By Dale Roberts, CutTheCrap Investing, Retirement Club

Special to Financial Independence Hub

Schwab’s SCHD is a popular U.S. dividend ETF that has been disappointing investors for a long time. Does that disappointment mean that the fund is going to shine when (if) the AI bubble bursts? And speaking of shining, we’ll take a look at gold. Can it go even higher? Plus, Canada’s most defensive sector ETF has a surprising history of outperformance.

What to expect from the U.S. stock market over the next 10 years? Not much.

Once again, having lived through it, and invested through it I remember:

He pointed to a JPMorgan chart from late last year that looked at what an investor’s annual return on average over the next 10 years would be if they had bought S&P 500 at a given price/earnings ratio. The P/E was 23 at the time, meaning that average return would be 2% to minus 2%, he said.

Of course there are other lost decades, such as the Depression era and the stagflation era of the late 60s into the early 8’s. But don’t worry: it was all ‘easily handled by a balanced portfolio with some inflation protection. We call that an all-weather portfolio of course.

Even a 5% allocation to gold during the stagflation era would have allowed you to breeze through the period. Add in oil and gas stocks and yer laughing.

That portfolio idea (not advice) uses defensive sectors in concert with dedicated inflation fighters.

Is SCHD well-positioned for a dot.com-like correction?

I’ve penned extensively on the concept that retirees might pay attention to valuation issues and hedge that risk with a U.S. value-oriented holding. We’d continue to hold some U.S. market or U.S. growth, but layer in a value holding. The Schwab Dividend ETF SCHD is a popular choice. What’s up with SCHD? Or what’s down might be the appropriate question.

I created a meaningful position in iShares Quality Dividend ETF XDU-T (Canadian Dollars) as a valuation slant. It outperformed SCHD in 2024 and that continues in 2025. In price terms SCHD was down 1.7% in 2025 while XDU-T was up 4.4% (at time of writing late in October 2025). We might attribute about 2% of that gain to the Canadian currency weakness vs the U.S. Dollar.

The S&P 500 was up 13.66% in 2025. The Nasdaq 100, QQQ was up 18.36%. Money continues to flow to growth-oriented stocks in the U.S.

This article on Seeking Alpha (sign up or sub required) suggests that SCHD might be well-positioned if we do get a major correction and rotation to value and quality.

The top 3 sectors for SCHD were leading sectors when the dot com bubble burst …

That chart tracks Energy, Consumer Staples and Healthcare vs Tech.

Who knows, but SCHD’s stubborn decline might be creating even greater value. Here’s an interesting table on sectors and valuation.

worldperatio.com

In the search for value you might also consider small cap, or mid cap or a classic value index ETF such as iShares VLUE. As I wrote for Findependence Hub, these might be challenging times for recent retirees who do not pay attention to valuation. You’ll find more bubble-bursting ideas in that post 😉

Accumulators with decades to go might ignore the valuation “issue.”

I’m happy with XDU and some of my other U.S. value-oriented stocks. In my U.S. RRSP account, my individual U.S. stock portfolio was up 20.7% in 2025 (again, as of time of writing). The core stocks are still driving the bus.

Second Quarter 2026 BMO Macro Regime Model – Strategy Report

By Bipan Rai, BMO ETF & Structured Solutions

(Sponsor Blog)

Upon reflecting on the current state of markets, we’re reminded of the lessons from Barbara Tuchman’s The Guns of August, which illustrates how hubris and rigid systems can override rational decision-making.

While we are not drawing direct parallels to the current situation in the Middle East, the book offers important lessons for investors as they navigate portfolio construction in the months ahead.

