My latest MoneySense Retired Money column takes a look at how a new Government program can be used by young people to save up tax-effectively for a first home: including the children of retirees and the almost-retired. For the full column, click on the highlighted text: How retired parents can use the FHSA to help their adult children.

The new First Home Savings Accounts [FHSA] should be operational by April 1, 2023. At least two regular bloggers who often appear here on the Hub have weighed in with summaries of the program. Dale Roberts’ take appeared on his cuthecrapinvesting blog on March 1st. Mark Seed’s myownadvisor blog ran a summary of the key points on March 4th.

For MoneySense and Retired Money, I took a bit of a different take, seeing as the column’s focus technically is on Retirees and near-retirees. These days, that category consists primarily of aging baby boomers like myself, but of course many of us have adult children who may have been slow to jump into the real estate market with home prices in places like Vancouver and the GTA soaring in recent years during the long spell of almost-free money. That era has of course ended with the Bank of Canada gradually raising rates over the past year, which has also helped to push home prices down to slightly more reasonable levels.

Whether they become even more reasonable remains to be seen but of course the positive of slightly lower prices is offset by higher mortgage rates so it’s a bit of a Hobson’s choice. You can wait and hope for the proverbial “blood in the streets” to hit home prices and make the plunge into ownership then, but there’s no guarantee that will happen.

Either way, if Ottawa is providing another tax-optimized way to save up a down payment, why not take advantage of it? We already have the RRSP home-buying program [HBP] and there’s no reason why TFSAs can’t also be used for the same purpose. What’s nice about the new FHSA is that not only does it tax-shelter investment income but it also provides a tax refund on contributions, similar to how RRSPs do so. (as the above blogs note, there are differences however.)

The Home Savings plan we all dreamt of

As quoted in the MoneySense column, CFP and RFP Matthew Ardrey, Wealth Advisor & Portfolio Manager with Toronto-based TriDelta Financial provides the following enthusiastic thumbs up for the new program: “The FHSA is the home savings plan we were all dreaming of when we first got the HBP. Combining the best aspects of the RRSP, tax deductions for contributions, and the TFSA, tax-free qualifying withdrawals, this can be a game changer for the next generation of homebuyers in Canada.” Continue Reading…

When we started our financial independence journey back in 2011, we didn’t set a specific FI date or number. In our minds, we do not doubt whether we could become financially independent or not. We knew we’d become financially independent in the future. It was just a question of time. We simply needed to have patience and let our investments compound over time.

A few years into our FI journey, our FI plan started to evolve. Rather than having a specific liquid net worth and utilizing the 4% safe withdrawal rule, we decided to have enough dividend income to cover our expenses. Looking at the calendar, we randomly set a target of reaching this milestone by 2025 or earlier.

It’s funny how ten years seemed to have gone by in the blink of an eye. At the same time, a lot has happened in our lives…

Getting engaged and married

Having two kids

Moving from an apartment in Vancouver to a house in the suburb

Me having different job titles, going from engineering to project managing to product marketing to engineering

Starting my photography business ( I’ve been on a bit of break the last few years)

Starting this blog, writing articles, learning new things, and connecting with other like-minded people

One thing I’ve realized is that life is never static. It’s always dynamic. Although we can do as many projections and make as many plans as we possibly can, projections and plans do and will change. Therefore, with three years to go before 2025, I thought it would be a good time to re-examine our financial independence plans and see if we need to make any adjustments.

Our FI numbers

Since starting our FI journey, we have tracked our expenses meticulously. Here are our annual expenses since 2012:

Total Necessities

Total Annual Spending

2012

$26,210.52

$44,603.76

2013

$26,343.00

$45,260.88

2014

$29,058.96

$47,391.96

2015

$31,256.88

$47,270.16

2016

$29,831.40

$47,566.96

2017

$33,887.68

$51,144.77

2018

$31,840.75

$57,231.99

2019

$33,199.98

$54,906.02

2020

$35,511.60

$48,908.74

2021

$38,950.66

$71,852.02

Necessities cover core expenses like food, insurance, housing, clothing, utilities, car, etc. Other expenses are considered as non-core expenses which include things like dining out, skiing, camping, travel, charitable donations, gifts, etc.

The last two years have been abnormal in terms of spending. Due to the pandemic, our spending was much lower than usual in 2020. Then last year we had unplanned expenses of around $16,500 on our cat and our house. If we take this amount out, it’d put our 2021 annual spending to around $55,000.

Based on our historical spending trend, I would estimate that we need somewhere between $50,000 to $60,000 in dividend income annually to cover our expenses. To be on the safe side, I’d use $60,000 annual spending for any FI plans because we need to have inherent built-in flexibility on variables outside of our control, like major purchases, emergencies, etc.

The $60k annual spending estimate, of course, assumes that we continue to live in Vancouver and do not have many significant changes in our spending habits.

