As Didi says in the novel (Findependence Day), “There’s no point climbing the Tower of Wealth when you’re still mired in the basement of debt.” If you owe credit-card debt still charging an usurous 20% per annum, forget about building wealth: focus on eliminating that debt. And once done, focus on paying off your mortgage. As Theo says in the novel, “The foundation of financial independence is a paid-for house.”

Here is a quote by Charlie Munger, vice chairman of Berkshire Hathaway, Warren Buffett’s business partner.

“The first $100,000 is a bitch, but you gotta do it. I don’t care what you have to do — if it means walking everywhere and not eating anything that wasn’t purchased with a coupon, find a way to get your hands on $100,000. After that, you can ease off the gas a little bit.”

Right now, my portfolio is over $500,000 but the first $100,000 were the most difficult to get because, of course, I started with $0, in a foreign country (Canada), with no family connections, no intergenerational wealth, no nothing.

Since I arrived in Canada, I have been a janitor, a busboy, a waiter, an Uber driver, a cleaner, a dance teacher, an insurance salesman, a photographer, and a website designer.

If you are a low earner, like me, you can only save $100,000 through a lot of discipline, sacrifices, perseverance, and the right mindset.

Most people, even those earning $100K per year, will never accumulate this amount of money. I feel extremely privileged to have arrived and surpassed this milestone.

I am the kind of person who believes that wealth is available to all of us and if we want it, all you have to do is to reach out and get it.

My biggest teacher in almost any entrepreneurial endeavour has been YouTube. My college education was not a complete waste, I get to go around and tell people that I have a college education, but for any practical purpose, it was useless.

You don’t need a fancy degree from any college to build wealth. Even now, I am teaching myself website design via YouTube.

Having the goal of saving $100K

Goals can also help to look toward the future and keep saving efforts in check. The more money you can save, either from reduced expenses or increased income, the faster you can move toward accumulating your first $100,000. And once you do that, the way to the next $100,000 becomes easier.

Having the right mindset

To save $100K you need to train your mind. Keeping your particular goal in mind can help, but you also need to understand how to achieve your goal with a plan.

As Canadians shop for last-minute gifts and search for deals, our Interac transaction data predicts that the busiest shopping day of the year will fall this year on December 22nd.

According to the transaction data, nearly 27.8 million purchase transactions are expected to take place next Friday (Dec. 22), representing roughly 2.7 million more transactions than the same date last year.

While Canadians are still planning to partake in gift giving, hosting, and more this holiday season, they’re feeling the constraints of today’s economic climate. Recent Interac survey* findings reveal that nearly four in ten Canadian shoppers (38 per cent) say they are feeling the pressure to spend during the holiday season even though their finances are tight.

Our survey revealed this phenomenon is felt as well among newcomers to Canada. Nearly seven in ten newcomers (69 per cent) say they feel more pressure to spend money around the holidays now that they live in Canada. What’s more, 71 per cent say their financial stress during the holidays has grown since moving to this country.

Amid rising prices, the holidays can be a stressful time of year. More than two thirds of Canadians (68 per cent) say they’re stressed about at least one aspect of spending during the holiday season and some sources of stress beat out others. Among those who are stressed, our survey shows us that buying gifts (77 per cent), spending money hosting and entertaining family and friends (41 per cent) and giving money to family members (34 per cent) are the top sources of stress.

For newcomers who are experiencing at least some holiday spending stress (82 per cent), spending money travelling to visit family and friends (48 per cent) is a prominent stressor.

As stressful as holiday spending can be, there are ways to make things a little easier:

Plan ahead

Try creating a gifting budget well in advance of any spending plans to help stay on track. Where possible, you can also look for a sale, consider a refurbished item or tap into purchases that make you and those around you feel good. You can also lean on Interac Debit to track your payments easily and take charge of your own money

Share the love, split the cost

When purchasing gifts for loved ones, organizing festive outings or hosting your family and friends, split the cost using Interac e-Transfer. Sharing the cost is one of the best ways to make sure you’re maximizing fun while staying in control of spending.

Embrace experiences

The holidays are a time to get together with friends and family and enjoy one another’s company. Consider sharing in an experience, rather than giving a physical gift. Interac research shows us that feel-good experiences are more likely to deliver happiness than material goods.

