By Mel Bucher, Co-Head of Global Distribution, Martin Currie, Edinburgh, UK

(Sponsor Content)

The investment choices we make can have a profound effect on the world around us. Investing according to sustainable principles allows investors to align their environmental, social and governance (ESG) goals with their investing choices.

Also, we believe sustainability can be a driver of long-term portfolio performance. As global equity markets recover from the COVID-19 pandemic, more Canadians want to invest in opportunities available within a wider sustainable context.

One new option is the sustainability investment expertise that Martin Currie brings to Canada.

Martin Currie may be a new name for many Canadian retail investors. Our firm is a Specialty Investment Manager of Franklin Templeton, based in Edinburgh, UK, and we focus on actively managing portfolios of the listed public equities of companies that generate long-term value from sustainable ESG polices. Our ESG framework helps to identify any material ESG issues related to a company’s cash flow, balance sheet and profit/loss account over time and whether these ESG issues could affect value creation. Having ESG analysis fully embedded in the research process enables our investment teams to uncover material issues.

Martin Currie’s leadership in ESG was recognized with the UN’s Principles for Responsible Investment A+ rating for 2017, 2018, 2019 and 2020.

This article considers our sustainable investing strategies in global equities and emerging markets equities, both of which are now available to Canadians.

A global equity strategy in a global recovery

We expect the strong comeback of the global equity market to be sustained under fairly benign inflation conditions and with asset prices supported by monetary policy. Our global equity strategy is well positioned in this environment.

The Franklin Martin Currie Global Equity strategy invests in companies with exposure to three established growth megatrends:

1. Demographic change (e.g., aging population, urbanization, healthcare)

2. Resource scarcity (e.g., electric vehicles, alternative energy, infrastructure)

3. The future of technology (e.g., outsourcing, cloud computing, security).

We believe these themes will drive long-term structural growth in the global economy. The portfolio seeks diversified holdings with exposures to the megatrends to capture growth.

Global equities for growth, at the right price

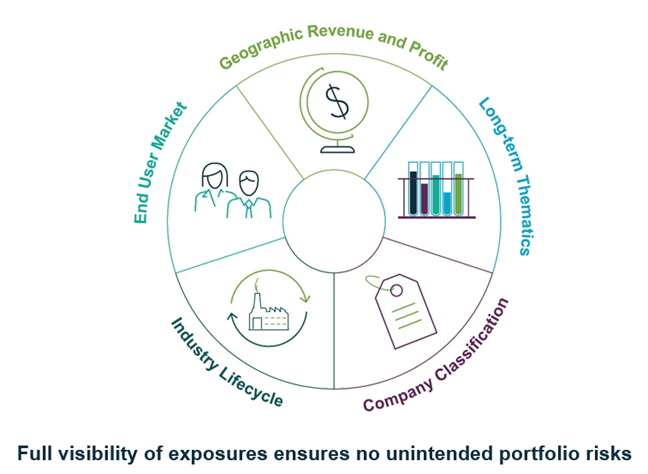

The portfolio holds 20-40 stocks of sustainable, well-managed growth companies that dominate their respective industries and have high barriers to entry. They hold pricing power and face a low risk of disruption. These firms have potential for long-term structural growth and value creation. Companies undergo a systematic assessment of their industry, company, portfolio and governance/sustainability risks.

These equities may not be cheap, so the portfolio managers are highly selective about acquiring companies at the right valuations. The goal is to find equities that combine strong industry, financial and governance attributes at the right price.

This global equity strategy is now available to Canadians through the Franklin Martin Currie Global Equity Fund and Franklin Martin Currie Sustainable Global Equity Active ETF (FGSG). The mutual fund’s U.S. equivalent is a 4-star Morningstar-rated fund* in the International Unconstrained Equity category.

Unique Approach to Portfolio Analysis and Construction