As Didi says in the novel (Findependence Day), “There’s no point climbing the Tower of Wealth when you’re still mired in the basement of debt.” If you owe credit-card debt still charging an usurous 20% per annum, forget about building wealth: focus on eliminating that debt. And once done, focus on paying off your mortgage. As Theo says in the novel, “The foundation of financial independence is a paid-for house.”

You’re a millennial. You’ve recently graduated from university and are beginning your career. You aren’t making quite as much as you’d hoped for, and as it turns out, rent is crushingly expensive.

Okay, you’ll just put off moving out for six months, save some money, live at home. Everyone’s doing it these days. You’re sure that before you know it you’ll be on track to success, living it up in homeowner-ville, sitting pretty. You’re not quite sure exactly how you’ll get to homeowner-ville, but it can’t be that hard, right?

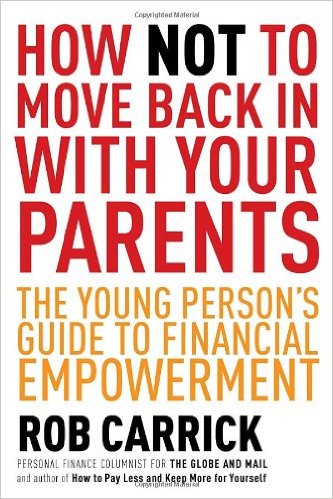

If any of this sounds plausible, I would seriously consider reading this wonderful book called How Not to Move Back in With Your Parents – The Young Person’s Guide to Financial Empowerment by Globe and Mail personal finance columnist Rob Carrick. I don’t want to be dramatic and say it will be your new finance bible, but it’s definitely a book you’re going to be referencing time and time again throughout those first few post-graduate years.

Something I really love about this book is that it’s broken down into great detail. Not only that, but it’s organized according to when in life you should be needing the advice.

In addition to running the Boomer & Echo website, Robb Engen is a fee-only financial planner. This article originally ran on his site on July 17th and is republished here with his permission.

We millennials are often told to visualize our future, then go out there and make it happen. But like so many things in life, this is more easily said than done.

Let me start with a disclaimer: Though finances are at the root of this week’s post, it’s mostly focused on spending our time and money on what we really want, as opposed to what society thinks we should want. ‘Should’ is a word I’ve come to decide to avoid at all costs.

As millennials, we get so focused on making sure we become good grownups that sometimes we forget just what we want it to mean. Do you want to become a good grownup by owning property, or is that just what everyone has told you makes a good grownup?

Could you be a good grownup by being completely financially self-sufficient while living the life you always wanted? Or do you think that being a good grownup means sometimes saying ‘no’ when you’d like to say ‘OMG YES PLEASE ALL OF THEM AND DO THEY COME IN RED?’

Clearly, being a ‘good grownup’ means different things to different people, which means it’s super important to define to yourself what you believe makes one. If you spend these valuable years working toward someone else’s dream, you could end up in a bad place.

Benefits of Imagination

A wonderful way to figure out what you want from life is to visualize or imagine it. Imagine yourself in your ideal place, doing the job you’d do even if they weren’t paying you. Daydreaming is a great way to escape the stresses of modern millennial life, Continue Reading…

We recently highlighted that now more than $10 trillion of government debt was trading at a negative yield. We mentioned it again in the Chalten Q2 Investment Review and have received a number of questions asking why anyone would ever hold a bond that would pay them back less than they invested. Why not just hold cash instead?

While it does seem bizarre at first there are both risk-related and practical reasons why investors might hold negative-yielding bonds instead of cash and some other reasons negative yielding bonds might still have value for investors.

Risk related / practical reasons for holding negative yielding bonds over cash

Just to get this one off the table right away, it is simply not practical or safe to hold cash physically, in a safe, under the mattress or buried in the back yard in mason jars!

Fortunately, the above options aren’t necessary as we have banks. However, there are definitely times where the safety and security of specific banks or the banking system in general is called into question. We can’t really relate here in Canada but living in Hong Kong in 1997/1998 and in the UK in 2008/2009, the topic came up quite regularly; by the end of the most recent financial crisis a lot of the UK banking system was effectively nationalized (nobody lost any deposits). For large depositors like institutional investors, keeping money in the form of bank deposits simply isn’t practical or prudent.