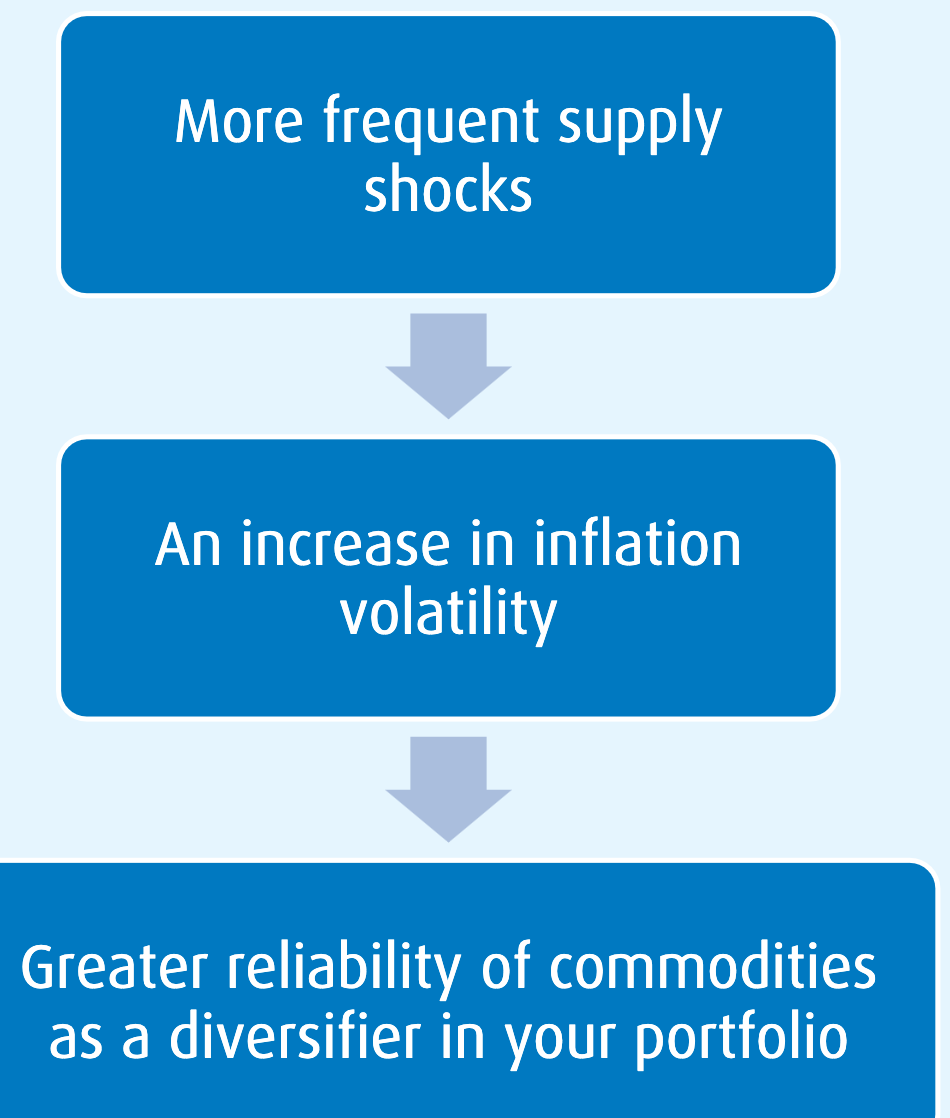

As an example, periods of higher inflation generally increase the co-movement between U.S. stocks and interest rates, requiring a more pragmatic approach to diversification. This often leads to greater interest in real assets like gold, as we’ve seen in recent years.

But what happens when even gold fails to provide adequate diversification during a geopolitical shock? Tuchman’s work reminds us of the importance of stress-testing assumptions before a crisis unfolds. When correlation structures break down and traditional hedges falter, investors who have considered tail risks in advance are better positioned.

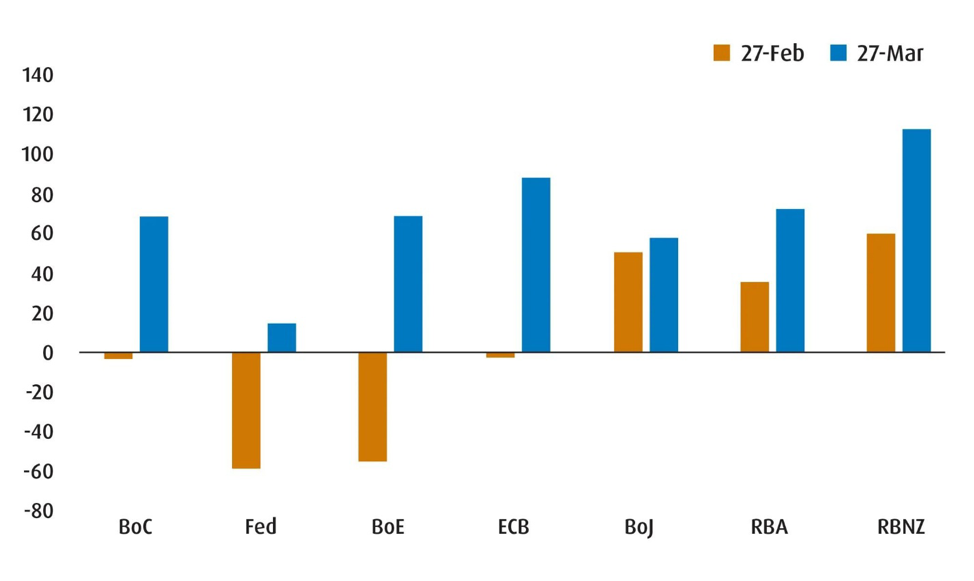

With that in mind, let’s consider the present environment. Even if the Middle East conflict is resolved quickly, the economic and market consequences will likely persist. Inflation risks are no longer symmetrically distributed, and price pressures appear likely to rise. Damage to energy-related infrastructure points to a prolonged period of crude oil and LNG supply disruption, pushing prices higher for longer. This affects refined products (such as gasoline, jet fuel, and kerosene), fertilizer production, and the supply of helium: complicating central bank messaging. Markets have responded by pricing out expected Federal Reserve rate cuts and pricing in aggressive hikes for other developed-market central banks (Chart 1).

Chart 1 – Markets Have Priced in Tighter Central Bank Policy by End-2026

Source: BMO Global Asset Management, as of March 27, 2026.

At the same time, growth risks are shifting in the opposite direction. Higher input costs act as a tax on consumers and weigh on corporate margins. The speed at which rising energy prices feed into slower growth depends largely on a country’s economic slack, which explains why some central banks have recently acknowledged growth risks more explicitly than they did in early 2022.

Indeed, our own proprietary macro regime model is signaling that we are transitioning from a ‘reflation’ backdrop to a more stagflation-like regime (Chart 2).1 This emerging stagflation regime need not mirror the 1970s, but we are still positioning our portfolios to be more robust and resilient. We’re broadening our commodity exposure to provide a more direct hedge against supply shocks. In an environment where inflation surprises are more likely to be positive, this type of convexity is valuable.2

We are also allocating to front-end TIPS (Treasury Inflation-Protected Securities) as a hedge against inflation pressures. While breakevens3 have moderated with recent disinflation progress, they do not fully reflect a sustained energy shock. TIPS offer a cleaner way to express inflation risk without requiring a strong view on nominal growth.

Within equities, we are tilting toward quality and low volatility. If growth slows while cost pressures persist, companies with strong balance sheets, durable margins, and stable cash flows should outperform more cyclical or highly leveraged peers. Low-volatility exposures can also help reduce drawdowns during headline-driven market swings.

History teaches us that conflict does not guarantee crisis. But periods of stress often reveal underlying fragilities. Our role as stewards of capital is not to forecast every geopolitical development, but to recognize that the distribution of macro outcomes is tilting toward a stagflation-like environment: and to position portfolios accordingly.

