Here’s my latest MoneySense blog, which tells the story of my first week with the Apple Watch. I’ve added some photographs below that show the packaging.

By Jonathan Chevreau

Over the years, I’ve been both an early adopter of technology devices as well as, on occasion, a late adopter. Early with notebook computers and the first Macintosh in 1984, but late with the Blackberry and the iPhone.

As someone who didn’t even wear a traditional watch, the hype over Apple’s new Watch intrigued me. As I wrote a few weeks ago here at MoneySense.ca, I decided I’d become an early adopter of the Apple Watch, preordering it the day after it was permitted. Continue Reading…

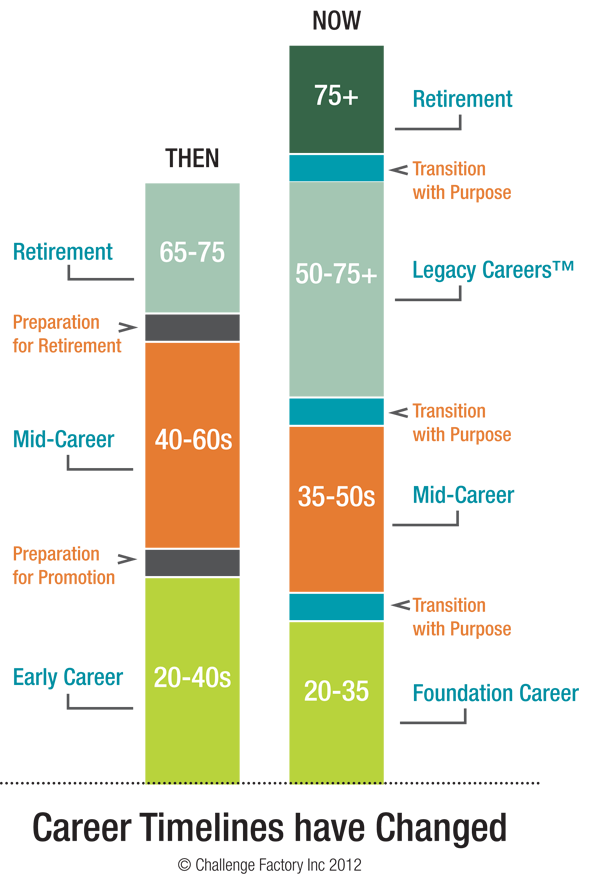

Regular Hub readers will know that if I had my druthers, the headline would read more like “Why Work won’t end after your Findependence Day.” (that is, the day you achieve Financial Independence).

I don’t view the terms Retirement and Financial Independence as interchangeable. By definition, Retirement (or at any rate, traditional full-stop Retirement funded with a generous Defined Benefit pension) means no longer working for money. Financial Independence (aka Findependence), on the other hand, can occur years and even decades before traditional Retirement and so seldom means the end of productive work.

This very web site — which just passed six months in existence — is dedicated to clarifying this distinction. And of course the site also constitutes a big element of my own personal Encore Act: next Tuesday will be the one-year anniversary of my own Findependence Day. In my case, I define that as no longer working as an employee of a giant corporation or government entity, and having the financial resources to work if I choose to, and not if I don’t.

Have you ever moved and forgotten about an old bank account? The Bank of Canada holds about $532 million dollars of unclaimed money dating back to 1900.

Where does the money come from?

Bank of Canada unclaimed balances are Canadian dollar deposits or negotiable instruments that were held at a bank or trust company. They include chequing and savings accounts and GICs, as well as uncashed bank drafts, certified cheques and travellers’ cheques.

Today’s Hub review is a bit unusual in that we’ve allowed an author to review her own book. I originally reviewed No Hype: The Straight Goods on Investing Your Money when it came out almost a decade ago and found it a useful addition to the genre, seeing as so many financial books these days are written by financial professionals.

It was refreshing to see a book written by a pure financial consumer like Gail, who like the rest of us has to sort the financial wheat from the chaff and has no real axe to grind. As she says on her web site, she’s an independent voice.

Hopefully we’ll review it in the more traditional manner over the coming weeks or months but in the meantime, it’s nice to know the book is still out there and has been revised.

Incidentally, and as noted in Saturday’s weekly wrap, Gail and I are among six speakers at The Financial Show in Mississauga later this month. Joining us will be Gordon Pape, Pat Bolland, Jim Ruta and Scot Blythe. — Jonathan Chevreau

By Gail Bebee,

Special to the Financial Independence Hub

Gail Bebee

When I set out in 2006 to write the original No Hype – The Straight Goods on Investing Your Money, my goal was to create a readable book that set down all the investing basics for Canadians, without a financial industry bias. It was born from my frustration at not finding such a book when I decided to take control of investing my money.

Thousands of books and two sold-out editions later, the students taking my Investment Planning night school course at Toronto District School Board still need a good reference, and retail investors are still looking for an objective, understandable book on all the investing basics written expressly for Canadians. Continue Reading…

In the recent Federal Budget, the government listened to seniors and advisors and reduced the minimum withdrawal amounts for RRIFs (Registered Retirement Income Funds). But did they go far enough?

If you’re not familiar with minimum withdrawal amounts, here’s a quick overview:

Up until the time you’re age 71 (or if your spouse is younger, their age 71) and you’re earning an income, you can contribute money on a tax deductible basis to a personal or spousal RRSP (Registered Retirement Savings Plan).

When you reach age 71 you have a decision to make. The decision is, do you convert your RRSP to a RRIF, an annuity, or do you cash it out (or a combination of the three). If you choose to convert it to a RRIF, the income payments cannot be deferred any longer than the following year (age 72). Continue Reading…