The Canadian Financial Summit is back once again this fall with a terrific line-up of 35+ personal finance experts, including yours truly, to tackle the burning financial questions facing us today.

You’ll hear from PWL Capital’s Ben Felix, Millionaire Teacher Andrew Hallam, The Globe and Mail’s Rob Carrick, consumer advocate Ellen Roseman, along with long-time personal finance bloggers Barry Choi, Tom Drake, Mark Seed, Bob Lai, , Stephen Weyman and Jonathan Chevreau.

How to take a tax holiday by working outside of Canada

Want an Unlimited TFSA? Try moving to these countries with territorial taxation

Are dividend stocks in a bubble?

The risks of investing in cryptocurrency

Should I have Bitcoin in my Portfolio?

Maximize the New Aeroplan and Post-Covid travel plans

Don’t let FOMO ruin your investment returns

Maximize Work From Home tax tips in a Post-Covid World

Will the Canadian Housing bubble finally pop?

How to setup a corporation, invest within it, and then pay yourself

The BEST ETFs in Canada

Why self-made dividends are better than ordinary dividends in every way!

I was happy to chat with co-host Kyle Prevost earlier this summer when we filmed our session about how not to let FOMO (fear of missing out) ruin your investment returns. It’s a topic at the forefront over the past 18 months as cryptocurrencies and meme stocks soared by triple and quadruple digits. Continue Reading…

Vanguard Investments Canada Inc. has announced the launch of two new globally diversified and actively managed mutual funds it describes as being “low cost”: Vanguard Global Credit Bond Fund [VIC500] and Vanguard Global Equity Fund [VIC600.] complement the firm’s current line-up of 37 ETFs and four mutual funds.

Management fees will be 0.40 and 0.55% respectively. Asked whether this means payment of trailer commissions to financial advisors, Vanguard Canada spokesperson Matthew Gierasimczuk told the Hub: “No. Vanguard doesn’t pay trailing commissions in any of our markets since we have a longstanding belief it leads to a conflict of interest for investors.” The funds are available through most wealth advisors and also on Questrade and Qtrade, he added.

In a news release issued on Sept. 13, Vanguard Investments Canada Inc. Managing Director and Head Kathy Bock said:

“Within an uncertain investing climate, Canadian investors and their advisors are looking for quality, long-term and high-performing investment products, at a low-cost … These mutual funds provide that and reflect our deep 45-year history in active management with proven portfolio manager expertise that can help investors achieve success.”

Globally, The Vanguard Group, Inc. manages over USD $8.1 trillion in assets and is one of the world’s largest active managers with USD $1.7 trillion in global actively managed assets under management.

“Since introducing our mutual funds three years ago, Canadians have embraced our differentiated approach to active management, providing investors with access to skilled global investment managers with a long-term view,” said Tim Huver, Head of Intermediary Sales, Vanguard Investments Canada Inc. “These two global funds can act as a core holiding or complement to an investor’s equity or fixed income portfolios.”

Vanguard Global Credit Bond Fund seeks to provide a moderate and sustainable level of current income by investing primarily in non-government fixed income securities of issuers located anywhere in the world. The fund will have a management fee of 0.40%. The fund will be sub-advised by The Vanguard’ Group Inc.’s Fixed Income Group, a global team of more than 185 tenured and dedicated professionals overseeing USD $2.1 trillion in total assets. For 40 years, Vanguard Fixed Income Group has been distinguished in the industry by its deep investment capabilities, disciplined security selection process, rigorous risk management techniques and strong long-term performance.

Vanguard Global Equity Fund seeks to provide long-term capital appreciation by investing primarily in equity securities of companies located anywhere around the world. The fund will be sub-advised by Baillie Gifford Overseas Limited and Marathon Asset Management Limited. These sub-advisors have worked with Vanguard for decades and collectively manage over USD $500 billion in assets under management. The maximum management fee for the fund will be 0.55%.

