This article has been sponsored by BMO Canada. All opinions are my own.

Fixed income doesn’t get enough attention on this blog, mostly because I’m still in my accumulation years and invest in 100% equities across all my accounts. But most investors should hold bonds in their portfolio to reduce volatility and so they can rebalance (selling bonds to buy more stocks) whenever stocks fall.

In this post we’re going to take a deep dive into BMO’s line-up of fixed income ETFs. We’ll see that there isn’t a one-size-fits-all approach to investing in fixed income, and that investors can capture yield using a wide array of products and strategies.

DIY investors should be familiar with BMO’s suite of fixed income ETFs. It’s the largest in Canada with more than $23 billion in assets. At the top of the list is BMO’s Aggregate Bond Index ETF (ZAG) with total assets of $5.86 billion.

Robo-advised clients also have BMO fixed income ETFs in their model portfolios:

- Nest Wealth clients hold BMO Aggregate Bond Index ETF – (ZAG)

- Wealthsimple clients hold BMO Long Federal Bond Index ETF – (ZFL)

- Questwealth clients hold BMO High Yield US Corp Bond Hedged to CAD Index ETF – (ZHY)

- ModernAdvisor clients hold BMO Emerging Markets Bond Hedged to CAD Index ETF – (ZEF)

BMO Fixed Income ETFs

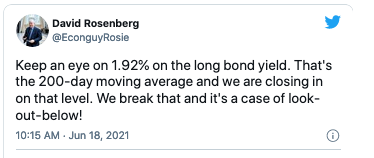

Investors are nervous about holding bonds today. Interest rates are at historic lows, and when rates eventually rise, we’ll see bond prices fall – especially longer duration bonds. We’re also seeing higher inflation, which causes interest rates to go up (and bond values to go down).

Q: Erika, investors are concerned about low bond returns, particularly from long-term government bonds. How should they think about the fixed income side of their portfolio?

A: Investors should think of fixed income as a ballast in their portfolio. It helps reduce overall volatility (chart below). Correlations between US Treasuries and stocks (represented by the MSCI USA index) have been negative over the last two decades. All that to say, when stocks fall, bonds tend to do well.

From an investor perspective, there are two things at play – FOMO, and fear of volatility. Fixed income still has its traditional value in a portfolio; to offset equity risk.

What we are seeing from some clients is the willingness to take on more equity risk – shifting from a 60/40 balanced portfolio to 70/30 portfolio, as an example.

But you can see the payoff from fixed income using a simple example of Canadian equities (represented by ZCN) and ZAG. Volatility drops materially without costing investors too much return.

| ETF | 10-year annualized return | Standard deviation |

|---|---|---|

| ZCN | 6.21% | 11.8% |

| ZAG | 3.69% | 4.0% |

| 60/40 (ZCN/ZAG) | 5.38% | 7.4% |

| 70/30 (ZCN/ZAG) | 5.61% | 8.5% |

The bottom line: Fixed income keeps investors in the markets during times of distress.

Q: What about a retired investor who typically holds a 60/40 or 50/50 portfolio but is concerned about generating income in a low-yield environment?

A: Such an investor may wish to include ETFs that harness option-writing strategies such as covered call writing, put writing, or a combination of the two, to generate a high level of tax efficient monthly cash flow (option premiums are taxed as capital gains and/or return of capital).

With fixed income generating lower yield today, the equity portion of a portfolio needs to make up for the yield shortfall. Covered call strategies are an efficient way to do so and ETFs are a convenient way that allow investors to attain access.

Here are a few examples of these types of strategies. I would include these on the equity side of the portfolio to increase overall level of yield:

- ZWC BMO Canadian High Dividend Covered Call ETF, yields 7.3%

- ZWB BMO Covered Call Canadian Banks ETF, yields 5.84%

- ZWS BMO US High Dividend Covered Call Hedged to CAD ETF, yields 5.94%

Q: I’m a big fan of asset allocation ETFs to make DIY investing as simple as possible. But is it wise to unbundle ZGRO or ZBAL and hold multiple ETFs with the intention of avoiding long-term bonds in favour of shorter duration government bonds or corporate bonds?

A: Part of the appeal of the all-in-one asset allocation ETFs is their simplicity; and they tend to appeal to investors who do not want to get granular in their investment process. The other benefit of a one-line holding is that you are less likely to overthink the underlying components and make reactive decisions when you see something go into the red.

The 0.18 % management fee (0.20% MER) for ZGRO and ZBAL are all-in, there’s no double-dipping on fees. That is basically the cost of underlying ETFs with almost nothing more for the rebalancing. Keep in mind that there is often a trading cost for rebalancing multiple ETFs on your own. For investors with small portfolios, the cost of selling and buying stocks and bonds every year can become proportionally expensive.

Portfolio rebalancing is the maintenance involved in sticking with your asset allocation plan. Your asset allocation plan is what is going to help you meet your goals. One of the biggest pros to portfolio rebalancing is that it keeps risk under control, and sometimes just maintaining a level of risk takes some action.

There is tremendous value to having the rebalancing done systematically. Conservatively, experts say it can add between 0.30% to 0.40% annually over the long term.

For an investor who does not mind doing a handful of trades and rebalancing once or twice a year, the “unbundling” strategy could work. However, if the concern is rising rates, corporate bonds would tend to do better than government bonds. Continue Reading…