Certain institutions, such as insurance companies, are required to hold specific asset classes. So some may not have a choice but to hold certain government bonds with negative yields.

Other reasons why negative yielding bonds might still have value for investors

While certain governments’ bonds might currently be posting negative yields, an investor might still want bond exposure in that particular currency. For example, some global investors often think of the Swiss franc or Japanese yen as “safe haven” currencies. 10-year government bonds from those two countries currently have a negative yield. Perhaps the premium reflects current demand levels for safe haven currencies.

If an investor feels yields are going to fall even further, they might be expecting to receive further gains from bonds, even if current yields are negative.

In a deflationary environment, a bond with a negative nominal yield, could still give you a positive real (inflation adjusted) return. Ultimately investors care about real returns.

Perhaps most importantly, bonds are not just return generators – their principal role in an investor’s portfolio should be to act as an uncorrelated shock-absorber when stock returns turn negative. According to Vanguard, current correlations between stocks and bonds are at records lows (see: By this metric, bonds have never been more valuable).

I’m sure there are more reasons. Yes, it still seems strange; however, investors have gotten a little too used to thinking of bonds being return-generators or growth assets. Taken for what they really are, an investor’s safety net, bonds still hold a very valuable place in a diversified portfolio, even at negative yields. And of course there are still plenty of bonds, bond funds and ETFs offering yields well above those being offered for cash in the bank.

Graham Bodel is the founder and director of a new fee-only financial planning and portfolio management firm based in Vancouver, BC., Chalten Fee-Only Advisors Ltd. This blog is republished with permission: the original can be found on Bodel’s blog here.

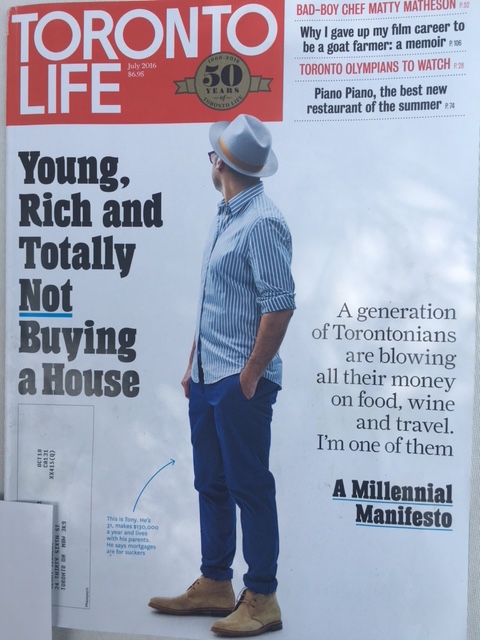

As a young, not-yet-rich millennial who has no immediate plans to get into the housing market, I was intrigued. The article is written by 31-year-old Tony; a pharmacist who lives with his parents and eschews the traditional rites of passage of his peers, like home ownership.

Before I actually read the article, I was sure I wouldn’t like Tony, wouldn’t relate to him. Growing up in Toronto I’ve seen his type countless times. Money is no object, and he’s not shy to show it. A common defence from this kind of person is that ‘normal’ or ‘rational’ people who are judging him are jealous or boring (or both).

What I found interesting about this piece is that Tony seems very self-aware about his spending and lifestyle choices. He’s accepting of his friends who do choose to be “shackled to a monstrous mortgage for the next 30 years,” and he understands that sometimes it just isn’t possible to have it all.

Though much of what Tony talks about in this article is out of reach for most normal millennials (last minute trips to Asia, $200 bottles of wine), I appreciate the sentiment. Continue Reading…

You’re a millennial. You’ve recently graduated from university and are beginning your career. You aren’t making quite as much as you’d hoped for, and as it turns out, rent is crushingly expensive.

You’re a millennial. You’ve recently graduated from university and are beginning your career. You aren’t making quite as much as you’d hoped for, and as it turns out, rent is crushingly expensive.