A growing number of Investors like buying Stocks without a Broker because they’re able to avoid possible Conflicts of Interest and Save on Broker Fees. However, it’s especially important to know what to Buy if you’re not using a Broker

Many investors assume their broker is honest and has their best interests at heart; if this proves to be untrue, they will shop for better stock trading advice from a new broker. Of course, many investors decide on buying stocks without a broker. That can be a successful strategy if you choose the best options for your investment temperament—using our Successful Investor approach.

Buying stocks without a broker: Why it might be a smart move for some investors

As any good stock broker or experienced investor can tell you, bad brokers are all too common. By “bad brokers,” we mean those who put their own interests above that of their clients. Keep in mind, however, that most bad brokers do this in a perfectly legal fashion, by catering to their clients’ whims and weaknesses.

Here are three main practices that bad stock brokers often practice:

Aiming for stability rather than growth

Double dipping

Stressing low-risk, low-return, high-fee structured products in client accounts

Additionally, you may have noticed that your broker sometimes uses unfamiliar words and phrases to describe investment concepts. Some of this stock broker jargon is simply shorthand that brokers use among themselves, to refer to familiar situations without having to go into any detail on the underlying concept. However, the concepts that these “broker-ese” words and phrases represent also serve to further the goals of the brokerage business.

If you find yourself thinking in broker-ese, you’ll naturally make assumptions that are in tune with the goals of your broker. They may be out of tune with yours.

Here’s one example: from time to time, your broker may advise you to sell a particular stock you own because it represents “dead money.” This doesn’t mean there’s anything wrong with the stock, or the company. Instead, your broker simply thinks the stock may only go sideways for a period of months or longer, producing no capital gains for you. So they naturally feel you should sell it and buy something with better short-term capital-gains potential. Continue Reading…

Many of us are familiar with the benefits of investing. Whether you’re looking to save for retirement, earn money in the stock market, or achieve some other financial goal, investing — when done well — can help you build your financial future. But if you’re not professionally trained in the stock market, starting out can be daunting.

Whatever the reason someone has for dipping their toes in the investing waters, starting out can be daunting. There’s a lot of math involved, tricky rules, and an entire lexicon of investing terms to remember. Those who are not scared away may be wondering where to start.

Despite these fears and uncertainties, though, leaping off the investing cliff can help build a foundation toward financial freedom. Here are five tips for new investors looking to get started in the stock market.

1. Set an Investment Budget

It can help to make investment contributions part of a normal household budget. By setting aside a predetermined amount of funds to funnel into investment accounts each month or pay period, one can rest assured that their accounts are being regularly funded, even as the market rises and falls. A good investment goal is typically between 10% to 15% of your income. If one is enrolled in an employer sponsored retirement plan, their match counts towards that percentage goal.

2. Start Investing as Early as Possible

Finances can be tight when someone is just beginning to invest, even with a job that pays their bills. However, once you’re able to allocate a portion of your monthly income to investing in the stock market, it’s beneficial to start investing as soon as possible.

The earlier one begins to invest, the longer they can allow compound interest to accumulate. Compound interest is how your investments grow. For example, if you have an account that pays 1% interest per year and you deposit $1,000 into that account, you would earn $10 on that money in one year. Average rates of return can fluctuate year by year, so make sure that you check out the rate of return on any stock or money market account you may be interested in.

3. Learn Basic Investing Terminology

While those just beginning to invest don’t need to know everything off the bat, there are a few terms they will need to familiarize themselves with to help them make smart investment decisions. For example, what is a money market account, anyway? How about an IRA? Continue Reading…

Canadians face a lot of headwinds in this volatile investing year, including high inflation, rising interest rates, slower economic activity and geopolitical shocks. In this turbulent environment, an actively managed income strategy can help steer the way through uncertainty. Volatile markets call for a strategy that can adjust client portfolios in a timely, tactical way as market conditions shift.

Active investment management can play a key role in offering a compelling risk-reward option for investors who are looking for income, growth and overall portfolio diversification. The strategy that underlies the Franklin U.S. Monthly Income Fund is an example of an approach to seeks to give investors stability amid volatility.

“The fund has a portfolio that can make adjustments in a timely manner on your behalf,” said Rob Rocoff, Vice President, Regional Sales with Franklin Templeton Canada in Toronto. “It’s a fund that uses a flexible, balanced strategy that is capital structure agnostic and has a track record in the U.S. of over 70 years of being able to tactically adjust to volatile market conditions.”

The Franklin U.S. Monthly Income strategy aims to generate income by investing in stocks, bonds and hybrid securities, such as equity-linked notes (hybrid securities have characteristics of both stocks and bonds). The strategy’s flexible asset allocation allows it to adjust across different market cycles, including moments of high pressure, to find the most attractive investment opportunities.

