New research from a colleague has me thinking about hindsight. The trouble, as the saying goes, is that hindsight is 20/20 — and you can’t benefit from it after the fact.

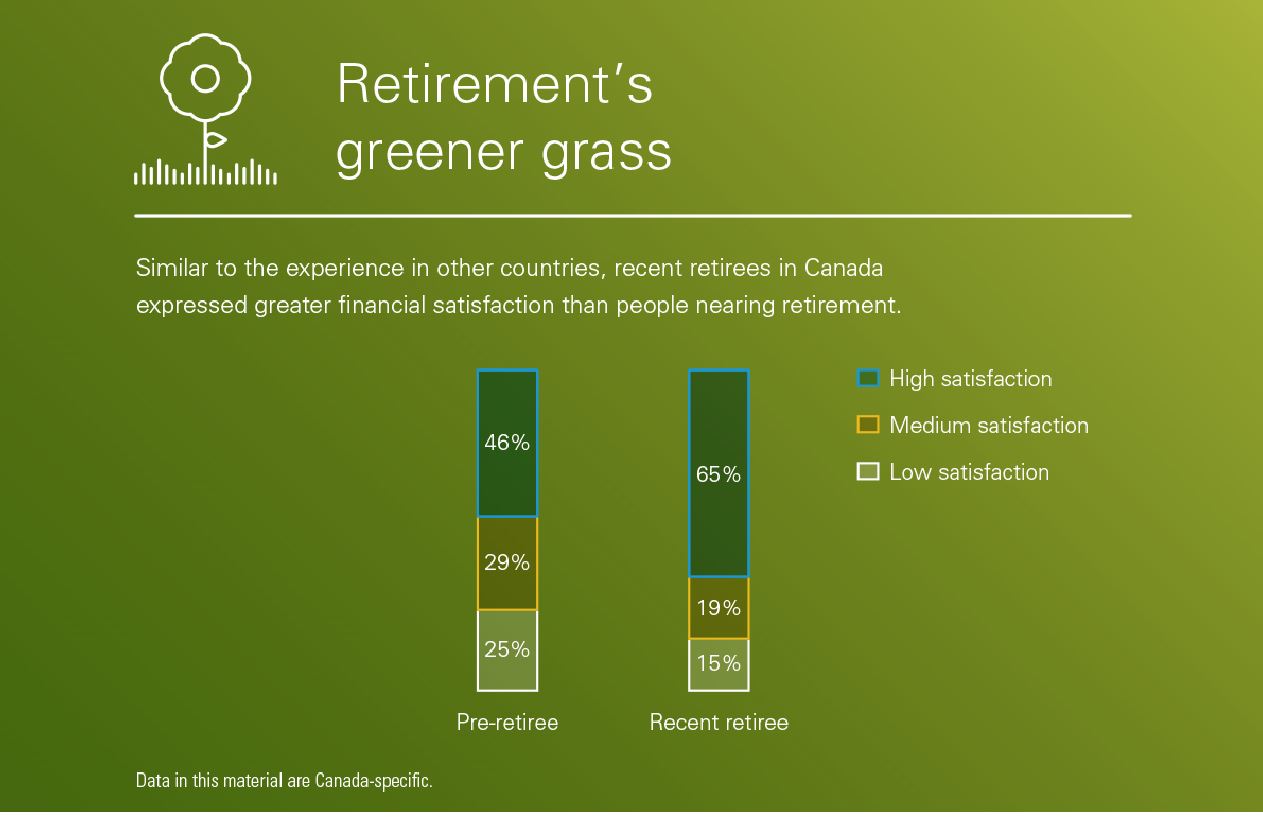

But why not try to benefit from someone else’s hindsight? My colleague Anna Madamba of the Vanguard Center for Investor Research found in a new study that recent retirees were largely satisfied with their financial situations in retirement, but, if they could, would still do some things differently in preparation.

With the benefit of retrospect, 43% of Canadian survey respondents “agreed” or “strongly agreed” that they would have saved more — a higher percentage than garnered by any other answer.

But perhaps it’s too simple to suggest that pre-retirees should just follow the example of others. Many people know at some level that they need to save more. Whether they do often comes down to two things: competing priorities and insight into how much money they’ll have (and need) in retirement.

I recently had a chance to discuss a new Canadian advisory on dividend stocks with the people responsible for that newsletter. The advisory comes from TSI Network, founded by Pat McKeough, whose investment approach I have always respected.

The advisory is TSI Dividend Advisor (shown above), and it grew out of a long respect for the power of dividends.

Pat and his investment team have always viewed dividends as a sign of investment quality. By extension, dividend stocks become the most reliable foundation of an investment portfolio built for growing wealth and financial independence.