There seems to be some confusion around what to expect for monetary policy in 2024. There’s a strong consensus that cuts are coming, but what is far less certain is how many – and why they are implemented.

Let’s assume that all cuts are of the traditional 25 basis point variety. Since the bank rate is adjusted every six weeks, there will be eight or nine opportunities to adjust it in 2024 in both Canada and the United States.

There are as many as three narratives making the rounds about what might be in store. Each narrative has a combination of rate cuts for monetary policy and corresponding outcomes for the broader economy. I attended a luncheon last week hosted by Franklin Templeton, where senior representatives outlined three possible scenarios with three different narratives accompanying them. A similar perspective was offered earlier this week by the Vanguard Group.

The three narratives are as follows:

#1 We have a soft landing.

The soft landing involves the economy remaining relatively robust, employment remaining strong, delinquency is modest, and rates are normalizing at a level close to but somewhat lower than where they are right now. Most people would suggest that scenario involves no more than two cuts in 2024.

#2 We have a routine recession.

To be more precise, the second narrative involves a garden-variety recession that lasts perhaps a couple of quarters that involves only modest reductions in economic activity over that time frame. Nonetheless, this scenario includes five or six rate cuts to stimulate the economy to the point where things can become stable going forward.

#3 We have a severe recession.

The final narrative involves massive cuts that are made out of desperation to keep the economy from plunging into an abyss. This scenario is not only the most drastic, but also seems to be the least likely. Nonetheless, if things get really ugly, seven, eight or nine rate cuts might be needed to stanch the bleeding. One or more of those cuts might even be for 50 basis points or more.

While I accept the logic associated with all three scenarios, I cannot help but notice that much of the financial services industry is conflating those scenarios in a way that strikes me as being intellectually inconsistent. The financial services industry has long been overly optimistic in the way it portrays outlooks and forecasts. It routinely engages in something I call bullshift, which is the tendency to shift your attention to make you feel bullish about the future.

There can be little doubt that stimulative cuts are positive developments for capital markets. What the industry seems disinclined to acknowledge is that cuts are often made out of desperation. People need to look no further then what happened throughout the entire industrialized world in the first quarter of 2020. Central banks in all major economies cut rates to essentially zero by the end of March of 2020 in the aftermath of the COVID pandemic. At the time it was seen as being both necessary and reasonable, given the severity and breadth of the challenge.

Reining in Inflation

As we all know, inflation became the primary public policy challenge by the beginning of 2022. Central banks needed to take what looked like draconian measures to rein in inflation, which had risen to generational highs and needed to be brought under control lest a sustained period of inflation like what was experienced in the 1970s were to recur. By the end of 2023, inflation is still higher than the high end of the range that is deemed to be acceptable for most central banks.

There is still work to be done, yet many pundits seem eager to take a victory lap, as if a reduction in inflation is somehow akin to bringing inflation under control. Much has been done over the past 20 months, but more work is needed. The admonition that rates will have to stay higher for longer is a very real constraint on economic activity and long-term growth prospects. We head into the new year on the horns of a dilemma. Bond market watchers are now suggesting that rate cuts will come no later than Q2 2024, whereas central bankers are insisting that those cuts will be modest and will only begin in Q3 of 2024 at any rate. They cannot both be right.

It gets worse. Most commentators have taken to suggesting that we will have both a soft landing and five or six rate cuts in the New Year. That strikes me as being fantastic – not to mention intellectually inconsistent. If we have a soft landing, it will likely entail the economy being remarkably resilient as it has been throughout 2023. There is absolutely no reason to have a parade of rate cuts in such an environment.

Stated differently, the financial services industry needs to pick a lane. If it believes we will have a soft landing in 2024, it should also be anticipating a very small number of very modest cuts in the second half of the year. Conversely, if it believes a recession is on the horizon, it should be forecasting multiple cuts only after it is clear a recession is underway. These would likely be needed to stimulate the economy in an environment where inflation will likely be modest as a direct result of economic weakness.

To hear the industry tell it, the economy will remain strong, but we’ll get multiple rate cuts anyway. You can’t have it both ways. I call Bullshift.

John De Goey is a Portfolio Manager with Designed Securities Ltd. (DSL). DSL does not guarantee the accuracy or completeness of the information contained herein, nor does DSL assume any liability for any loss that may result from the reliance by any person upon any such information or opinions.

