My latest MoneySense Retired Money column looks at the Iran conflict that erupted suddenly late in February: you can find the full column here: How Retirees should respond to the Iran Crisis.

On Tuesday, the day after Trump TACO’d over his threat to attack Iran’s oil infrastructure (a 5-day reprieve that calmed stock markets at least for the week ending March 27th) Findependence Hub ran a blog that collected input from 14 financial advisors and business owners based largely in the United States. Those sources were collected via a partnership with long-time contributor Featured.com, which works with Linked In to select input. You can find the resulting column here: Financial Experts and Business Owners on what if any moves Retirees should consider if Iran War drags on.

You can get the gist of the messages those experts sent by quickly scrolling down through an admittedly long blog and reading the subheadings highlighted in Blue in the original post. Below I append my favourites, some of which I flagged on social media. If you find the headline summaries intriguing, you’ll find the accompanying observations useful, if not actionable:

Avoid Knee-jerk Liquidation

This is more of a rebalance-and-defend moment than a reason to overhaul the portfolio

Put Capital Preservation over Aggressive Growth

Seek Robust diversification across asset classes and sectors

Rebalance toward defense, yes. Blow up your entire strategy? No.

Make sure existing Allocation is suitably Defensive and Liquid

Don’t over-rotate into a single ‘safe’ bet that can whipsaw when the narrative changes

Remain diversified enough to absorb uncertainty

Reduce volatile individual Growth Names but maintain Diversified Index Funds

Move from Sector Rotation to Structural Resilience

Canadian perspective, with CUSMA renewal looming

The MoneySense column focuses more on the Canadian situation, with input from Toronto-based advisors like John De Goey, Matthew Ardrey and Steve Lowrie, all of which should be familiar to readers of this site and the Retired Money column.

See also a recent blog on Stagflation penned by Dale Roberts of the Retirement Club and cutthecrap investing. Among his many suggestions, the most valuable may be his emphasis on maintaining an “All-Weather Portfolio” catering to all four possible economic quadrants: Inflationary Growth, Disinflationary Growth, Stagflation and Deflation/Recession. Continue Reading…

Since we last polled financial experts and business owners about the prospects for investing throughout 2026, the surprise war in Iran late in February has decidedly upset the apple cart.

These experts were gathered with the assistance of Featured.com, which has been supplying Findependence Hub with quality content for several years. It has changed its procedure so editors like myself can request input on particular topics we think will interest our readership. The sources are all on LinkedIn, as you can see by clicking on their profiles below.

Here’s how we posed the question about how retired or almost-retired clients might approach their portfolios in light of the Iran conflict:

What defensive strategies do you suggest for retirement-age clients concerned that the Iran war will drag on long enough to impact their nest eggs? Defensive ETFs, gold, utilities or what? Any major shift in Asset Allocation?

Below are the 14 responses that caught my attention, but so many were coming in that I wanted to publish this blog before events overtook the observations and recommendations. I am also doing a followup Retired Money column for MoneySense.ca that will likely run in the next week, which focuses more on Canadian input from domestic experts. This site will run a “throw” to that column once it appears.

The events of the past weekend (March 21 – March 22nd) are typical of the chaos and uncertainty that abound under a rogue American president. Typically, the weekend began with a threat to bomb Iran’s power plants if they didn’t re-open the Strait of Hormuz in 48 hours.

That likely ruined the weekend for many investors but also typical, just hours before U.S. markets opened Monday, Trump provided a 5-day reprieve, causing stocks to surge and oil to fall back to more acceptable prices. As this was everywhere online and in broadcast media yesterday, and will be the main topic in Tuesday’s papers, I won’t recap further, beyond this observation:

This is of course another instance of the so-called TACO Trade: for Trump Always Chickens Out. Unless of course the next time he doesn’t.

So on with our perspective from U.S. business owners and financial experts, keeping in mind that these were submitted before this weekend.

“Protect purchasing power and smooth volatility while still allowing the portfolio to grow over time.”

For retirement age clients worried that a prolonged conflict could affect markets, most advisors focus less on drastic changes and more on defensive diversification and income stability. The goal is protecting capital and reducing volatility rather than chasing returns.