This confidence in dividends is accompanied by a detailed examination of dividend-paying stocks to identify those with the greatest potential to sustain, and raise, their payouts.

The 8 key points they use to evaluate dividend stocks grew into their Dividend Sustainability Ratings. This proprietary ratings system became the backbone of the new TSI Dividend Advisor. It was launched late in 2016 to impressive reviews in the media and a flood of subscriptions from Canadian investors.

Here are some of the keys to that success, from the editors’ point of view.

Jon Chevreau: First of all, Pat, thanks for your time. What role do dividends play in a successful portfolio? How can they lead to Findependence?

Pat McKeough

Pat McKeough: Top dividend stocks are a key part of a successful portfolio. Top dividend stocks can produce as much as a third of your total return over long periods. These payouts are drawn from earnings cash flow and paid to the shareholders of the company. Typically, these dividends are paid quarterly, although they may be paid annually or monthly as well.

At TSI Network, we think investing in dividend stocks is one of the best investment decisions you can make to achieve Findependence. Dividends serve as a way for companies to share the wealth they accumulate through successfully operating their businesses.

JC: Manystocks have dividends. What makes a top dividend stock?

Jon Chevreau

PM: Top dividend stocks provide steady dividends: a sign of investment quality. Some good companies reinvest profits instead of paying dividends. But fraudulent and failing companies hardly ever pay dividends. So if you only buy stocks that pay dividends, you’ll automatically stay out of almost all the market’s worst stocks. For a true measure of stability, focus on companies that have maintained or raised their dividends during economic and stock market downturns. These firms leave themselves enough room to handle periods of earnings volatility. By continually rewarding investors, and retaining enough cash to finance their businesses, top dividend stocks provide an attractive mix of safety, income and growth. Continue Reading…

There is something very wrong with the work world today. It is far too common to find employees who are tired, over-worked, stressed out, and living in fear of an uncertain future.

As a result, people are eating too much, watching too much television, and complaining too much, often self-medicating with drugs and/or alcohol or taking prescription medication to cope with their stress.

How can it be that in North America, with two of the most prosperous societies in the world, people are taking more medications for anxiety, depression, and sleep disorders than ever before?

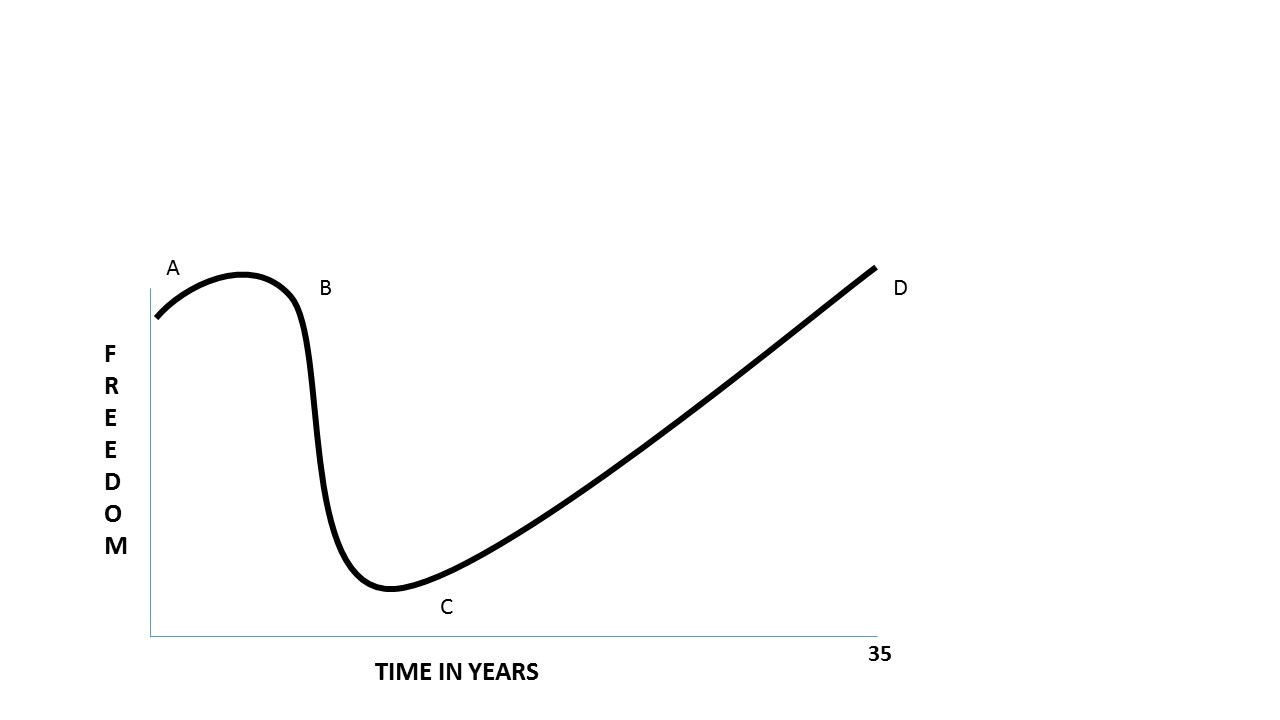

Blame it on the big dip.