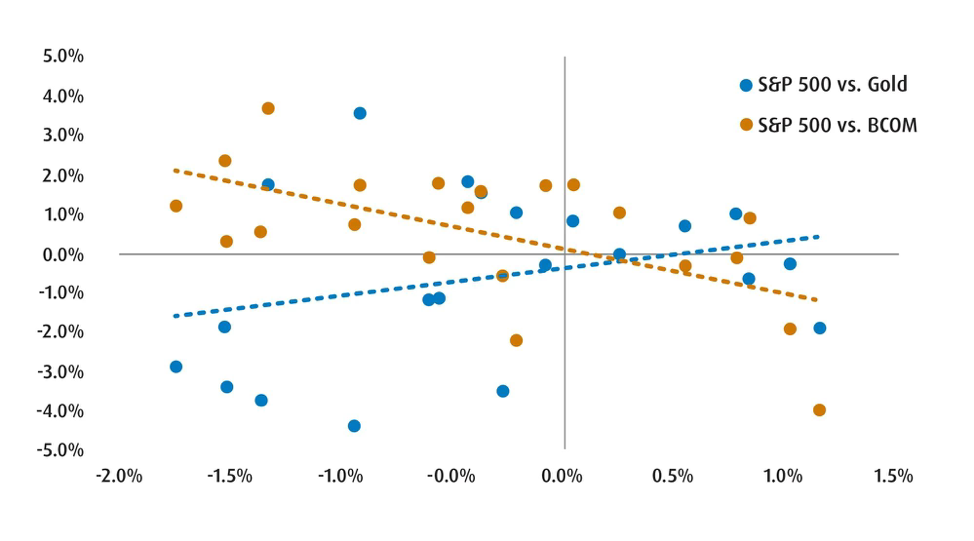

Chart 2 – Broad Commodity Exposure is Now a Better Diversification Strategy than Just Relying on Metals

Source: BMO Global Asset Management, Bloomberg. Daily returns from February 27 to March 27.

Asset Allocation

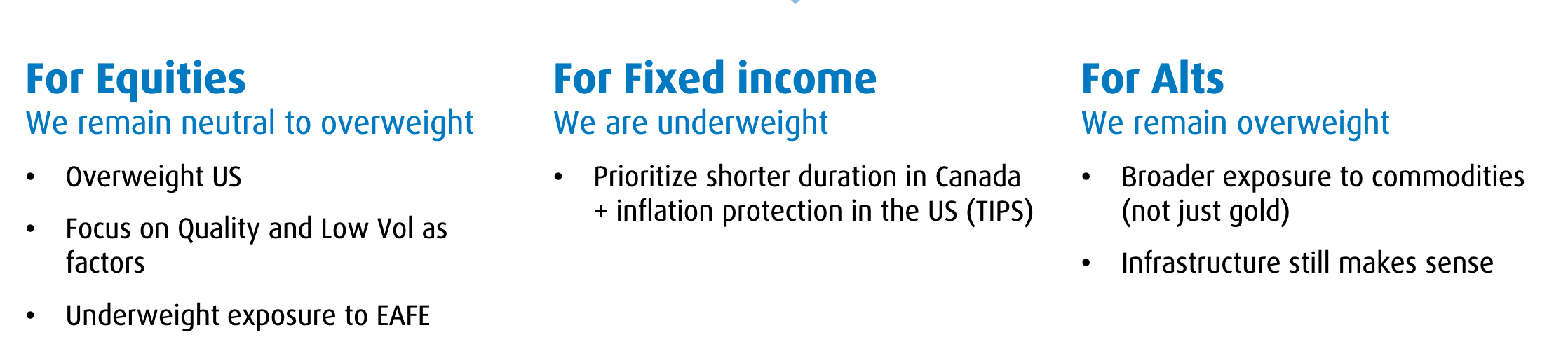

Relative to the Q1 edition, we’re making some modest changes to our asset allocation splits. The most notable shifts are that we are paring our positions in the equity and alternative sleeves and reallocating them towards fixed income. Of course, these aren’t big changes: as we still remain underweight fixed income and overweight both equities (slightly) and alts.

Our macro regime model suggests that we are in the midst of a transition from reflation to stagflation: characterized by low growth and high inflation. This is still consistent with the late cycle feel of the macroeconomic backdrop.

Despite the challenging backdrop, the underlying fundamentals remain sound enough to maintain a neutral/slightly overweight broad equity position for now. Ahead of the conflict, we did see earnings growth across several sectors in the U.S. and Canada. At the same time, the situation in the Middle East remains fluid, which requires us to be nimbler and more flexible.

In the fixed-income sleeve, the increase in weight reflects our view that the Canadian yield curve4 provides better value and that we feel U.S. TIPS should outperform in the months ahead. For the alts sleeve, the reduction in weight reflects our shift away from gold and towards a broader set of diversifiers in the commodity and infrastructure spaces.

Importantly, we are bullish on the U.S. dollar (USD) for the coming months. This means that our preference is to keep our U.S. exposure unhedged on a tactical basis. The main reasons for this view are the following:

We expect the CAD swaps market to price out rate hikes for the Bank of Canada in 2026.

We expect USD upside as net long positioning remains relatively light.