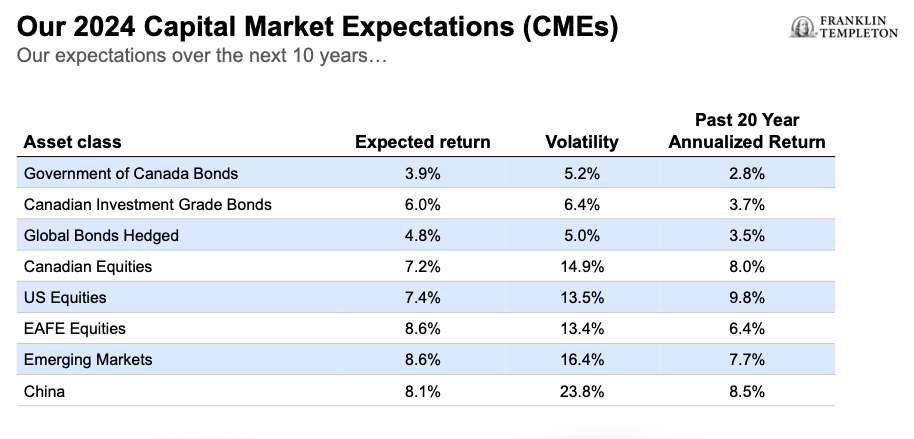

Investors can expect strong positive single-digit returns for the ten years between 2024 and 2034, portfolio managers for Franklin Templeton Investments told advisors on Thursday.

Ian Riach

Speaking at the 2024 Global Investment Outlook in Toronto, portfolio manager Ian Riach said Canadian equities will have expected returns in C$ of 7.2%, a tad below the 7.4% of U.S. equities and 8.6% for both EAFE and Emerging Markets and 8.1% for China. Riach is Senior Vice President and Portfolio Manager for Franklin Templeton Investment Solutions and CIO of Fiduciary Trust Canada.

Fixed-income returns are expected to be in the low single digits: 3.9% for Government of Canada bonds, 6% for investment-grade Canadian bonds and 4.8% for hedged global bonds, again all in C$. See above chart for the Volatility of each of these asset classes, as well as the past 20-year annualized returns for each. From my read of the chart, expected returns of North American equities the next decade are slightly below past 20-year annualized returns but EAFE and Emerging Markets expected returns are slightly higher, with the exception of China.

Fixed-income investors who were dismayed by bond returns in 2022 will no doubt be relieved to see expected future returns of Canadian bonds and global bonds are higher than in the past 20 years. “Expected returns for fixed income have become more attractive; recent volatility [is] expected to subside,” Riach said in the presentation provided to attendees.

Capital markets expectations (CME) are used to set Strategic Asset Allocation, which forms the basis of Franklin Templeton’s long-term strategic mix for portfolios and funds, the document explains: “Portfolio managers then tactically adjust.”

“This year CMEs are generally higher than last year. Primarily due to higher cash and bond yields as a starting point,” the document says.

Global equity returns are expected to revert to longer- term averages and outperform bonds, EAFE equities “look attractive,” and Emerging market equities are expected to outperform developed market equities, albeit with more volatility.

Central banks may have to tolerate higher inflation, but are determined to at least get it closer to target in the short-run. The Bank of Canada does have some room to tolerate a higher rate as its target is more flexible at 1%-3%. This compares to the Fed’s hard-wired 2%. Thus, rates in the US may stay higher for longer to bring inflation down to target

Risks of Recession

Riach described three major broad portfolio themes. The first is that Recession risks are moderating but “reasons for caution remain.” The second is that on interest rates, central banks have reached “Peak policy, but expect higher rates for longer.” The third is that “Among the risks, opportunities exist.” Addressing the narrow market of the top ten stocks in the S&P500 (the Magnificent 7 Big Tech stocks plus United Health, Berkshire Hathaway and ExxonMobi), market breadth should broaden to the rest of the market.

For portfolio positioning, Riach suggested selectively adding to Equities, overweighting U.S. and Emerging markets equities, underweighting Canada and Europe equities, and for Fixed Income,”trimming duration and prefer higher quality corporates.” In short, “a diversified and dynamic approach [is] the most likely path to stable returns.”