Here are a few commonly recommended strategies:

1. Increase exposure to defensive sectors

Sectors that provide essential services tend to hold up better during geopolitical or economic stress. These include utilities, healthcare, and consumer staples because people still need electricity, medicine, and basic goods regardless of the economy. ETFs tracking these sectors are often used as defensive holdings since they tend to have lower volatility and consistent dividends.

2. Add a modest allocation to gold

Gold has historically acted as a “safe haven” during geopolitical crises and financial instability. Many retirement portfolio strategies suggest holding around 5 per cent to 15 per cent in gold or gold ETFs as a hedge against market stress, inflation, or currency risk.

3. Maintain or increase high-quality bonds

Government bonds and investment grade bonds often act as a buffer when equities become volatile. Defensive retirement strategies typically include high quality bonds and dividend paying assets to stabilize portfolio income and reduce drawdowns.

4. Use defensive ETFs rather than individual stocks

Broad ETFs that track utilities, healthcare, real estate, and gold are often used to diversify risk. For example, defensive portfolios sometimes include sector ETFs tied to utilities or healthcare alongside treasury and gold exposure to hedge against market shocks.

5. Avoid major asset allocation shifts driven by headlines

Even during geopolitical tension, most advisors caution against dramatic portfolio changes. The focus is usually on gradual rebalancing, ensuring the portfolio is aligned with the investor’s risk tolerance and time horizon rather than reacting to short term events.

Bottom line: For retirees concerned about geopolitical risk, the typical approach is not a complete overhaul but a defensive tilt:

Maintain diversified equity exposure

Add defensive sectors

Keep a strong bond allocation

Consider a modest gold position

Focus on income-producing assets

This kind of structure helps protect purchasing power and smooth volatility while still allowing the portfolio to grow over time. — Omer Malik, CEO, ORM Systems

“Avoid Knee-jerk Liquidation.”

As an attorney who has guided clients through Desert Storm, 9/11, and the Great Recession, I move immediately to suppress the urge to panic. War is tragic for humanity, but historically, the stock market treats it as a temporary injunction rather than a permanent dismissal. The worst financial crime you can commit right now is a “knee-jerk liquidation.”

Selling your entire portfolio because of a headline is how you turn a temporary paper loss into a permanent reduction in your standard of living. History shows that while markets jitter at the sound of cannons, they often rally once the uncertainty resolves. Therefore, we do not make major shifts in Asset Allocation based on fear; we make minor tactical adjustments based on risk management.

For defensive strategies, I advise a pivot toward the “Boring Sector.” This means Utilities (XLU) and Consumer Staples (XLP). Regardless of what happens in the Strait of Hormuz, people still need to turn on the lights, brush their teeth, and wash their clothes. These sectors are the “tenured professors” of the market: they aren’t exciting, but they have reliable cash flow and pay dividends that can cushion the blow of a downturn. They act as a legal defense against volatility.

Regarding Gold, view it not as an investment, but as a “geo-political insurance policy.” Allocating 5% to 10% to a gold ETF (like GLD) or physical bullion is prudent. It creates a “hedge” because gold often moves inversely to the dollar and panic. However, do not go “all in.” Gold generates no cash flow; it just sits there looking pretty. It is the airbag, not the engine.

Finally, consider the specific nature of this conflict: Energy. Iran is a major energy player. If the conflict drags on, oil prices will likely spike. Holding a diversified Energy ETF (XLE) acts as a natural hedge for your personal budget. If you are paying more at the gas pump, you might as well be earning dividends from the oil companies to offset the pain. Combine this with short-term US Treasuries (SGOV or SHV), which are currently paying around 5% risk-free. This is your “dry powder.” It keeps your capital safe and liquid, allowing you to sleep at night while the world argues. The verdict? Stay diversified, embrace the boring, and turn off the news. — Lyle Solomon, Principal Attorney, Oak View Law Group

If you are worried a prolonged Iran war could affect your nest egg, I recommend focusing on securing retirement income and preserving short-term assets rather than chasing tactical bets like gold or sector ETFs.

Use a bucket approach to hold stable, low-volatility assets to cover several years of withdrawals while keeping a growth allocation for longer-term needs. Shift the portion of your portfolio needed soon toward preservation and lower volatility investments as you enter retirement.

