can be found at his Common Sense Investing YouTube series here.

By Ian Moyer

By Ian Moyer