Once you achieve Financial Independence, you may choose to leave salaried employment but with decades of vibrant life ahead, it’s too soon to do nothing. The new stage of life between traditional employment and Full Retirement we call Victory Lap, or Victory Lap Retirement (also the title of a new book to be published in August 2016. You can pre-order now at VictoryLapRetirement.com). You may choose to start a business, go back to school or launch an Encore Act or Legacy Career. Perhaps you become a free agent, consultant, freelance writer or to change careers and re-enter the corporate world or government.

Looking to get out of your business as soon as possible? Our tips will help you sell your business quickly while still getting a fair deal.

Adobe Image by Robert Kneschke

By Dan Coconate

Special to Financial Independence Hub

Are you a small business owner ready to start the next phase of your life? If you’re looking to sellyour businessquickly and move on, read on.

We have some helpful strategies for attracting serious buyers and closing deals below.

Get your House in Order

The first thing you should do before putting the “For Sale” sign on your business’s front lawn is to get your organization and financial records in order. One of the first things that any potential buyer will want to look at is the accounts and books of the business to gauge its financial health.

If the documents and accounts are a disorganized mess that only you can decipher, your business won’t be very appealing to a buyer. Ensure your financial documents are organized and straightforward, including critical documents like the complete list of all assets, copies of patents and licenses, and profit and loss statements.

Hire a Business Broker

As you prepare for a sale, hiring an independent business broker is one of the best strategiesforselling yourbusinessquickly. A broker will take a commission from the sale, but their experience and skills are invaluable when selling a private practice or business.

They’ll connect you with more potential targets and get the word out that you’re looking to sell and vet buyers for you. They’ll also represent you in negotiations and offer valuable insight to attain the best deal as quickly as possible.

Sell to a Competitor

While it may sting the pride of some to sell their business to the competition, it’s often the fastest and easiest option for small business owners. After all, what competitor wouldn’t be interested in expanding and bringing their competition under their umbrella? Continue Reading…

Uncover good companies for long-term investments and you will boost your portfolio returns over time. Learn more here and discover one of our top picks.

Long-term stock investment strategies aren’t built to make a fast dollar. They are built to prosper over time, and most importantly, teach you how to pick the right stocks.

In our view, your goal as an investor, particularly if you follow a conservative investing strategy like the one we recommend, is to make an attractive return on your investments over a period of years or decades. Failure means making bad investments that leave you with meager profits or losses. Continue reading to learn about good companies for long-term investments.

Visa Inc., symbol V on New York, is on our list of good companies for long-term investments

Visa has been a terrific performer for our subscribers since we first recommended the stock at $19 (adjusted for share splits) in the December 2010 issue of our Wall Street Stock Forecaster newsletter.

A big part of Visa’s appeal is that it gets most of its revenue from the fees it charges card issuers and merchants using its network. This unique business model means the banks — and not Visa — are responsible for evaluating customer creditworthiness and collecting payments, which helps to cut risk for investors.

The company first sold its stock to the public at $11 a share in March 2008. We held off recommending it at that time, as the best way to cut the risk of investing in initial public offerings is to wait till after the next market slump and/or recession comes along. Thanks to Visa’s unique business model, it was able to avoid big losses during the 2008-2009 financial crisis.

Even though rising interest rates and inflation could slow consumer spending, we feel Visa has many more years of growth ahead. The COVID-19 pandemic accelerated the shift to online shopping, while the easing of restrictions will spur the use of credit and debit cards to pay for airline tickets and hotel rooms.

Visa is also making shrewd acquisitions that enhance its expertise in new areas, such as buy-now-pay-later payment plans. These moves will let it stay ahead of smaller firms with potentially disruptive fintech (the combination of financial services and technology services).

The company also continues to reward investors. In the first half of fiscal 2022, it spent $7.05 billion on share buybacks. It still has $9.8 billion remaining under its current authorization.

Visa has also increased its dividend each year since the 2008 IPO.

Visa is a buy for long-term gains.