Strengthen diversified income sources such as Social Security, pensions, and annuity income to reduce sequence-of-return risk. Pay attention to asset location so taxable, tax-deferred, and tax-free accounts are positioned to minimize taxes when you withdraw.

Finally, adopt a flexible withdrawal plan with guardrails so spending can be adjusted if markets or geopolitics worsen, instead of making a major permanent allocation shift based on one event. — Clint Haynes, Financial Planner, NextGen Wealth

Put Capital Preservation over Aggressive Growth

For retirement-age investors, the current conflict in Iran highlights the importance of capital preservation over aggressive growth. A prudent approach involves making modest, 5-20% tactical shifts into defensive assets like gold and short-term Treasuries, which provide a necessary hedge against geopolitical spikes and energy-driven inflation.

By prioritizing liquidity and stability now, retirees can cushion their nest eggs against immediate market shocks without abandoning their long-term recovery potential.

On the equity side, focusing on “all-weather” sectors like Utilities, Healthcare, and Consumer Staples offers a way to maintain steady dividend income even during broader market downturns. While small, satellite positions in energy or defense ETFs can offset rising oil prices, the key is to avoid emotional overreactions to the headlines. Maintaining a diversified, high-quality portfolio ensures that your capital remains protected while you stay positioned to benefit when markets eventually normalize. — James Sahagian, Certified Financial Planner, Ramapo Wealth Advisors

Seek Robust diversification across asset classes and sectors

For retirement-age clients worried that a prolonged geopolitical conflict like the Iran war might impact their nest eggs, a defensive posture typically emphasises diversification and capital preservation over aggressive growth. One core idea is to balance a portfolio so that it can withstand volatility without forcing major asset reallocations in response to headlines. Robust diversification across asset classes and sectors remains a foundational strategy for resilience during geopolitical stress.

1. Safe-haven assets

Many investors look to traditional safe havens such as gold or gold-linked ETFs (e.g., IAU or GLD) because gold has historically served as a store of value and tends to have low correlation with equities during times of uncertainty. Allocating a modest percentage of a portfolio to gold or precious metals can act as an insurance policy against market drawdowns and inflationary pressures that often accompany geopolitical risk.

2. Fixed-income and cash equivalents

Holding high-quality bonds, short-duration Treasuries, or cash/money-market funds can preserve capital and provide liquidity, which is especially important for retirees who may need to draw income over time without selling equities at depressed prices. Treasury securities, particularly short-term ones, can serve as defensive assets when stock markets are volatile.

3. Defensive sectors and ETFs

Allocations to utility, consumer staples, and healthcare sectors — typically included in defensive ETFs — can provide relative stability because these industries supply essential goods and services regardless of economic cycles. These stocks often exhibit lower volatility than growth or cyclical sectors during stress periods.

4. Core & satellite approach

Rather than making a sweeping shift, many advisers recommend a “core-and-satellite” strategy where the core of a retirement portfolio remains broadly diversified in quality equities and bonds for long-term growth, while the satellite portion can include tactical defensive positions like precious metals or short-term fixed income to manage near-term risk. This allows retirees to maintain growth potential while tempering volatility. — Daria Turanska, Legal Manager, FasterDraft

Move from Sector Rotation to Structural Resilience

My perspective: Moving from Sector Rotation to Structural Resilience

From an institutional research perspective, navigating protracted geopolitical conflicts requires a fundamental shift in how we define a “defensive” strategy. For high-net-worth investors managing retirement portfolios exceeding $500,000, simply rotating out of tech and into utility ETFs or defensive equities often leaves the portfolio exposed to broader, systemic market shocks tied to global supply chain disruptions.

The Institutional Approach:

When analyzing how large-scale custody accounts prepare for sustained geopolitical volatility, the focus shifts from standard paper asset allocation to structural preservation: specifically, integrating non-correlated, tangible liquidity.

Historical data from protracted conflicts indicates that institutional capital heavily prioritizes sovereign wealth strategies, primarily through IRS-compliant physical precious metals. In a self-directed IRA or 401(k) rollover, physical gold doesn’t just act as a hedge; it serves as a structural firewall. It operates outside the traditional banking system and is immune to the counterparty risks that affect even the most “defensive” equities during wartime.

