By Hamilton ETFs

(Sponsor Blog)

International equities continue to be in focus. As global market leadership broadens, Canadian investors are paying closer attention to geographic diversification and opportunities beyond North America. International stocks, which outperformed the U.S. stock market in 2025, have continued to attract attention as the geopolitical landscape evolves.

So far this year, Canadians have poured $22.8 billion into international equity ETFs, according to National Bank of Canada Capital Markets[1]. In contrast, they directed just $13.4 billion to Canadian equity funds and $11.3 billion to U.S. equity funds, over the same period.

Recent market performance has helped reinforce this trend. Since December 31, 2024, the MSCI EAFE Index rallied 40.5% compared to 24.6% for the S&P 500[2].

This combination of improved relative performance and more attractive valuations has helped bring international equities back into focus for investors looking to broaden exposure beyond North America. This shift has also been reflected in market commentary. Yardeni Research began recommending a “Go Global” approach in December 2025, after more than a decade of favouring a “Stay Home” allocation. “So far this year, the U.S. has been among the laggards in the global performance derby,” he wrote in a research note published April 27, 2026.

Canadian investors have plenty of options for accessing international equity exposure. Yet for those seeking attractive, tax-efficient monthly income from developed markets outside North America, the available solutions have been far more limited. That’s why we’re closing that gap with the Hamilton International Equity YIELD MAXIMIZER™ ETF (IMAX).

Introducing IMAX

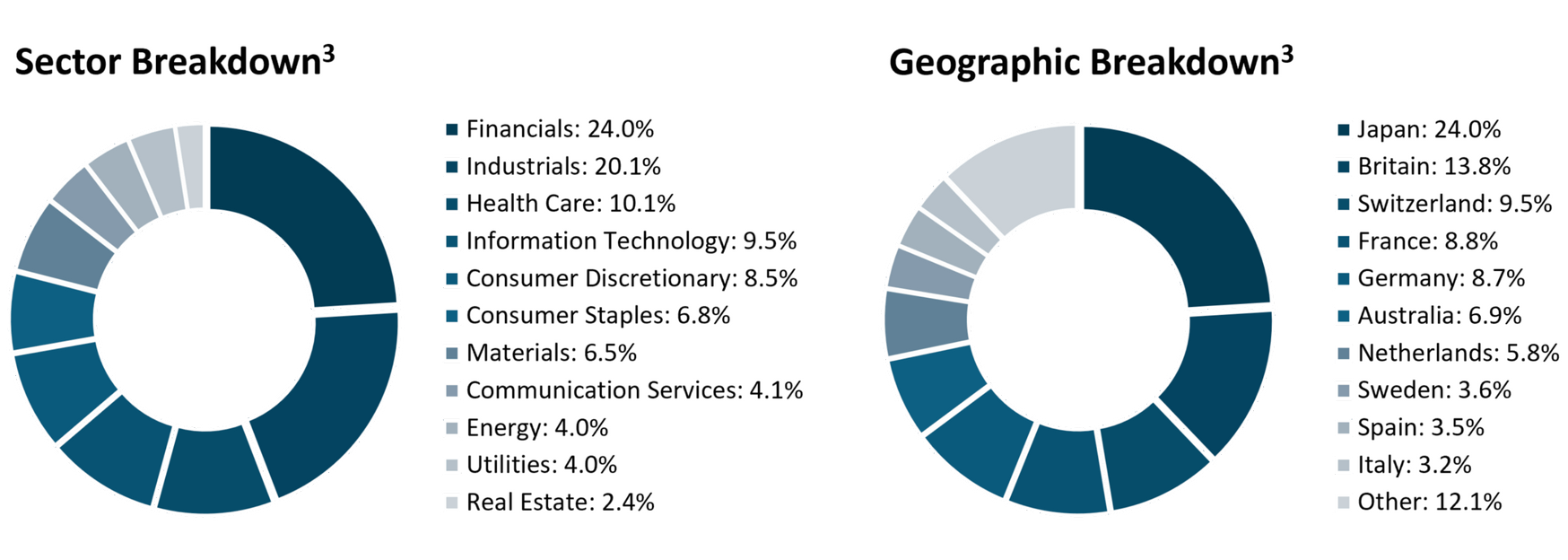

IMAX is designed for investors seeking diversified international equity exposure paired with attractive, tax-efficient monthly income. To achieve this, IMAX holds ETFs that provide exposure to both the MSCI EAFE Index and MSCI EAFE IMI Index and overlays a covered call strategy on a portion of the portfolio. The MSCI EAFE Index captures developed markets outside the U.S. and Canada.

International and global covered call ETFs remain relatively limited in Canada. The few available strategies often have significant geographic concentrations, such as Europe or the U.S., or provide exposure to a narrower group of companies through concentrated portfolios. By contrast, IMAX offers broad developed market exposure specifically outside North America. Through this approach, investors gain exposure to more than 2,500 large-, mid- and small-cap equities across markets including Japan, Britain, Switzerland, France, Germany and Australia.

To help generate monthly income, IMAX employs an actively managed covered call strategy overseen by our experienced options team. Like the other ETFs in our YIELD MAXIMIZER™ suite, IMAX utilizes an income first approach that primarily writes at-the-money call options in an effort to generate higher option premiums to provide enhanced cash flow potential. The strategy also maintains a flexible coverage ratio, allowing the portfolio management team to balance monthly income generation with long-term capital appreciation potential.

Importantly, IMAX helps provide tax efficient income, as options premiums are generally taxed as capital gains and/or return of capital.

Going Global with IMAX

Diversification is one of the most important principles of portfolio construction, and it applies not only across asset classes (stocks, bonds, commodities etc.), sectors and market capitalizations, but also regions. Continue Reading…