The Franklin U.S. Monthly Income strategy looks throughout the capital structure for securities that offer attractive income and long-term growth potential. Top-down insights inform the investment team’s view on asset allocation, while the security selection process is driven by rigorous bottom-up fundamental research. The team focuses on investment opportunities where their fundamental views may differ from the market consensus, especially with investments in large companies.

Seeking Yield from multiple sources

As a result, the fund’s portfolio includes equities (common or preferred stocks), fixed income assets (e.g., investment grade bonds, Treasuries) or hybrids (e.g., equity-linked notes and convertibles). This mix seeks yield from multiple sources and allows for dynamic asset allocation, depending on market conditions. Continue Reading…

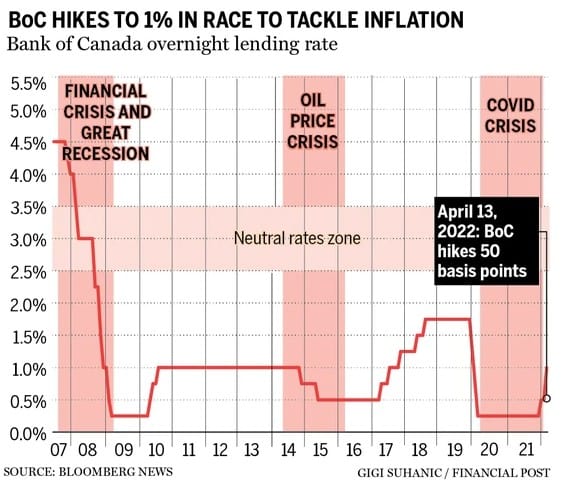

Lately, the talk of the town seems to be rising interest rates. In April, the Bank of Canada raised the benchmark interest rate by a whopping 0.5% to 1%, making it the biggest rate hike since 2000. Given the high inflation rate, it is almost a given that these rate hikes will continue throughout 2022 and beyond. [On July 13, 2022, the BOC hiked a further 1%: editor.]

But before you freak out, let’s step back and look at the big picture. At 1%, the benchmark interest rate is still relatively low compared to the past interest rates.

I still remember years ago before the financial crisis, being able to get GIC rates at around 5%. And some people may remember +10% interest rates in the 80s or early 90s. Back then, interest rates were much much higher than measly below 1% rates we’ve been seeing the last decade.

Historical BoC overnight rates

What’s going to happen to the stock market? Well the general rule is that when Bank of Canada or the Federal Reserve cuts interest rates, the stock market goes up. When Bank of Canada or the Federal Reserve raises interest rates, the stock market goes down.

It’s been awhile since I reviewed any political books here on the Hub. The last time was this time a year ago when I surveyed what were then the latest books on the Trump presidency (at one point in 2021, 3 of the top 6 New York Times bestselling books were on Trump: see here).

I occasionally wade in on this topic on the grounds that investors need to be on top of this seemingly unique political situation. That’s despite the fact that when Trump first won his shock victory in 2016, markets briefly cratered, only to quickly recover.

The particular pair of mini-reviews below has no real financial angle but you can see I explicitly covered that a few years ago in a MoneySense column that evaluated the implications of the Trump presidency for the Boomers’ collective retirements: see here.

Over the long weekend, I finished reading two recently published books that some may find of interest, whose covers are illustrated on this blog. One is Thank You for Your Servitude, Mark Leibovich’s entertaining summary of all the Republican enablers who made the Trump presidency possible in the first place, and may yet facilitate a dreaded second term. The other is This Will Not Pass [Simon & Schuster) by Jonathan Martin and Alexander Burns, subtitled Trump, Biden, and the Battle for America’s Future. The co-authors are both New York Times writers and CNN political analysts, neither known as MAGA-friendly outlets.

Save your money and borrow these from the library

I might add that, despite being an author myself, I generally refuse to buy any of these US political books: I either read ebooks from the Toronto Library’s excellent Libby app, or download ebooks or audio books from the paid SCRIBD service. Libby often involves waiting a few weeks or months for popular bestsellers; however, if you can read quickly, you may be able to luck into the occasional Skip the Line service, which lasts only a single week. SCRIBD sometimes has books not yet on Libby, often in audio format, and unlike the library, you can keep them beyond the normal three-week limit.

There’s been a fair bit of press and YouTube clips on both these books. Formerly with the New York Times, Leibovich is perhaps best known for his bestselling This Town, about 21st century Washington. Thank You for Your Servitude [Penguin Press, New York, 2022] is subtitled Donald Trump’s Washington and the Price of Submission. While the author admits that many of the anecdotes will be all too familiar to anyone following the daily press, he manages to provide a fresh perspective on them while simultaneously apologizing for making readers relive the worst of these moments. Many of them center around Trump’s Washington-based Trump Hotel, which is where the book begins and ends. There you meet such familiar characters as Rudy Giuliani, Reince Priebus, Kevin McCarthy, Mitch O’Connell, William Barr, Jeff Sessions, Lindsay Graham, Marjorie Taylor Greene, Kellyanne Conway and the whole sordid collection of Trump toadies and sycophants, or the so-called MAGAts.