Rather than trying to time the market with sector-specific ETFs, our research framework suggests that true defensive posturing requires verifying liquidity and securing a baseline allocation in physical, universally recognized assets governed by transparent custodial fee structures. — Steve Maitland, Founder & Independent Research Analyst, Maitland Wealth

Flexible Deferred Annuities for Defensive Income Building

For retirement-age clients worried that a prolonged Iran conflict could harm their nest eggs, I suggest considering a Flexible Deferred Annuity as a defensive, income-building option. Many financial institutions offer variations with a chosen performance cap rate and segment buffers, plus timelines tied to segment types such as the S&P or Russell 2000 with defined ceiling and floor features.

Those elements can minimize the percentage risk for a loss in down years while limiting upside in stronger years, which can help stabilize near-term retirement income. This approach is not right for every investor, so review it with your financial advisor to see if it fits your timeline and income needs. — Ashley Kenny, Co-Founder, Heirloom Video Books

Reduce volatile individual Growth Names but maintain Diversified Index Funds

For older retirement-age clients who are concerned about over-extended geopolitical conflict, I propose a more cautiously defensive posture than drastic portfolio changes.

Allocate 5-10% to precious metals ETFs like GLD or IAU as hedge, and increase exposure on defensive sectors via utility ETF (XLU) which usually provide stable dividends during volatile periods. Consumer staples and healthcare exchange-traded funds (ETFs) can also provide stability as those sectors are needed no matter what wars are going on in the world.

Instead of drastic asset allocation changes that jolt long-term retirement strategies, slowly pare off holdings in more volatile growth names while keeping a kernel investment in diversified index funds: this way, you protect your retirement timeline and give yourself some wiggle room from a market that is near term-fuzzy at best. — Scott Brown, Founder, MintWit Continue Reading…

The column originated from a mid-January Vanguard Canada briefing with two of its economists held for the Canadian media in downtown Toronto. You can find at least two news stories on the web filed shortly after the event by Bloomberg Newsand Investment Executive.

While the general thrust of the press conference was on the opportunities for Canada in A.I. and materials stocks (chiefly gold and silver miners), the Q&A allowed me to probe Vanguard about something that has intrigued me for the past year: As a semi-retired investor who recently started a RRIF, I regard one particular Vanguard ETF as a big part of my core portfolio, along with low-volatility ETFs from BMO ETFs, and income-oriented ETFs from vendors you may see in blogs on this site.

After the Liberation Day craziness of April 2025, I became more defensive, though my Asset Allocation is not (yet) to the point the Rule of Thumb that your age should equal your Fixed Income: that would suggest in my case I should have 28% in Equities and 72% Fixed Income.

One core fund for retirees is VRIF, the Vanguard Retirement Income Fund, which is one of several funds often mentioned by the Retirement Club (see this introductory blog on the Club co-founded by blogger Dale Roberts of . ) It trades on the TSX under the ticker symbol VRIF.