Spotting good companies for long-term investments lets you profit from long-term growth in the economy

For decades — as long as I’ve been involved with the stock market — some brokers have claimed that they favour the “buy and hold” investing strategy in principle, except when the market was so treacherous and unpredictable that their clients had to indulge in short-term trading, options or whatever to make any money. Continue Reading…

Imagine retiring, and then you have to head back to work, or you cancel your planned trips and greatly curtail your lifestyle. That’s what happened to too many who retired at or near the recesssions created by the dot com crash and the financial crisis. Risk in retirement is perhaps the flipside of risk in the accumulation stage. In the accumulation stage, lower stock prices can be very good. Lower prices in retirement can impair retirement. The equity risk in retirement is called sequence of returns risk. Poor stock market returns early in retirement can create a situation where the portfolio value has decreased, and selling more shares at lower prices might be hazardous to your retirement health. That’s why retirees own bonds, cash and GICs.

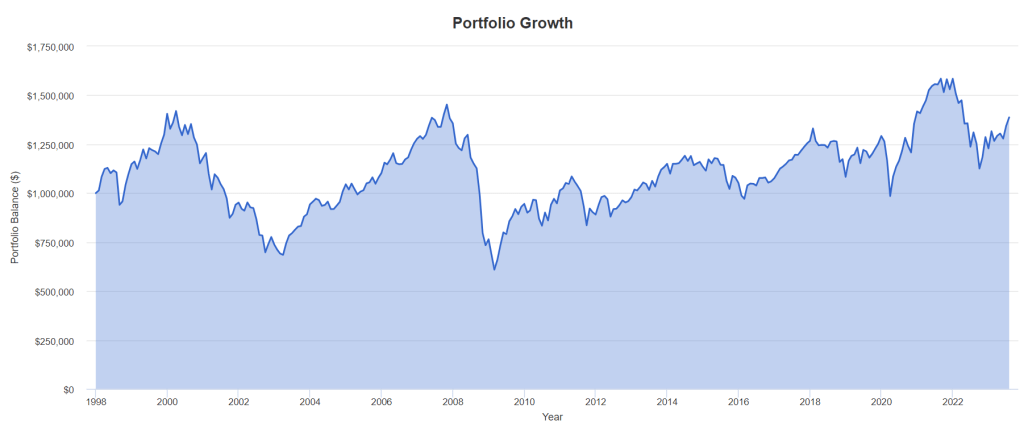

I will start off with a few charts that demonstrate the path of a retiree’s portfolio who retired at the start of the dot com crash (late 90s) and the financial crisis (2007-2009).

Here’s the drawdown history in recessions using the U.S. market as an example.

Yes, two of the most recent major corrections were epic and extraordinary. In the dot com crash and the financial crisis, stock markets were down 50%. In the early 2000s U.S. stock markets were down 3 years in a row.

The “average” decline in a recession is close to 25%. But as we know, average rarely happens when it comes to investing and stock markets.

The dot com crash retirement scenario

In the following scenario the retiree has a C$1,000,000 portfolio and spends 4.2% of the portfolio value in year one. The $1,000,000 creates $42,000 of income. The spending rate then increases, adjusted for inflation. If inflation is 3%, the retiree gets a 3% raise.

The portfolio is 50% U.S. stocks and 50% global.

Portfolio Visualizer

We can see that it was “over” quickly for the equity portfolio in this scenario. Even the strong market returns from 2003 to 2008 could not bring the portfolio back to health. In late 2007 the portfolio value was $870,000 but the spend rate would have been considerable. We have a portfolio value much lower than $1,000,000 and the amount taken out of the portfolio has increased at the rate of inflation. It is a dead portfolio walking, even in 2007. The financial crisis essentially finished it off, and was limping through the 2010s. 2024 would be its final year.

Unfortunate start date

The retiree was a victim of bad luck. They strolled into a very unfortunate start date – at the beginning of a recession and a severe stock market correction.

Let’s head back two years to see what happens to a retiree who retired in 1998.

What a difference two years makes. That said, I would suggest that the portfolio was impaired in 2003 and 2008. It was outrageous stock market gains that brought the portfolio back to the land of the living. There is no guarantee that after 40% and 50% portfolio declines that 30% and 20% annual stock market gains will ride to the rescue.

It’s also likely that a retiree who has watched 30% to 40% of their portfolio value disappear is not comfortable keeping up the spend rate. They have cancelled trips, dinners, gifting and more. They might have self-imposed retirement withdrawal.