One early chapter is entitled “The Joke,” which apparently is how even how Trump’s closest enablers seem to view his rise to the top of the political pyramid:

It would be risky, obviously, for a Republican member of Congress to declare, explicitly, that “Donald Trump is a complete ignoramus,” even though that’s what they really believed. But none of this had to be spoken because the truth of this scam, or “joke,” was fully evident inside the club …. Everyone … got the joke.

Covers Ukraine invasion but not January 6th hearings

The book is recent enough that it includes an epilogue about the Russian invasion of Ukraine in February. The book ends on a despairing note of pessimism about the prospects of anyone stopping Trump in 2024. Of course, it was published months before this summer’s high-profile January 6th hearings, nor does he spend much time addressing any of the other multiple investigations into Trump’s businesses and political shenanigans.

The following telling snippet is one of many that may not be widely known. I was struck by the revelation in the epilogue that within a day of Trump’s “Be there, will be wild” tweet promoting the January 6 rally, the cheapest room in the Trump Hotel immediately jumped from US$476 to US$1,999.

Donald Trump didn’t just inspire the Jan. 6 riot … He seems to have made money off it.

That pretty much says it all. Leibovich ends with an ominous foreshadowing of Trump’s possible triumphant return in 2024. His final sentence is “And who’s going to stop him?” A few sentences earlier, he quotes a former Republican congressman who confessed that the party’s only real plan for dealing with Trump in 2024 involved a darkly divine intervention: “We’re just waiting for him to die .. That was it, that was the plan. He was 100 percent serious.”

Can Joe Biden extract the US from its “political emergency?”

Simon & Schuster

Those who are thoroughly sick of Trump — as I am — may find This Will Not Pass more to their liking, as roughly half the content is devoted to Trump’s successor, Joe Biden. The focus is what it describes as the “political emergency in the United States: the story of how the country reached and survived a moment when carrying out the basic process of certifying an election became a mortally dangerous task.”

It recounts how the country “sort of” survived but like Leibovich, leaves readers pretty nervous about what may yet occur in the 2022 mid terms this fall and ultimately in 2024. As Martin and Burns remind us (as if we needed it!):

Donald Trump has not been banished from national life, but instead remains the dominant force in his party and is bent on purging those few Republicans who won’t bow to him … The former president’s delusions about a stolen election … have lingered with corrosive force, warping his own party and catalyzing a wave of red-state voting restrictions aimed at cracking down on election fraud that did not happen. The fantasies of a Trump restoration have only deepened since his departure from the White House.

The book is arranged in three parts: the year before the 2020 election and Trump’s mismanagement of Covid; the tumultuous months between the contested 2020 election and Inauguration Day, and everything that has transpired since:

… As President Biden attempted an acrobatic feat of leadership: pushing a liberal policy agenda of titanic ambition with the thinnest of majorities … Far from quickly erasing the Trump era, leaders in both parties have found the shadow of the last presidency has been longer and darker than they anticipated, colouring every major political decision and legislative negotiation of the Biden administration and shaping even the perceptions of American democracy overseas.

Ambitious, yes: One chapter nicely summarizes the dominant question before Biden as “How Big Can We Go?”

Unlike Servitude, This Will Not Pass was published too soon to cover much of the events of 2022. Oddly, for an American book, it closes with an observation by a Canadian, Bob Rae (at one point Canada’s ambassador to the United Nations.) He calls Trump an “authoritarian … I don’t believe the Republican Party believes in democracy.” And he warned that the threat to American democracy was far from defeated: “America,” he said, “is a very important battleground.”

They Want to Kill Americans

(Added subsequently). There’s a third and even scarier book that I only began to read the day this blog initially was published. They Want to Kill Americans by Malcolm Nance, describes Trump’s brownshirts and the ongoing assault on American democracies by Americans. Here’s a link to Goodreads’ entry on it. And here’s a Kirkus review.

Jonathan Chevreau is Chief Financial Officer of the Financial Independence Hub, author of the financial novel, Findependence Day, co-author of the non-fiction Victory Lap Retirement, and columnist and Investing Editor at Large for MoneySense.ca.

A growing number of Investors like buying Stocks without a Broker because they’re able to avoid possible Conflicts of Interest and Save on Broker Fees. However, it’s especially important to know what to Buy if you’re not using a Broker

A growing number of Investors like buying Stocks without a Broker because they’re able to avoid possible Conflicts of Interest and Save on Broker Fees. However, it’s especially important to know what to Buy if you’re not using a Broker