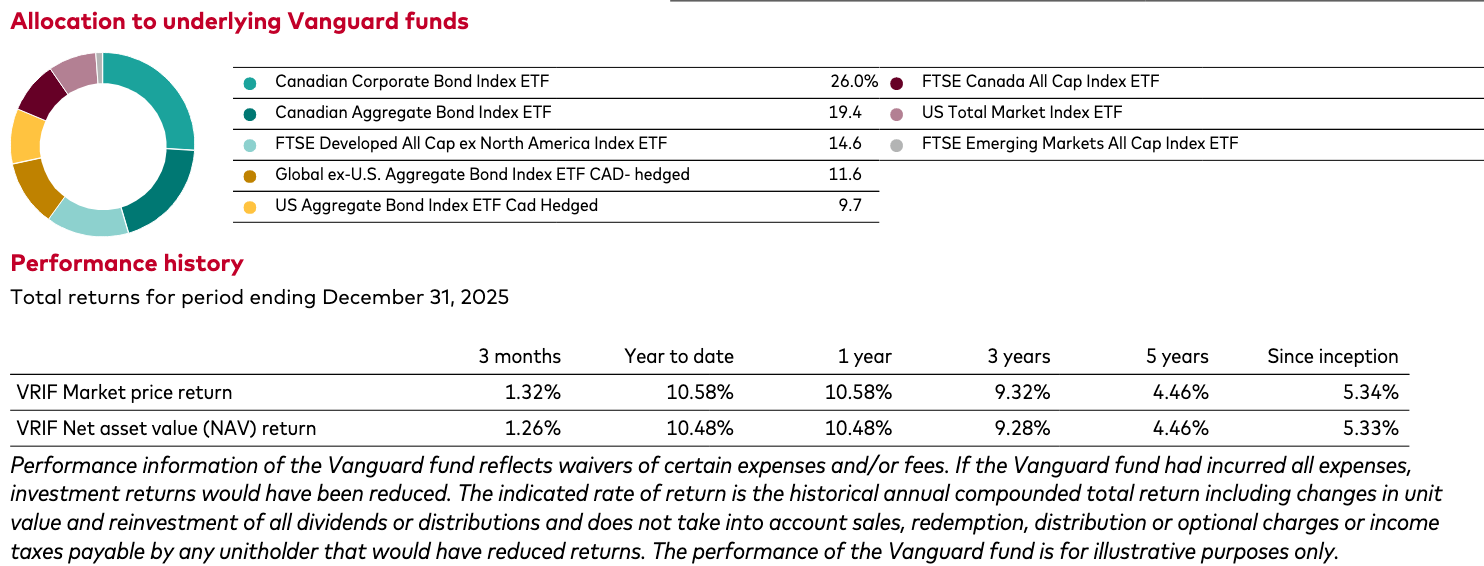

The screenshot below from Vanguard’s brochure shows VRIF’s holdings of Vanguard ETFs and performance to the end of 2025.

I first started a position in VRIF soon after its launch in 2020. At the time, its Asset Allocation seemed to be around 50% stocks to 50% bonds, spread around all geographies in the normal proportions.

However, as 2025 proceeded I noticed that VRIF had begun steadily to cut back on its equity exposure and raise its Fixed Income, almost to the point of 30/70. I’ve also noticed various YouTube videos from Vanguard’s U.S. parent that suggest similar caution: a cutting back from the big US growth mega cap stocks and a move more to other developed and emerging economies around the world.

If you read the VRIF launch news release, it emphasizes the objective is to provide income-seeking investors with a “targeted 4% annual payout.” That happens to be in line with William Bengen’s famous 4% Rule, which is “fine with me,” as I quipped at the media briefing.

In response to my query, Vanguard Canada spokesman Matthew Gierasimczuk said VRIF’s asset allocation varies over time” but the goal is the targeted 4% Return: Vanguard sees a “more optimistic outlook on bonds and Fixed Income: better to lock in without risk of equities.”

Kevin Khang, Vanguard

Then Kevin Khang, Vanguard’s head of global economic research [pictured left] reiterated that the ETF seeks to fund a “certain level of payout: bonds in our view can achieve the desired certain level of payout” and “the US stock market is pretty expensive for obvious reasons: the US is reasonably valued and bonds are very normally valued; which is a new thing.” From 2009 to 2022, since the Great Financial Crisis, bonds in general didn’t pay much, which upset people in 2022-223 when rates went up but now they are reasonably valued: relative to inflation they are paying a decent Real Return.”

