By Mark Venning, ChangeRangers.com

By Mark Venning, ChangeRangers.com

Special to Financial Independence Hub

Following Canada’s National Institute on Ageing (NIA) since their beginning in 2016, it’s been a year since I last commented on the value of the NIA as a knowledge resource for Canadians on topics related to ageing and longevity.

And I would say, their regular reports, generated often in collaboration with other groups, are also a resource for anyone engaged in comparative research outside this country.

Now here’s today’s feature on one report from the NIA files from 2023 so far

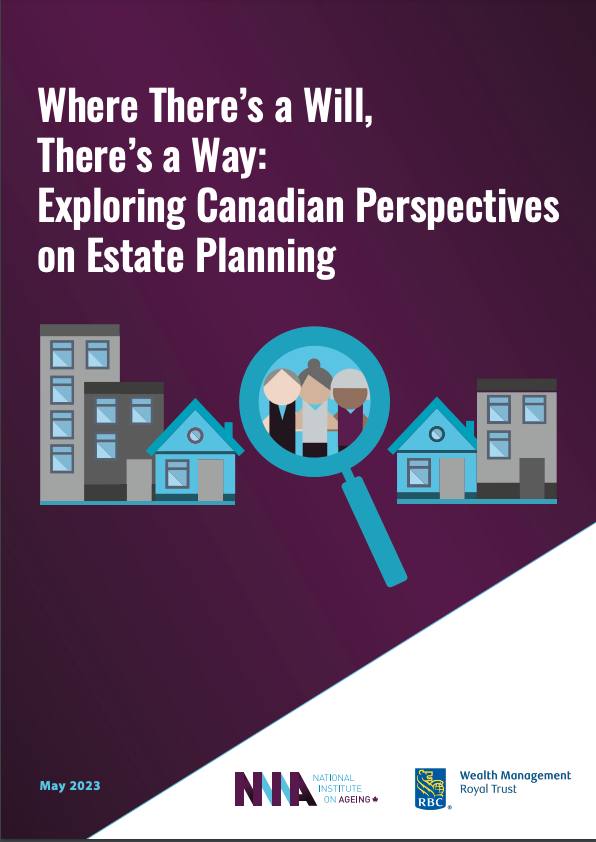

Where There’s a Will, There’s a Way: Exploring Canadian Perspectives on Estate Planning.

When I first received my NIA email notification of this report on May 17th, I was not surprised in the least by the lead headline: “Less than Half of Canadians Have a Will – and Many Don’t Even Know Where To Start.” For over twenty plus years, back when I was working in partnership with financial planners to deliver seminars on later life transitions, this was always a commonly known fact, and most people who didn’t have a Will knew that they should have had one.

The April 2022 Ipsos survey for this NIA report was conducted in collaboration with RBC Royal Trust. As the report details, it all starts with overall Estate Planning, and this includes setting up a Will, Powers of Attorney (POA) for care and property and, what was less discussed twenty years ago, Advanced Care Planning. As it happens my Will and POAs are ready for some small updating, but this time advanced care will also be on the agenda.

So if, as the report suggests, people know the value of planning and the subsequent sad consequences from not doing so – what’s the reason for inaction? I recall facilitating group conversations where literally some have said things like “if I do a Will, I know fate will bring me an early death” or, “I don’t have enough of an estate to worry about.” Of course the other concern I heard was about the perceived high cost of legal fees which halted the move to getting to the matter.

How fortunate for me, straightforward household budgeting and for that matter, estate planning Wills and POAs were things I learned early on at home from my parents, not from the education system. Today, learning from professionals in these topic areas should not be that intimidating or made difficult to access. Regardless of your age, picking up this report would be a great start. Continue Reading…