One thing to keep in mind is our spending can drastically come down if we decide to geo-arbitrage by moving to a smaller Canadian town or somewhere in South East Asia with a lower cost of living than Vancouver. On the flip side, the spending number can increase if we move to Denmark and live there for a few years (I’m ignoring the tax consequences for now).

How much do we need in our dividend portfolio?

How much do we need in our dividend portfolio to generate $60,000 in dividend income? Let’s do a quick math exercise, shall we?

For $60,000 dividend income per year, at 3% dividend yield, we’d need a dividend portfolio worth $2 million; at 4% dividend yield, we’d need a dividend portfolio worth $1.5 million. In other words, we need a portfolio valued between $1.5 million to $2 million. That’s certainly not a small chunk of change.

Now, if we take a middle-of-the-road approach and use a portfolio dividend yield of 3.5%, that means a portfolio value of around $1.714 million.

One thing is clear – we need to continue to save and invest money in our dividend portfolio. We also need to find the right mix between high-yield low-dividend growth stocks and low-yield high-dividend growth stocks.

With three years remaining in our FI timeline, it might be tempting to start buying more very-high-yield dividend stocks to make sure we can reach our FI target. But it is very important to make sure our dividend income is safe and remains sustainable over time. We definitely don’t want to hit $60,000 in dividend income one year only to see that amount slashed by 20% or more the next year.

The stability of our dividend income is extremely vital.

We also want to make sure the portfolio value continues to appreciate over time. The rationale is simple – total returns matter. Having a stable and safe dividend income and a portfolio that increases value over time will give us more options.

By 2025, both Mrs. T and I will be in our early 40s. With decades ahead of us, we need to ensure our dividend income can grow organically over time and inflation doesn’t eat into our dividend income’s buying power. It will be necessary to have some low-yield high-dividend growth stocks in our portfolio to allow for organic dividend growth.

The plan of living off dividends

Living off dividends is an amazing idea. Based on my dividend income projection, we should receive $51,000 in dividend income in 2025. However, when we compare that number with the $60,000 annual spending target, it doesn’t take a rocket scientist to realize that we are short by several thousand dollars. Continue Reading…

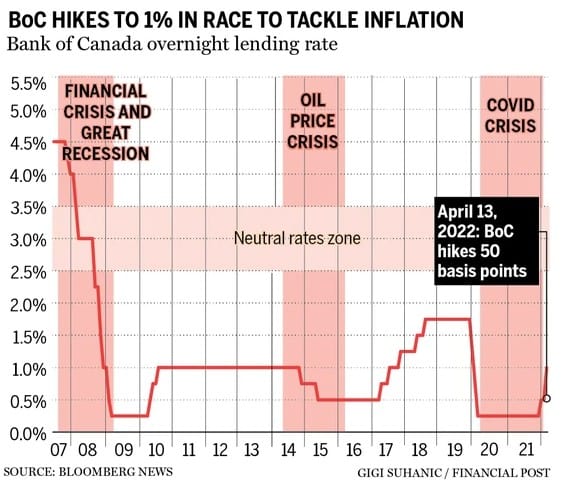

Lately, the talk of the town seems to be rising interest rates. In April, the Bank of Canada raised the benchmark interest rate by a whopping 0.5% to 1%, making it the biggest rate hike since 2000. Given the high inflation rate, it is almost a given that these rate hikes will continue throughout 2022 and beyond. [On July 13, 2022, the BOC hiked a further 1%: editor.]

But before you freak out, let’s step back and look at the big picture. At 1%, the benchmark interest rate is still relatively low compared to the past interest rates.

I still remember years ago before the financial crisis, being able to get GIC rates at around 5%. And some people may remember +10% interest rates in the 80s or early 90s. Back then, interest rates were much much higher than measly below 1% rates we’ve been seeing the last decade.

Historical BoC overnight rates

What’s going to happen to the stock market? Well the general rule is that when Bank of Canada or the Federal Reserve cuts interest rates, the stock market goes up. When Bank of Canada or the Federal Reserve raises interest rates, the stock market goes down.

According to BMO’s annual Investment Survey, Gen Z is now Canada’s most engaged generation for tracking financial goals.

Younger Canadians are flexing their financial savvy by evaluating their financial goals and plan more frequently than any other cohort: including Boomers!

According to the survey, 62% of Gen Z (aged 18-25) and 54% of Millennials (age 26-41) review their financial goals at least quarterly, with 41% of Gen Z and 29% of Millennials doing so monthly. In comparison, only a third (36%) of Boomers (aged 58-67) review their financial plans at least once a quarter and only 15% of them do so monthly.

