Pleased to meet you

Hope you guess my name

But what’s puzzlin’ you

Is the nature of my game

- Sympathy for the Devil, by The Rolling Stones

By Noah Solomon

Special to Financial Independence Hub

Historically, bonds have offered investors two main benefits. Firstly, their yields provided a reasonable, if unspectacular return. Secondly, they offered diversification value, muting overall portfolio losses during bear markets.

In my view, it is the second attribute that is the most important. In relative terms, bonds are not particularly useful for providing investors with strong long-term returns (that’s equities’ job!). So, by process of elimination it follows that the primary function of bonds is their diversification value.

When comparing equity strategies, one should compare their relative returns, volatilities, Sharpe ratios, drawdown characteristics, etc. However, given bonds’ primary purpose of providing diversification, an extra layer of diligence is required when evaluating bond strategies. Specifically, you should analyze their differing correlations to equities, and by extension their varying abilities to offset stock price declines during challenging environments.

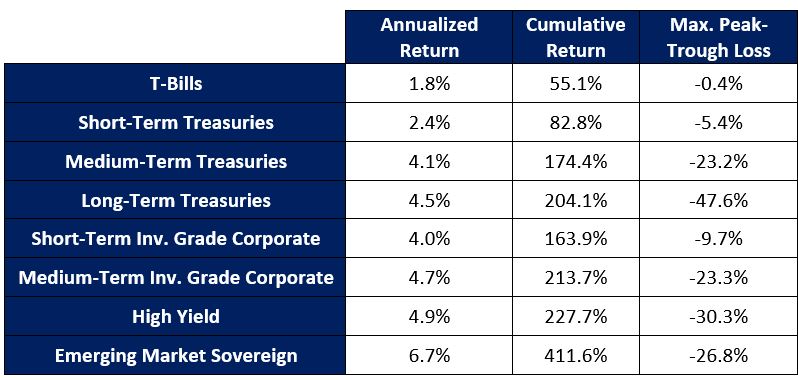

There is no Free Lunch Part I

Economist and Nobel Prize recipient Milton Friedman famously stated, “There is no such thing as a free lunch,” which means that every choice has a cost, even if it’s not immediately obvious.

Traditional bond mandates each have their individual advantages and pitfalls with respect to returns, risks, and diversification properties. In terms of the tradeoff between risk and return, history strongly suggests that there is no clear free lunch to be had.

Risk vs. Return by Bond Type: 2000 – 2024

As the above table illustrates, there is a clear relationship between the returns of the various segments of the bond market and the maximum losses that they have sustained over the past 25 years. If you want extra return, you can reasonably expect to suffer larger losses in bad times. That being said, large losses in bond holdings are generally not what investors want or expect.

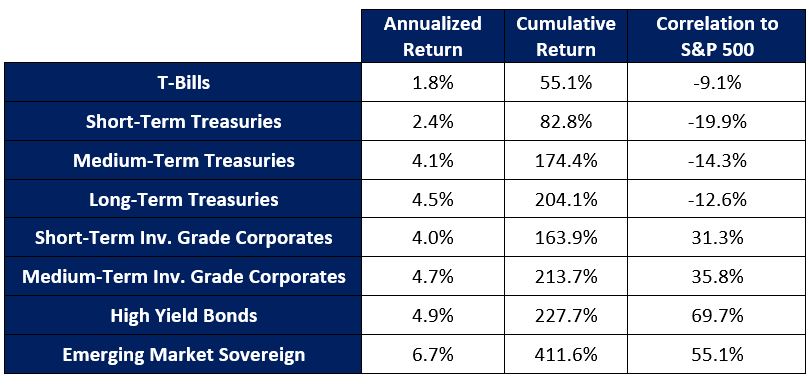

There is no Free Lunch Part II

Not only is there no free lunch with respect to the tradeoff between risk and return, but there is also none when it comes to diversification value. Higher returns are not only associated with larger losses but are also associated with higher correlations to equities.

Return vs. Correlation to Stocks by Bond Type: 2000 – 2024

Bonds that offer higher returns have a greater tendency to move in tandem with stocks, thereby providing less ability to mitigate stock losses during bear markets. In contrast, lower-return bonds possess greater diversification properties and thus are better equipped to offset stock-price declines during times of equity market turmoil.

None of the above: Sometimes there’s Nowhere to Hide

Notwithstanding the fact that higher-return bonds have on average suffered more severe losses and offered less diversification value than their lower return counterparts, these relationships have exhibited significant variations across different bear markets. Continue Reading…