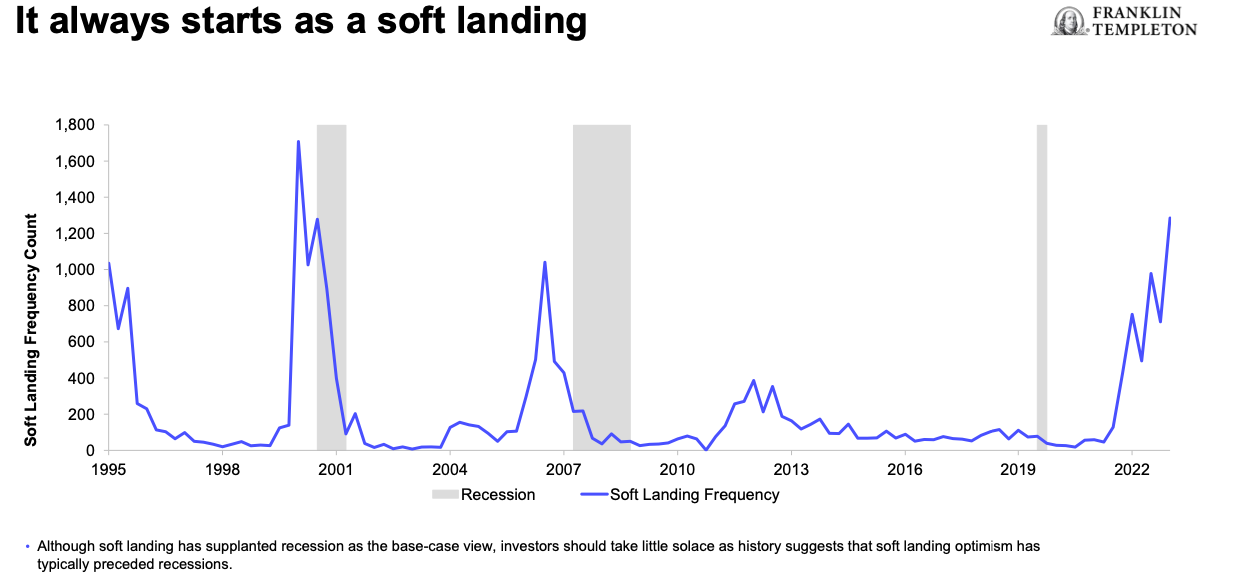

Jeff Schulze, Head of Economic and Market Strategy, ClearBridge Investments (part of Franklin Templeton) gave a presentation titled “Anatomy of a Recession.” A recession always starts as a “soft landing,” as the slide below illustrates. “We’re not out of danger. Leading indicators point to Recession,” he said, “The base case is Recession.” While the S&P500 consensus is for earnings growth, the U.S. GDP is expected to worsen.

He described himself not as a permabear but a permabull, at least until a year ago. If as he expects there’s a “soft landing” with stocks possibly correcting by 15 to 20% in 2024 Schulze would view that as an opportunity to add to U.S. equities in preparation for the next secular bull market.

One of the catalysts will be A.I., not just for the Magnificent 7 but also for the S&P500 laggards. As the chart below illustrates, economic growth often holds up well leading into a recession, with a rapid decline coming only just before the onset of a recession. Continue Reading…

By Alizay Fatema, Associate Portfolio Manager, BMO ETFs

(Sponsor Blog)

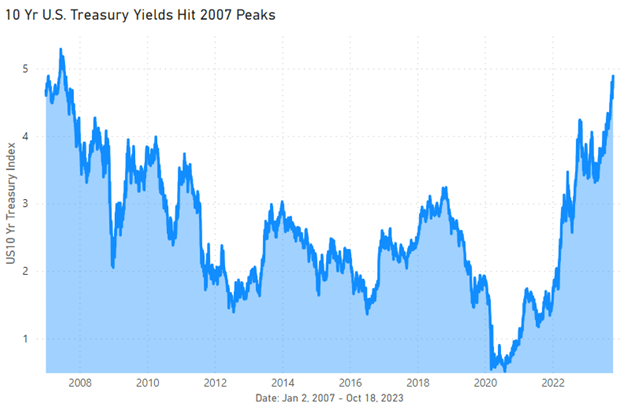

The latest economic data unveils a captivating narrative of a strong and resilient economy in both Canada and the U.S. The current inflation stickiness and robust job market numbers make a solid case for the central banks in both countries to keep interest rates higher for longer.