Equities

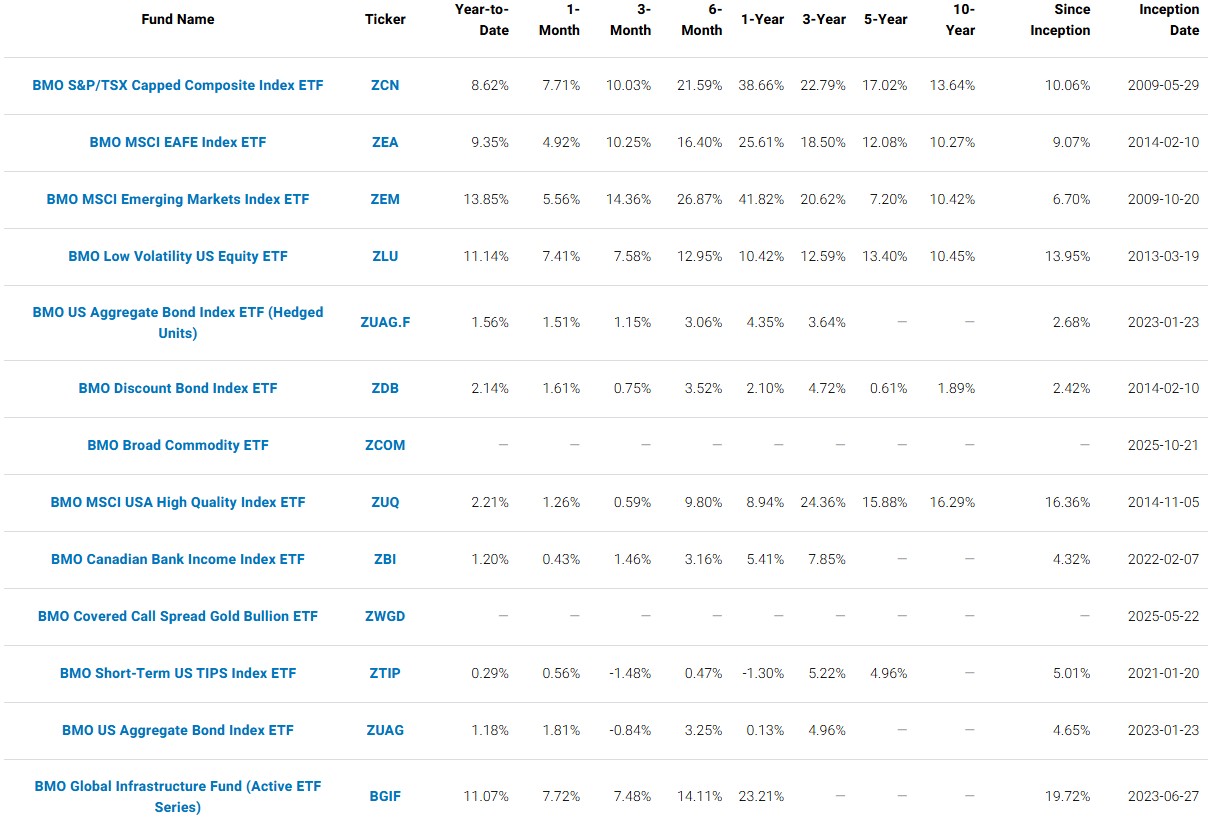

We are increasing our allocation to ZCN (BMO S&P/TSX Capped Composite Index ETF)as Canada remains well positioned as a commodity and energy producer. With energy prices supported by ongoing geopolitical uncertainty, the Canadian equity market should continue to benefit, though outcomes will remain sensitive to the duration of the conflict in the Middle East.

For our U.S. position, we are adding ZLU (BMO Low Volatility US Equity ETF)to complement our existing exposure through ZUQ (BMO MSCI USA High Quality Index ETF). This combination reflects a preference for defensive characteristics and earnings resilience during a period whereby investors remain selective on valuation and fundamentals.

We’ve also added ZTIP (BMO Short‑Term US TIPS Index ETF)as a tactical position as we expect inflation risks to stay firm given energy and broader commodity pressures.

Alts/Hybrids

The most notable change we’ve made in Alts/Hybrids is adding a tactical allocation to ZCOM (BMO Broad Commodity ETF)to broaden our inflation and geopolitical hedge. Energy has led performance on a year‑to‑date basis, but a persistent risk premium can support a wider set of commodities, which improves diversification if equity volatility picks up.

We’ve also upgraded the weight for BGIF (BMO Global Infrastructure Fund ETF)as we continue to constructive on infrastructure, including electric grids, and engineering/construction projects.

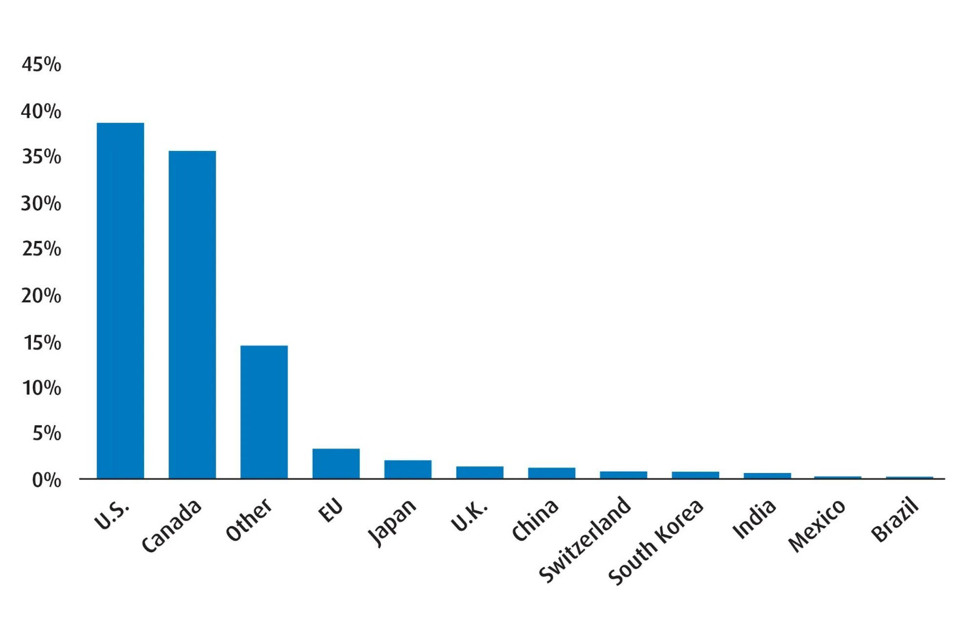

Chart 3 – Q2 2026 Regional Exposure

Source: BMO Global Asset Management, as of March 31, 2026.