One thing that many economic historians often overlook is that one’s worldview is shaped by life experiences. That includes matters like love, marriage and divorce, money and savings and attitudes toward political risk – to name a few. If our values, likes and dislikes are shaped by our experiences, it stands to reason that our perceptions of what the future might hold could be largely informed by what we have already experienced. That’s especially true of the things we experience in our formative years.

In the summer of 2021, for the first time in over a generation, there’s been some talk of inflation being a going concern. Inflation was wrestled to the ground in the 1980s and hasn’t been heard from since – until now. As the debate rages about the degree to which we should be concerned (if at all) about inflation coming back in a meaningful way, it is noteworthy that while there are credible economists on both sides of the debate, virtually everyone in the “inflation will be a problem” camp is at least 70 years old. Stated differently, those people who experienced inflation in their adult lives are concerned and those who did not are not.

Transitory inflation?

For about 30 years now, the goal of central banks in the west has been one of price stability, which they define as inflation at 2%, give or take 1%. Basically, anything between 1% and 3% is okay. Now, we’ve experienced inflation above 3% for a couple of quarters and people naturally wonder what that might mean. Central Bankers have been assuring us that the uptick is “transitory,” that it is just a situation where awful data from the early days of the COVID crisis is working its way through the system. Nothing to see here. Move along.

Although I am technically old enough to remember inflation, I never had to deal with it personally or directly. I was a teenager when my parents built the family home on their property in 1979. I heard about their astronomical, double-digit mortgage rates, but never had to experience anything of the sort as the payor. My sense is that young people – especially millennials – cannot relate to anything close to what I’m about to say: the inflation rates, and therefore the mortgage rates and interest rates you have experienced throughout your entire lives, may not be around for much longer. Furthermore, if that is true, the consequences could be enormous.

5% constitutes “Real inflation”

As mentioned, there are competing views on inflation. I have not come down on either side, but I enjoy the exchange of ideas. If the doves are right and the inflation we’re seeing now is little more than a passing phase, there’s not much to say because little will change. If, however, real inflation is coming sooner than later and for longer than just a phase, we need to prepare. What constitutes ‘real inflation’, you may ask. My guess is something like 5%. At that level, no one can pretend that the inflation rate is not a concern and does not need to be dealt with. For this discussion to be meaningful, inflation needs to be at least 2% above the high end of the traditional range and to stay there for at least a year. At that point, both the logic behind it being transitory and the facile dismissal of it being above the target by an inconsequential amount disappear. At that level, something needs to give. Continue Reading…

By Steve Lipper, Senior Investment Strategist, Managing Director, Royce Investment Partners

(Sponsor Content)

Companies with small market capitalization make up one of the more overlooked parts of the global equity markets. This could be attributed to a lack of coverage of their stocks by analysts, but whatever the reasoning, being overlooked creates opportunities for those investors who know where to look among small-cap equities.

Royce Investment Partners has more than 45 years of experience in the small-cap space. Such longevity brings with it a high level of expertise, allowing the firm to build assets under management (AUM) of US$17.6 billion.1

This has been achieved through a combination of specialization in small-cap investments and a commitment to ownership among the firm’s portfolio managers. With an average tenure of 22 years, Royce’s seasoned group of PMs have substantial ownership in the strategies they manage; in fact, 89% of the firm’s assets are in funds where the portfolio manager has invested at least US$1 million themselves.2 In this respect, Royce stands apart from its competitors: 37 asset managers in the U.S. have more than US$5 billion in small-cap assets, but only Royce has more than 95% of its total AUM invested in the space.3

While developing expertise in small-cap investing is complex, the reasoning for specializing in this area is quite simple: quality small-cap companies have been proven to deliver for investors.