Towards the end of September 2023, markets basked in record-high yields. However, earlier this month, based on the current situation in the Middle East, bond yields fell owing to an increase in demand for safer assets and caused longer-term bond prices to surge. U.S. consumer prices remained elevated for the month of September and a pullback in demand for a treasury auction pushed longer-term yields higher again, resulting in 10-yr U.S Treasury yields touching their highest point since 2007. On the contrary, the recent CPI printed lower than expectations in Canada, yet the yields remain high as hot economic data continues to build pressure south of the border.

Source: Bloomberg

Given the current two-decade-high interest rates, yields on Aggregate Bond ETFs have surpassed 5%, making them an interesting avenue for fixed-income investors. Before we dive in further, let’s discuss some aggregate bond ETFs in detail along with their benefits.

Aggregate Bond ETFs as the Core of your Investment Strategy

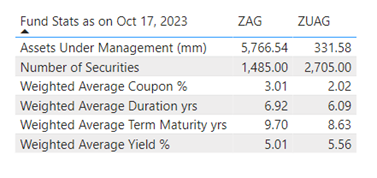

Aggregate bond ETFs are exchange traded funds that aim to track performance of a diversified portfolio of bonds. These ETFs are referred to as core because it reflects their status as a foundational building block of a well-rounded investment portfolio. These ETFs can help investors achieve diversification, steady income & stability within their investment portfolios. BMO currently offers two Aggregate Bond ETFs:

BMO Aggregate Bond Index ETF (ZAG) aims to replicate the performance of the FTSE Canada Universe Bond Index. This ETF primarily invests in a Canadian investment-grade fixed income securities consisting of Federal, Provincial and Corporate bonds, with a term to maturity greater than one year.

BMO US Aggregate Bond Index ETF (ZUAG) tracks the performance of the Bloomberg US Aggregate Bond Index. It invests in U.S. investment-grade bonds such as U.S. treasury bonds, government-related bonds, corporate bonds, mortgage-backed pass-through securities, and asset backed securities with a term to maturity greater than one year. ZUAG is also offered as hedged to CAD (ZUAG.F) and in USD (ZUAG.U).

Source: BMO Asset Management.

These aggregate bond ETFs have proven to be an extremely viable investment solution owing to their key features:

The Symphony of Diversification: Aggregate Bond ETFs provide exposure to a broad spectrum of bond market offering diversification across the curve, various sectors and segments, maturities, issuers, and credit qualities; making them resilient for any market environment.

For example, in the current high-interest rate environment, exposure to short duration bonds might provide some down-side protection. On the other hand, if central banks start cutting rates, then longer duration can provide some upside potential.

Aggregate Bond ETFs can also be considered an equity market hedge. Given the inverse correlation between equities and bonds, they can provide a cushion against market turbulence and can potentially outperform stocks during selloffs.

Harnessing Cost Efficiency through Lower Fees: These ETFs are passively managed with the aim to track performance of the aforesaid indices. Their expense ratios are lower as compared to some actively managed funds, thereby reducing overall investment costs and improving net returns for investors. BMO is currently charging a Management Expense Ratio of 0.09% for both ZAG & ZUAG.

Liquidity & Ease of Trading: Like all other ETFs, ZAG & ZUAG are traded on stock exchanges, enabling investors to easily buy and sell shares throughout the trading day, allowing them to see real-time prices. The bid-ask spreads on these products are lower in contrast with the underlying bonds which enhances their liquidity compared to traditional bonds, making them a cost-effective way to attain the exposure to the aggregate bond market.

Navigating Risk Management through High Credit Quality: Aggregate Bond ETFs are perceived as a stable and safer investment option as they provide exposure to investment-grade bonds, which are considered to have lower risk as opposed to high-yield or junk bonds. In the current rising interest rate environment, the credit quality & relative stability of the investment grade bonds make them an appealing choice for investors seeking to minimize risk & preserve capital.

Combined with the key features mentioned above, these Aggregate Bond ETFs provide investors with a low-cost core in any investment portfolio. They distribute monthly interest payments, providing a steady stream of income. These ETFs emphasize on preservation of capital and provide transparency and visibility into the funds’ composition and their underlying assets. Continue Reading…

By Alain Guillot

By Alain Guillot