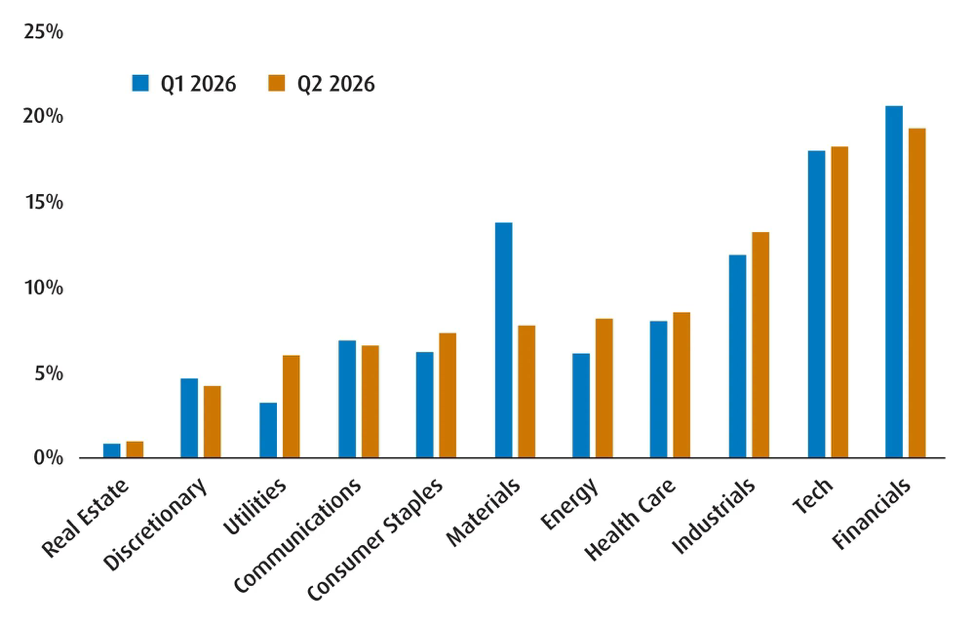

Chart 4 – Global Equity Sector Breakdown

Source: BMO Global Asset Management, as of March 31, 2026.

Building a nest egg is a respectable goal for financial enthusiasts at all levels, but many focus entirely on accumulating capital, losing sight of key structural considerations.

As fulfilling as it is to watch your balances grow through long-term discipline and determination, ensuring that Wealth is supported by sufficient pillars is imperative for success. When the entire fate of your security relies on a single stock or industry, it’s more of a gamble than a solid foundation.

What is a Financial Single Point of Failure?

In Engineering, a single point of failure is a component that brings down the entire system if it malfunctions. The world of Finance is no different. A financial single point of failure occurs when a specific asset or condition in your portfolio accounts for a disproportionate share of your net worth.

For many professionals, this often manifests as concentrated stocks. If your primary income or retirement savings are tied to the success of your employer, a scandal or industry downturn could wipe out both your career and savings at once.

Another common problem is not having an appropriate amount of liquid reserves. While having home equity is a key aspect of a wealth strategy, having little liquidity is a risk. A sudden shock like a medical emergency could force you into a high-interest loan or a badly-timed panic sell.

Core Strategies for Financial Protection

Effectively shielding your nest egg requires understanding and implementing a few fundamental concepts:

Diversify your Investments

Many financial enthusiasts believe that portfolio diversification simply entails owning multiple stocks. While this holds some truth, it’s a small part of the equation. Optimal diversification requires an understanding of correlation.

If you own 10 different companies, but they all belong to the software industry, it is still considered a single point of failure. A shift could cause all your assets to depreciate simultaneously. If your portfolio looks like this, consider branching out to other asset categories, such as bonds or real estate.

How you allocate assets should be determined by personal risk tolerance, financial targets and current situation. Many people prefer sticking with longer-established investments such as government bonds or Exchange-Traded Funds (ETFs.) Others lean toward newer and more “adventurous” investments such as cryptocurrency and blockchain technology, which have shown considerable innovation in recent years.

Protect your Major Assets

If you own a home, that is likely your largest asset. It can also be a significant liability if not managed with vigilance. Proper diligence involves paying for insurance and managing the risks associated with maintenance.

For example, it’s essential to ensure hired contractors carry adequate insurance to shield you from liability during renovations. Taking the time to verify coverage prevents sudden workplace accidents on your property from turning into expensive lawsuits that drain your investment accounts.

Build an Emergency Fund

A liquid emergency fund is the most effective insurance for your long-term investment strategy. Continue Reading…

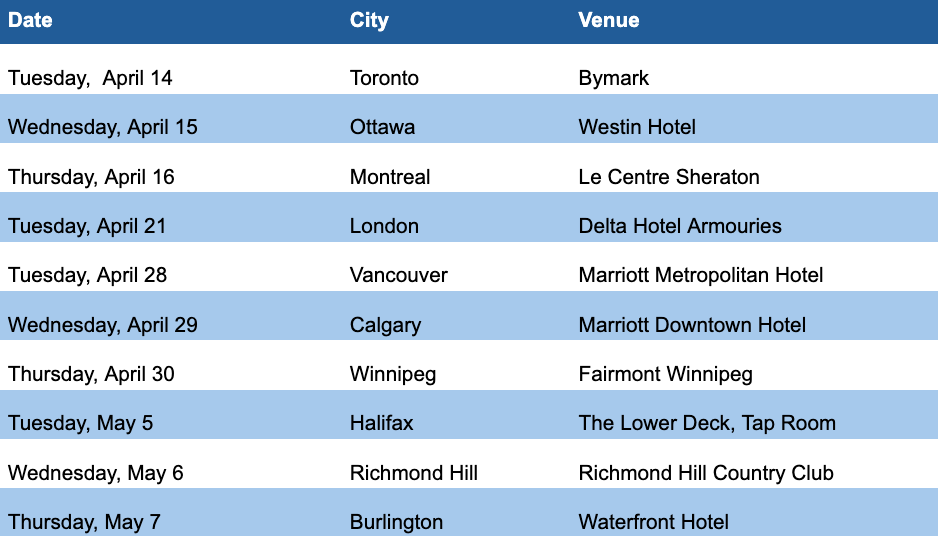

On Tuesday, I attended the Toronto instalment of BMO ETFs’ Spring Road Tour, the first of a 10-city Canadian tour that extends into early May.