Risk is different and feels different in retirement.

That self-imposed retirement withdrawal may have occurred during the financial crisis as well.

Who is going to keep the spend rate when the portfolio is down over 50%? I’d suggest no one. And I’d count that as a retirement failure, having to change your retirement plans.

Are you feeling lucky?

Now, let’s give the retiree a very fortunate start date. 1991.

The portfolio never sees new lows. And obvioulsy, the retiree could have treated themself to a much higher spend rate of 4.2% inflation-adjusted. That’s called a variable withdrawal strategy. You spend more when times are very good. And you spend less during recessions. More on that later. Continue Reading…

Phil Bliss (on left) interviewing Brad Krieger (right)

By Philip Bliss

Special to Financial Independence Hub

Starting a business can be both exhilarating and daunting. Aspiring entrepreneurs often find themselves navigating through a sea of uncertainties, seeking guidance on financing, funding, and launching their ventures successfully. In today’s digital age, podcasts have emerged as powerful platforms for disseminating invaluable insights and wisdom.

One such beacon of knowledge in the Canadian entrepreneurial landscape is the “#1 Podcast for Entrepreneurs in Canada” by canadaspodcast.com. In this blog post, we explore the profound importance of listening to entrepreneurs’ words of wisdom and advice, and how this podcast can become your go-to resource in your journey towards building a successful business in Canada.

Empowerment through Experience

The beauty of a podcast hosted by successful entrepreneurs is that it provides you with firsthand accounts of their experiences, challenges, and triumphs. These entrepreneurs have weathered the storm, overcome obstacles, and tasted success. By listening to their stories, you gain insight into the real-world dynamics of business, which textbooks and theories often fail to capture. Their experiences can empower you with the knowledge to avoid common pitfalls, make informed decisions, and stay motivated through tough times.

Insights into Financing and Funding

Financing and funding are critical components of starting and sustaining a business. Entrepreneurs featured on Canada’s #1 Podcast share their journeys of securing capital, whether it be through angel investors, family investment, venture capitalists, or traditional loans. Their advice can enlighten you on creating a compelling business plan, preparing a convincing pitch, and choosing the right financing options for your venture’s unique needs. Additionally, understanding the financial landscape in Canada and how to navigate it effectively can significantly improve your chances of success. Continue Reading…

Many people seek the life Findependence [aka Financial Independence] can bring. While there are many ways to achieve this status, one great way is to start a business.

Building a company can be daunting, but it’s vital to consider if it’s something you really want to do.

How does starting a Business help you reach Findependence?

Many business owners trying to obtain findependence implement an exit strategy. This is where the company still operates normally but doesn’t rely on the person who started it to do the work. In other words, the company is automated to function without intervention from the owner. Other people prefer to sell their organization and live on the profit they get from it.

Instead of selling the enterprise, another route is to invest the capital in different areas. Some entrepreneurs use the profit their business generates to create additional passive-income streams.

You can invest your money in many different areas to reach findependence. Here’s a summary of a few popular avenues:

● Roth IRA: This individual retirement account [in the U.S.; similar to Canada’s TFSA] offers the investor tax-free growth and withdrawals. To withdraw money from an IRA, the owner must own the account for at least five years and exceed the age of 59 and six months.

● Property: Many entrepreneurs decide to invest their capital into real estate to sell or rent it again. Buying property could be an excellent chance to obtain passive income, which can aid with the end goal of reaching findependence. However, real estate might have additional costs, such as hiring someone to manage the investment for you.

● The stock market: You can’t talk about investing and not mention stocks. Most people are already familiar with this option, where someone purchases a portion of a company and receives shared ownership. Stocks can also generate monthly passive income via dividends, but many consider them high-risk investments.

If investing company profits to reach financial goals is something you’re interested in, there are other opportunities to look out for. Consider researching bonds and index funds to determine if they’re something you want to invest in.

What kind of Business should you start?

The type of organization you should start comes down to personal preference. Consider looking at your interests and what excites you. Many entrepreneurs create a company around what they already know. For example, if they have coding experience, they could build a business offering customers web development services. Whichever idea you choose, ensure you conduct sufficient research to know what it will take to make it a success.