The graph above represents a typical person’s (mine) working lifecycle. I call it the “big dip” as it’s only fair to recognize Seth’s influence on the development of the concept.

You will note two axises, the vertical one representing personal freedom and the horizontal one representing time spent in years. The graph isn’t to scale but it does get the point of the story across. Be warned, it might scare you: it gave me the jitters when I first drew it so you might want to sit down for this one.

Entry point A is when you leave school and start working, maybe in a “corp.,” like I did. It’s a happy time. Life is fun and exciting and you do not have any significant worries. You are finally making some real money for the first time. One could reasonably say a person at this point is financially independent. They carry no personal debt, their parents still provide them with a roof over their head and food on the table. Life is as simple as it could be. Work-Eat-Have Fun-Repeat.

Everyone’s goal at this point is similar. Work hard, get promoted and make more money. This was the path to success as taught to them by their parents and teachers and every kid wants to look successful in the eyes of their parents, right? Continue Reading…

We recommend that you base your investing for retirement on a sound financial plan. Here are the four key factors that your plan should address to ensure that your retirement investing generates enough income in retirement:

1.) How much you expect to save prior to retirement;

2.) The return you expect on your savings;

3.) How much of that return you’ll have left after taxes;

4.) How much retirement income you’ll need once you’ve left the workforce.

Stick with conservative estimates to account for unforeseen setbacks

As for the return you expect from investing for retirement, it’s best to aim low. If you invest in bonds, assume you will earn the current yield; don’t assume you can make money trading in bonds.

Over long periods, the total return on a well-diversified portfolio of high-quality stocks runs to as much as 10%, or around 7.5% after inflation. Aim lower in your retirement planning —5% a year, say — to allow for unforeseeable problems and setbacks.

Above all, it’s important to remember that while finances are important, the happiest retirees are those who stay busy. You can do that with travel, golf or sailing. But volunteering, or working part-time at something you enjoy, can work just as well.

One thing we encourage all investors to do is perform a detailed study of how you spend your money now. Then, you analyze your findings to see what personal expenses you can cut or eliminate. This too can have fringe benefits, especially if it helps you break unhealthy habits. You may be surprised at how much you’re spending and how much more you could be saving for retirement.

TFSA vs. RRSP is one of the most common questions I am asked. If you want to know for sure which is better for you, then you need a financial plan.

Many articles have been written on this topic that list pros and cons with general opinions.

The truth is that:

1.) Rather than just having an opinion, there is a precise right answer specifically for you. To the extent that you know your present and future marginal tax brackets, you can calculate a precise optimal contribution for RRSP and TFSA for each year, as well as the optimal amounts to withdraw each year after you retire.

2.) The decisive factor is your tax brackets now vs. after you retire. Most people just assume they will be in a lower tax bracket after they retire, because their income will be lower. In many cases, that is not true.

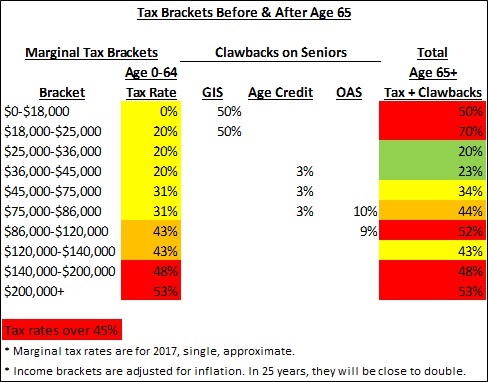

When you include the clawbacks of government income programs that affect everyone over 65, many seniors are in shockingly high tax brackets!

The clawbacks cost you actual money and are the same as a tax. The three main clawbacks are the 50% clawback on GIS for low incomes (under $20,000), 15% clawback on the age credit for middle incomes ($35,000-85,000), and the 15% clawback on OAS for higher incomes ($75,000-120,000).

The chart above shows the actual approximate tax brackets before and after age 65. Check out the tax brackets over 45% in red:

Understand the differences

You can own the same investments in your TFSA as your RRSP. The main difference is that RRSP contributions and withdrawals have tax consequences, while TFSA contributions and withdrawals don’t.

Therefore, the answer to TFSA vs. RRSP is primarily based on your marginal tax bracket today compared to when you withdraw after you retire: Continue Reading…