The title is We’ve got you covered, which is a sly allusion to one of the main themes of the series: Covered Call ETFs.

Aimed primarily at financial advisors, the sessions are roughly an hour long, coinciding either with breakfast or lunch, depending on the city. There are three main segments:

Bipan Rai, Head of ETFs & Alternatives Strategy, provides insights into BMO’s current macroeconomic outlook, including positioning across asset classes and risk models

Jimmy Xu, Head, Liquid Alts and Non linear ETFs, manager of BMO’s flagship Covered Call ETFs, discusss these innovative solutions designed to help clients meet their cash flow needs while maximizing long term growth.

The road show ends with an introduction to BMO’s new Portfolio Consulting Services, designed to help advisors navigate an increasingly complex investment landscape. Senior Portfolio Consultant, Hilly Cutler shares how BMO supports advisors in optimizing their model portfolios—reducing costs, enhancing diversification, and managing risk as CRM3 approaches.

As the chart below summarizes, the road shows ends in Burlington on May 7th:

Except the Toronto event, which was a breakfast session, the other sessions all begin at either 12 pm or 1 pm. Below we reproduce some of the slides presented at the show.

Current Market outlook and Positioning by Bipan Rai

Bipan Rai, BMO ETFs

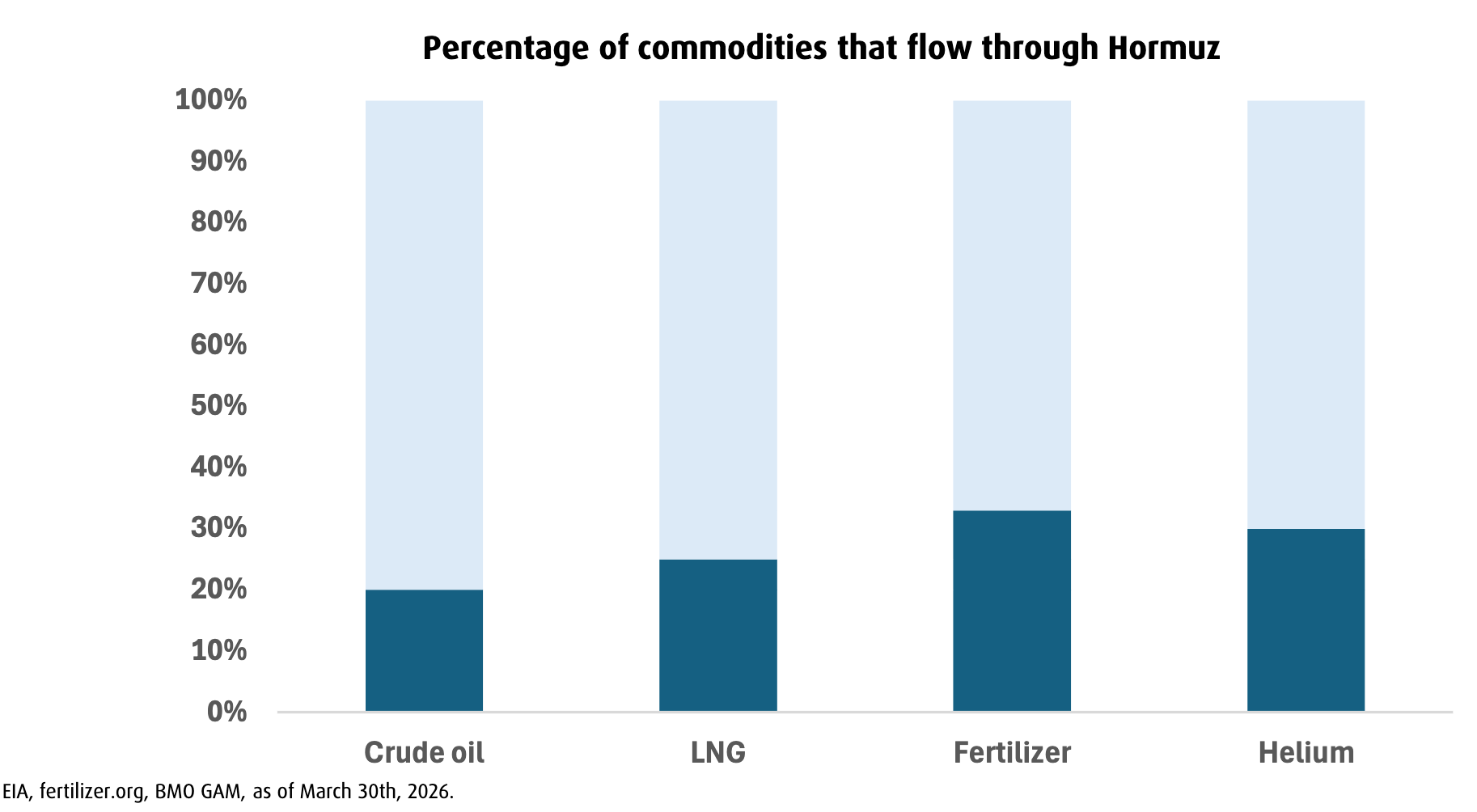

The sessions kick off with a current market outlook delivered by Bipan Rai, who focused on the impacts of the ongoing Iran war, which began at the end of February. He confessed to having a few sleepless nights about the closing of the Hormuz Strait. Not surprisingly most investors suffered negative returns in both stocks and bonds during March. Hormuz matters for the macroeconomic picture, not just because of oil, but also because of Liquid Natural Gas, fertilizers and Helium: the latter helps cool AI systems. (shown below).