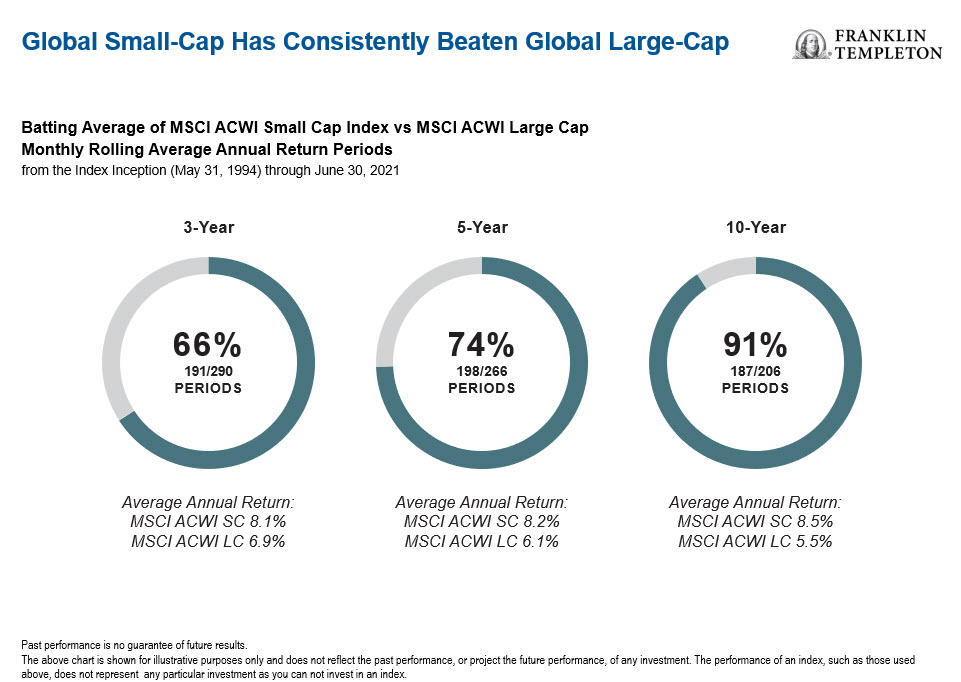

In fact, small-cap stocks have consistently provided meaningful outperformance compared to their large-cap counterparts over the long term. Using the MSCI ACWI Small Cap and MSCI ACWI Large Cap indices as proxies, it shows that small caps have delivered higher annual returns over most multi-year time periods (see chart below). In addition, small caps not only provide a much larger set of companies to invest in (approximately four times the amount in large caps), but with valuations that often understate their true worth. This is an important point to consider, especially given some of the pretty elevated valuations in equity markets right now.

As this link published at MoneySense.ca on Sept 3rd indicates, I will be giving a half-hour virtual presentation on September 21st on how the annual MoneySense ETF All-stars package can help retirees and near-retirees build their nest eggs and then draw income from them. (i.e. Accumulation and Decumulation).

The World of ETF Investing Canada Virtual Expo talk is on Sept. 21. Registration is free.

Here’s how MoneySense describes it:

Jonathan Chevreau, a longtime personal finance journalist, former Editor-in-Chief of MoneySense and the creator of our perennially popular Best ETFs in Canada package has said there’s only one free lunch for investors—and that’s the kind of broad diversification you can get from a low-cost, broadly diversified portfolio “core” based on exchange-traded funds (ETFs).

ETFs have become so popular that there are now roughly 1,000 listed on Canadian exchanges alone, with thousands more on US and international stock exchanges. Now in its 9th annual edition, I write up the feature each spring after conferring with an all-star panel of eight investing professionals and specialists. Together, we narrow the field to the very best options across five categories: Canadian, U.S., International, fixed-income and all-in-one asset-allocation funds.

In addition individual panelists provides their unique “Desert-Island Picks” that they are particularly passionate about and that may merit consideration, but don’t achieve the full-consensus vote otherwise required to make the cut. Continue Reading…

The Canadian Financial Summit is back once again this fall with a terrific line-up of 35+ personal finance experts, including yours truly, to tackle the burning financial questions facing us today.

The Canadian Financial Summit is back once again this fall with a terrific line-up of 35+ personal finance experts, including yours truly, to tackle the burning financial questions facing us today.