“It’s exciting to see the next generation of Canadians building solid financial habits and establishing a foundation early” said Nicole Ow, Head, Retail Investments at BMO, in a press release, “Real financial progress is a lifelong pursuit as our goals and circumstances change throughout our lifetime. We encourage Canadians of all ages to consider ways not only to grow their wealth and work towards immediate financial goals, but also to ask their advisor how they can align their investments with their values, define their longer-term goals, and protect and share their wealth with their loved ones and the causes that mean the most to them.”

Social media a big influence

While the survey found the majority of young Canadians rely on advice from a professional when making financial decisions, what’s more interesting is the additional sources they are seeking out for guidance. Many are currently working with a financial advisor, and 47% of Gen Z and 32% of Millennials say they were referred to their advisors on the advice of a trusted friend or family member. The impact of social media on the financial habits of young Canadians also mustn’t be overstated. A third of Gen Z and 22% of Millennials refer to financial influencers and social media for their investment decisions. In comparison, only 7% of Canadians over 55 utilize these sources.

Barriers to Entry

Among younger Canadians with savings primarily held in cash, half of Gen Z and close to two fifths of Millennials say the primary reason for this is that they do not know how to invest. Whether it’s not knowing where to begin, or being unsure who to trust with their finances, a lack of basic financial literacy skills being taught in schools may be partly to blame for this. Thankfully, the previously mentioned alternate sources that young Canadians seek out can help to educate those feeling overwhelmed. Continue Reading…

The federal government kept the annual TFSA contribution limit at $6,000 for 2022: the same annual TFSA limit that we had since 2019. It’s still good news for Canadian savers and investors, who as of January 1, 2022, have a cumulative lifetime TFSA contribution limit of $81,500.

The Tax Free Savings Account (TFSA) was introduced in 2009 by the federal conservative government. The TFSA limit started at $5,000 that year: an amount that “will be indexed to inflation and rounded to the nearest $500.” The TFSA limit is expected to increase to $6,500 in 2023.

TFSA Contribution Limit since 2009

The table below shows the year-by-year historical TFSA contribution limits since 2009.

Year

TFSA Contribution Limit

2022

$6,000

2021

$6,000

2020

$6,000

2019

$6,000

2018

$5,500

2017

$5,500

2016

$5,500

2015

$10,000

2014

$5,500

2013

$5,500

2012

$5,000

2011

$5,000

2010

$5,000

2009

$5,000

Total

$81,500

Note that the maximum lifetime TFSA limit of $81,500 applies only to those who were 18 or older as of December 31, 2009. If you were born after 1991 then your lifetime TFSA contribution limit begins the year you turned 18.

You can find your TFSA contribution room information online at CRA My Account, or by calling Tax Information Phone Service (TIPS) at 1-800-267-6999.

TFSA Overview

The Tax Free Savings Account is a flexible vehicle for Canadians to save for a variety of goals. You can contribute every year as long as you’re 18 or older and have a valid social insurance number.

That means young savers can use their TFSA contribution room to establish an emergency fund or save for a down payment on a home. Long-term investors can use their TFSA to invest in ETFs, stocks, or mutual funds and save for the future. Retirees can continue to save inside their TFSA for future consumption or withdraw from their TFSA tax-free without impacting their Old Age Security or GIS.

Unlike an RRSP, any amount contributed to your TFSA is not tax deductible and so it does not reduce your net income for tax purposes.

Your contribution room is capped at your TFSA limit. Excess contributions will be taxed at 1 per cent per month

Any withdrawals will be added back to your TFSA contribution room at the start of the next calendar year

You can replace the amount of your withdrawal in the same year only if you have available TFSA contribution room

Any income earned in the account, such as interest, dividends, or capital gains is tax-free upon withdrawal

How to open a TFSA

Any Canadian 18 or older can open a TFSA. You are allowed to have more than one TFSA account open at any given time, but the total amount you contribute to all of your TFSA accounts cannot exceed your available TFSA contribution room.

To open a TFSA you can contact any bank, credit union, insurance company, trust company or robo-advisor and provide that issuer with your social insurance number and date of birth.

The most common type of TFSA offered is a deposit account such as a high-interest savings account or a GIC.

You can also open a self-directed TFSA account where you can build and manage your own savings and investments.

Qualified TFSA Investments

That’s right: you’re not just limited to savings accounts and GICs. Generally, you can put the same investments in your TFSA as you can inside your RRSP. These types of allowable investments include:

Cash

GICs

Mutual funds

Stocks

Exchange-Traded Funds (ETFs)

Bonds

You can contribute foreign currency such as USD to your TFSA. Note that your issuer will convert the funds to Canadian dollars. The total amount of your contribution, in Canadian dollars, cannot exceed your TFSA contribution room.

If you receive dividend income from a foreign country inside your TFSA, the dividend income could be subject to foreign withholding tax.

Gains inside your TFSA

Some investors may be tempted to put risky assets inside their TFSA account to try and earn tax-free capital gains. There are two advantages to this strategy: Continue Reading…