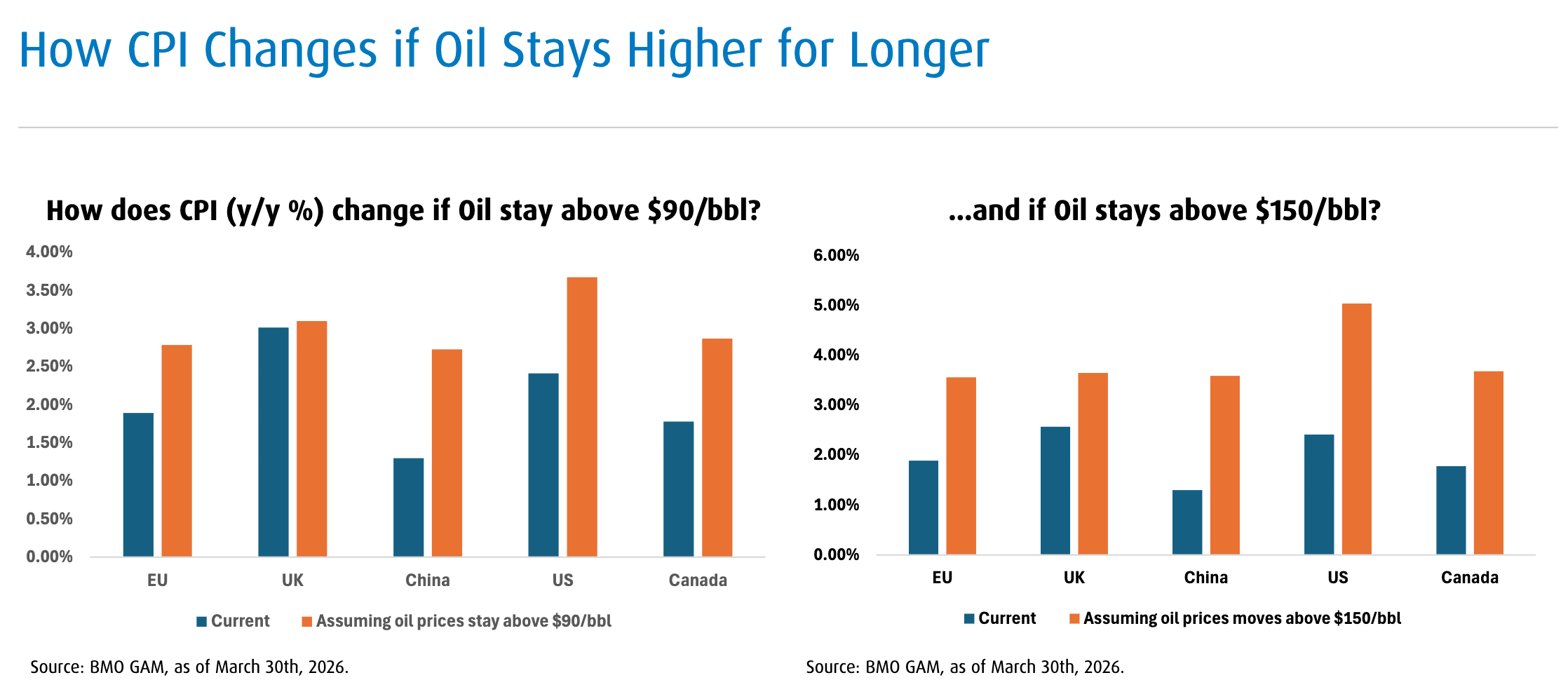

Rai also showed the following two charts, which illustrate how the Consumer Price Index changes the longer the price of oil stays higher. The longer the Strait is closed or traffic severely constrained, the more it will create inflation and create risks to economic growth.

If the price of Oil does stay higher for longer, Rai commented that investors may want to take a more defensive tilt to equities, emphasize quality and low volatility as factors, diversify with Treasury Inflation Protected Securities and embrace broad commodities. BMO has of course ETFs for all of these: such as ZTIP (BMO Short-term US TIPS Index ETF) or the new ZCOM for broad commodity exposure.

Rai’s “big takeaway” is that while Commodities are the “source of the shock,” they also “benefit from supply constraints, fiscal demand and de-globalization.”

Knowing that Inflation risks are “to the upside” and “growth risks are to the downside” Rai concludes that “We are most likely migrating from a ‘reflation’ to ‘mild stagflation.’ ”

He says we are likely in a transition from Strong Growth and High Inflation to Slower Growth and High Inflation, while North American banks are “likely to keep rates on hold.”

As a result, as shown below, BMO is neutral to overweight Equities, underweight Fixed Income, and overweight Alternatives:

Jimmy Xu on the Benefits of Covered Call ETFs

Jimmy Xu, CFA, BMO ETFs

The second talk is by Jimmy Xu, Head of Liquid Alts and Non linear ETFs. His focus was on Covered Call ETFs, which BMO has pioneered in the Canadian market. While investors often buy covered call ETFs just for yield, yield is not the most important consideration, Xu said. “Chasing yield is the quickest way to have unstable income, capital erosion and unhappy clients.” Continue Reading…

I’ve noticed a flurry of articles recently about how investors, including nearing or in the Retirement Risk Zone, might consider moving beyond the traditional 60/40 balanced portfolio of stocks and bonds to consider multiple alternative asset classes.

Indeed, here at FindependenceHub.com we have in the past week run two blogs on specific alternative assets classes: Gold and Bitcoin.

Click on the following headlines to read them if you missed them the first time around:

Admittedly both blogs have a strong point of view that comes from the respective authors. It happens that these two bloggers don’t think much of Gold and Bitcoin respectively. I value their opinion and felt it was worth passing along to readers, who can make their own judgements. Personally, I’ve always believed 5% in Gold or Precious Metals bullion and/or mining stocks is a risk worth taking. I’m a little more skeptical about cryptocurrency but have written in the past that for those inclined to take a flyer on Bitcoin, a 1 or 2% position could work. That 1% could soar and become 10% or more of a total portfolio but it’s also possible that it might indeed descend to zero.

The rest of this blog canvases a baker’s dozen of financial experts and business owners and you’ll see that several of them take a stance on gold and bitcoin, both positively and negatively, as well as numerous other asset classes, such as real estate, private equity, hedge funds and many more.