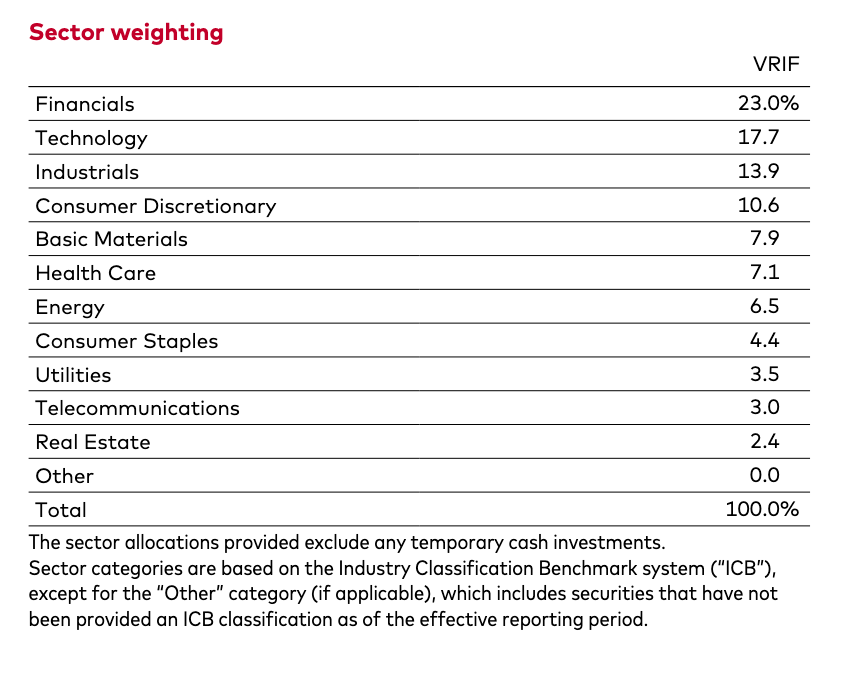

Here’s the sector weightings for VRIF at the end of 2025:

Vanguard rates its volatility as “low.” Notice the weightings of certain sectors often overweighted in pure low-volatility ETFs (like those from BMO and Harvest): Health Care, Consumer Staples and Utilities. As you can see above, the weightings in more volatile sectors like Technology and Financials is much higher.

For the MoneySense column I was subsequently referred to Head of Product for Vanguard Canada, Aime Bwakira. The rationale for VRIF’s high fixed-income exposure appears to be one of not taking more risk than you need to take, a stance which is apt for the retirees VRIF caters to. Bwakira confirmed Vanguard “has been leaning more heavily toward bonds — particularly higher quality and corporate bonds — than in past years while staying within its equity guardrails” of a minimum 30% and maximum 60%. This positioning “reflects the current environment and the results of our capital markets projections.”

3 reasons Vanguard is boosting Fixed Income in VRIF

The rationale is three-fold:

First is higher interest rates. Bonds — especially corporate bonds — are paying more than they did for many years post the 20008 Great Financial Crisis (GFC): “This makes them well‑suited to support VRIF’s 4% income target without taking on unnecessary stock-market risk. VRIF includes corporate bond exposure specifically to help enhance yield for investors.

Second, given today’s market outlook, the fund’s model has shifted toward fixed income because bonds “currently provide a more favourable balance of expected return and risk.” I was also referred to Vanguard’s current VCMM 10-year projections (VCMM = Vanguard Capital Markets Model) for various asset classes. It’s also published in the US for US investors Vanguard Capital Markets Model® forecasts | Vanguard.

Dated January 22, 2026, the document states that “Even at current stretched valuations, rising earnings growth could provide momentum for stocks in the near term. However, our conviction is growing stronger that long-term prospects for U.S. equities are subdued. Our model anticipates annualized returns of about 3.9% to 5.9% over the next 10 years.” It adds that “Our muted long-term return projection for U.S. equities is entirely consistent with our more bullish prospects for an AI-led U.S. economic boom.”

The third and most important point raised by Bwakira is that “a higher allocation to bonds helps VRIF deliver reliable cash flows, which is central to its mandate. Because income needs don’t disappear during market volatility, VRIF prioritizes stability and sustainability in its payout. VRIF aims to maintain the value of an investor’s initial investment over the long term. Tilting toward bonds during periods of elevated equity market uncertainty helps protect investors from large drawdowns while still supporting the payout.”

VRIF is one popular source of Retiree income at the new Retirement Club

This common-sense caution has not gone unnoticed by Canadian retirees seeking stable income. VRIF is a well-regarded ETF members of the Retirement Club, founded by Cutthecrapinvesting blogger Dale Roberts and partner Brent Schmidt. One of the club’s monthly Zoom presentations in the autumn of 2025 highlighted VRIF among several other income sources for retirees. Roberts has long championed VRIF, as in this blog on his site originally written after the launch, and subsequently updated: most recently in this version. Continue Reading…

Market volatility and shifting economic signals are forcing retirement savers to rethink their portfolios in real time. This article gathers practical strategies from five seasoned financial leaders who manage billions in retirement assets and are actively adjusting allocations right now. Their approaches range from bucketing time horizons to integrating global hedges, offering concrete tactics that advisors and individuals can apply immediately.

