By Paul MacDonald, CIO, Harvest ETFs

(Sponsor Content)

As the MRNA winners of the COVID-19 vaccine race turn their sights to illnesses like shingles and the flu, investors and analysts are renewing their focus on innovation in the healthcare sector. If a technology like MRNA can conquer endemic illness and even go on to combat cancer, what other lifechanging innovations could the healthcare sector provide us with? What opportunities could those innovations open for investors?

The healthcare innovation story is wider, deeper, and richer than MRNA to me. The healthcare sector has been innovating since human beings first started to treat illness. It is a sector built on the use of the scientific method to develop novel solutions to new and ancient problems of human health. Healthcare companies, by nature, push the limits of human knowledge to heal people. That means innovation in the space is a near-constant.

In the healthcare sector large-cap companies play an outsized role. These firms have the scale to innovate a wide range of products and services on their own and are well positioned to capture value from innovations initiated by smaller-scale companies. Our view that these large-caps serve as the fulcrum of healthcare innovation underpins the Harvest Healthcare Leaders Income ETF (HHL).

When we think about large-cap healthcare, we have to see these companies as innovators. They are always innovating on their own, but they’re also the companies that have the ability to extract value from innovation by smaller-cap firms in the sector.

Within HHL we own the dominant companies in the sector, companies with tremendous R&D platforms across subsectors.

How one ETF captures a universe of healthcare innovation

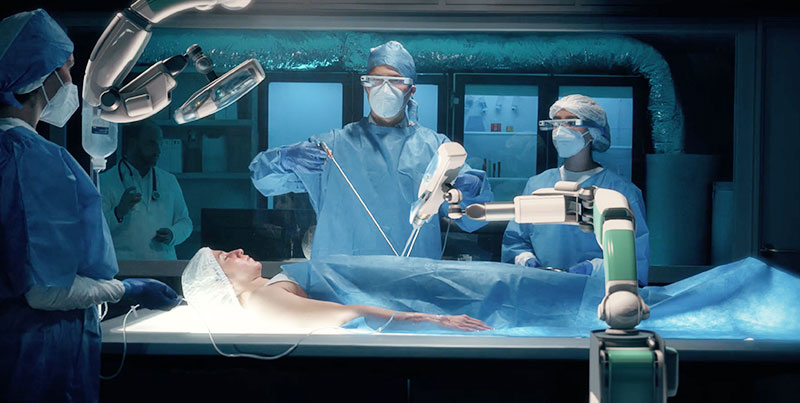

Those subsectors include pharmaceutical companies finding new avenues for MRNA, but they also include the biotech companies like Abbot Labs using phones to better monitor diabetes patients and the med-tech companies like Stryker developing robotic surgery assistants to power less-invasive operations with better outcomes. They even include healthcare providers like United Health, using and developing new technologies to provide better and more efficient patient care. HHL is set up, through a basket of 20 of the best large-cap healthcare companies, to capture healthcare innovation in almost all its forms.

That diversity of innovation is why a large-cap ETF like HHL is so well positioned in the space. We should emphasize that healthcare innovation will generally follow one of two paths. The first is that headline-grabbing, game-changing, blockbuster innovation. That would happen when one company is able to completely change the outcomes for an illness or condition that hasn’t seen much significant improvement. A major leap in Alzheimer’s treatment would be one such blockbuster. Continue Reading…