With the assistance of Featured.com, which has been supplying Findependence Hub with quality content for several years, we recently polled a number of these experts on LinkedIn, as you can see by clicking on their profiles below.

Here’s how we posed the question:

Beyond traditional stocks and bonds, represented in Balanced ETFs, what, if any, alternative asset classes do you recommend, and in what proportions? For example: precious metals (gold or silver bullion or related stocks, or ETFs holding the same), commodities in general, Bitcoin, Ethereum and other cryptocurrencies, real estate held directly or via REITs or certain publicly traded stocks, or any other alternatives not mentioned here, such as Private Equity or Hedge Funds.

1. I recommend gold primarily as geopolitical and inflation insurance, not as a growth asset. Allocate 5-10% of your portfolio to gold via ETFs like GLD or physical bullion if you have secure storage. Silver is more volatile and industrial, so treat it as a smaller speculative position (2-3%) if at all. Gold doesn’t pay dividends or interest, so it’s dead weight in a bull market, but it’s the ultimate “crisis hedge” when currencies or governments misbehave.

2. Direct real estate ownership is capital-intensive and illiquid, so for most investors, publicly traded REITs (Real Estate Investment Trusts) are the smarter play. They provide exposure to commercial, residential, or industrial property with daily liquidity and mandatory dividend payouts. I prefer diversified REIT ETFs like VNQ. This gives you inflation protection (rents rise with prices) and income generation without the headache of being a landlord. Avoid over-concentration here; real estate correlates heavily with the broader economy during downturns.

3. Crypto is not an investment; it’s a volatility lottery ticket with a philosophical thesis. I recommend limiting exposure to 2-5% of your portfolio, and only in the “blue chips” (Bitcoin and Ethereum). Treat this as venture capital: money you can afford to lose entirely. Do not buy crypto with debt, and do not FOMO into altcoins. Store it in a hardware wallet (Ledger, Trezor) if you hold significant amounts; exchanges are not banks. This allocation satisfies your urge to participate in the “future of finance” without risking your retirement if it all goes to zero.

4. Commodities (oil, natural gas, agricultural products) via ETFs like DBC provide inflation protection and diversification, but they are mean-reverting and volatile. Allocate 3-5% as a tactical hedge, especially during inflationary periods. Avoid direct futures contracts unless you are a professional; the contango and rollover costs will eat you alive.

5. Unless you are an accredited investor with $10M+ in liquid net worth, private equity and hedge funds are legally and financially inaccessible or impractical. They charge egregious fees (2% management + 20% performance), lock up your capital for years, and studies show most underperform public markets after fees. If you insist, access them via interval funds or publicly traded BDCs (Business Development Companies), but understand you are paying for illiquidity and complexity, not guaranteed outperformance. — Lyle Solomon, Principal Attorney, Oak View Law Group

Alternative investments should represent twenty per cent of an investor’s total portfolio. In terms of specific allocations, I recommend ten percent in physical gold as a hedge against loss or theft, five percent in real estate investment trusts (REITs) for income generation and three percent in Bitcoin for growth opportunities. Finally, I suggest two per cent be allocated to private equity for both capital gains and diversification purposes. A combination of these types of alternative investments will help protect investors from future inflationary pressures and contribute greatly to their long term performance. Geremy Yamamoto, Founder, Eazy House Sale

Put the most money into things you understand best

My bigger principle is this: Put the most money into the things you understand best.

In my case, that has always been real estate and housing because I know how value gets created there. I know what distress looks like. I know where the discount comes from. I know how people get in trouble. That matters. The more removed an asset is from your real-world understanding, the smaller it should probably be.

And one more thing. Liquidity matters. A lot. People forget that. An investment may look great on paper until you need cash and cannot get to it without taking a beating. That is why I like keeping things simple and staying out of anything that locks you up unless the reward is clearly worth it. — Don Wede, CEO, Heartland Funding Inc.

I’ll break the answer into two parts depending on what your goals are. Growing your assets is one thing, turning your capital into a lifetime income that never runs out is another and that is the #1 financial concern of the 50+ age group.

Purchasing Power Protection is the new Growth strategy:

Historically we used to achieve stable growth by balancing a risk-on asset class (equities) with a risk-off asset class (bonds). In good times the equities flew and the bonds did little; in bad times the bond performance offset declines in equities.

The problem is that in inflationary times, both fall. Inflation undermines the economics of established businesses which have to compete for limited resources that are increasing in price. Positioning for scarcity can insulate you against these circumstances. Gold, Silver and even Bitcoin are the most liquid scarce assets on the planet but they don’t move uniformly. Backing a portfolio with a scarce risk-on asset such as Silver or Bitcoin — while having the majority in a reliable, but occasionally boring, asset like gold — now gives you balance over the longer term. A 30/70 split seems to be the sweet spot.

Assets run out, Lifetime Income is forever:

70% of savers worry about one thing above all others. Can I afford my ideal lifestyle now at the risk of poverty if I live 25+ years? Not everyone will live 25+ years but if I spend now then I am betting against my own longevity. Insurers capitalize on this risk by pooling lives together and promising annuitants a fixed income for life. But fixed incomes lock in the loss of purchasing power. Your lifestyle is going to degrade over time.

It wasn’t always this way. Just over a century ago, 50% of U.S. households joined a longevity risk-sharing arrangement called a Tontine. Recent legislation has enabled modern Tontine Trusts which can be backed by assets that can resist inflation. The Tontine Trusts use your preferred assets to pay you a monthly income for life. When a member dies, their leftover assets top-up the trusts of survivors, typically enabling their monthly income to increase.

So the question the reader really needs to decide upon is: What matters most? The balance of the account or the lifestyle that I always want to enjoy. For generations past, the answer was not to play the markets but rather to invest in yourself.

[Potentially there is a far larger article here, contact us if you want to offer readers a $250 bonus and a similar reward for yourself] — Dean McClelland, Founder/CEO, Tontine Trust Europe KB Continue Reading…