These experts were gathered by Featured.com, which has been supplying Findependence Hub with quality content for several years. It has changed its procedure so editors like myself can request input on particular topics we think will interest our readership. The sources are all on LinkedIn, as you can see by clicking on their profiles below.

Secure Core Needs via Indexed Annuities

Segment Time Buckets to Tame Sequence Risk

Shift Toward Global Breadth and Tangible Hedges

Favor Quality Income Plus Balanced Discipline

Blend Abroad Exposure for Safety Anchors

Secure Core Needs via Indexed Annuities

Given the trade and tariff noise, I start by securing essential lifestyle costs with Fixed Indexed Annuities that provide floors with index-linked upside to blunt sequence-of-returns risk.

I also require clients to keep separate emergency reserves and a growth sleeve because FIAs have surrender periods. We coordinate annuity design, laddering, and rider choices with Roth conversions and RMD planning to create a predictable income base before taking market risk.

Looking ahead to the rest of 2026, portfolio concerns for individuals aged 65 and over, and those close to retirement (within 10 years), include risk management, purchasing power protection, and geopolitical and currency diversifications.

We are seeing a move away from traditional 60/40 or 70/30 portfolios and toward a more dynamic framework for asset allocation. U.S. stocks and high-grade Fixed Income are still foundational, but we are trying to avoid over-allocation to a particular market or macro scenario.

Some key themes for the future are greater geographic diversification, selective access into non-U.S. assets, and cautious hedging versus U.S. dollar declines. We are not making stark currency predictions, but geographical diversification outside of USD-focused assets is becoming sensible for increasing numbers of investors.

At the same time, there’s also been a reinforcement of allocations to hard assets like precious commodities and metals. The inclusion of crypto exposures is small and is based on suitability.

As such, it’s emphasized that there’s a focus on “resilience and adaptability, and positioning to withstand trade tensions, volatility in inflation, and policy uncertainties in a way that is independent of specific narratives.”

For investors in or approaching retirement, the balance of 2026 should be geared towards capital preservation, income stability, and inflation resilience as the primary objectives: while still maintaining enough growth exposure to support long retirement horizons.

Retirees cannot afford to eliminate equities, especially with longer life expectancies and ongoing inflation risk. But favor high-quality cash-generating companies over speculative, momentum-driven stocks. Bonds should primarily reduce volatility and fund near-term spending. Real assets, alternatives can support diversification while improving returns, and investors could have a small exposure to this segment.

For retirees and near-retirees in 2026, the goal is not to time markets, but to construct a portfolio that:

Can withstand equity volatility

Generates dependable income

Preserves purchasing power over a multi-decade retirement

Asset allocation should be personalized, tied to spending needs, risk tolerance, and other income sources — but the overarching theme is balance, quality, and discipline. Not aggressive risk-taking or excessive conservatism.

For my pre-retiree clients, one of the biggest risk factors to a successful retirement is Sequence-of-Return risk, or the risk of experiencing poor market conditions at the start of retirement.

To help address this risk, I believe in holding a diversified portfolio that consists of several accounts that have different asset allocations and amounts. For example, funds needed in the first year of retirement would be allocated more conservatively than funds needed in the 15th year of retirement. This helps to reduce the impact of geopolitical risk or currency risk on their portfolio and thus their retirement. Additionally, having a portfolio that includes commodities like gold or international equities helps to balance the risk of a particular underperforming asset class throughout retirement as well.

For retirees and those within ten years of retirement, the ongoing tariff tensions and global trade uncertainties require a careful reassessment of asset allocation while maintaining a focus on capital preservation and income reliability. Traditional allocations, such as the 60/40 or 70/30 equity-to-bond mixes, still provide a strong foundation, but we are increasingly emphasizing diversification across geographies and asset types to manage both market and currency risks.

For U.S.-based investors approaching retirement, a modest increase in non-U.S. equities makes sense to capture growth opportunities abroad while reducing concentration risk in domestic markets that may be more exposed to trade disruptions.

We are also monitoring the U.S. dollar closely, and while we are not making aggressive currency bets, selective exposure to assets that historically hedge dollar weakness — such as precious metals and certain commodities — can provide a measure of protection and portfolio resilience.

We continue to stress bonds and cash equivalents for retirees, particularly high-quality, short- to intermediate-duration bonds that preserve capital while providing reliable income. However, in light of persistent inflation pressures and potential geopolitical shocks, we are selectively introducing alternatives, such as commodities, real assets, and limited exposure to crypto in small, highly managed positions: not as core holdings but as strategic diversifiers. The goal is not chasing yield or speculative gains, but rather enhancing portfolio resilience and smoothing volatility.

Overall, the guiding principle remains risk-adjusted diversification: maintaining sufficient equity exposure for growth, bonds for income and stability, and alternatives to hedge against systemic risks, while keeping allocations flexible and aligned with liquidity needs. Retirees should avoid over-concentration in any single market or asset type and prioritize investments that protect purchasing power, provide consistent income, and withstand trade or currency shocks over the remainder of 2026.

The focus of the column is on the Purpose Longevity Pension Fund (LPF), which I recently initiated a small position in my personal RRIF.

It also touches on tontine products like Guardian Capital’s GuardPath Funds, as well as several longevity-oriented investment income funds recommended by some U.S. advisors and retirement experts. However, Guardian closed its GuardPath Funds a year ago and are effectively no longer a tontine pioneer.

That leaves LPF as the lead Longevity Fund pioneer in the Canadian market and to some extent the world. Fraser Stark, Global Business Leader for Toronto-based Purpose Investments Inc., says LPF has accumulated about $18 million since its launch almost five years ago, with roughly 500 investors in either the Accumulation or Decumulation classes.

As the MoneySense column summarizes, Purpose doesn’t use the precise term tontine to describe LPF but it does more or less aim to do what traditional Defined Benefit pensions do: in effect those who die earlier than expected end up subsidizing the lucky few who live longer than expected. LPF deals with the dreaded Inflation by gradually raising distribution levels over time. It recently announced it was boosting LPF distributions by 3% for most age cohorts in 2026.

Two classes of Purpose Longevity Pension Fund

Fraser Stark, courtesy Purpose Investments

Age is a big variable here. Purpose created two classes of the Fund: an “Accumulation” class for those under age 65, and a “Decumulation” class for those 65 or older. The latter promises monthly payments for life; at the same time the structure is flexible enough to allow for either redemptions or additional investments in the product; something that traditional life annuities do not usually provide. When moving from the Accumulation to the Decumulation product at age 65, the rollover is free of capital gains tax consequences.

The brochure describes six age cohorts, 1945 to 1947, 1948 to 1950 etc., ending in 1960. Yield for the oldest cohort as of September 2025 is listed as 8.81%, falling to 5.81% for the 1960 cohort. My own cohort of 1951-1953 has a yield of 7.24%.

How is this all achieved? Apart from the mortality credits, the capital is invested much like any broadly diversified Asset Allocation fund. As of Sept. 30, Purpose lists 38.65% in Fixed Income, 43.86% in Equities, 12.09% in Alternatives, and 4.59% in Cash or equivalents. Geographic breakdown is 54.27% Canada, 30.31% the United States, 10.84% International/Emerging and the same 4.59% in cash. MER for the Class F fund (which most of its investors are in) is 0.60%.

Canadian advisors supporting LPF

What do Canada’s financial advisors think about LPF in particular? John De Goey of Toronto-based Designed Securities has clients in it. Soon after its launch, he said he was a big supporter of the Purpose product … I think it is innovative and overdue. Accepting the usual disclaimer that everyone’s circumstances are unique and you should consult a qualified professional before buying, I was delighted when it was launched because longevity risk was one of the last ‘unsolved challenges’ of financial planning.” De Goey says Canadians “severely underestimate” how long they’re going to live. As for LPF, he says “Risk pooling in three-year cohort groups / pools is a big innovation and is only possible in a mutual fund structure.” Continue Reading…