Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

Hard to believe but Findependence Hub just turned 10 years old. We launched Financial Independence Hub on Nov. 03, 2014. Here is the very first post.

You’ll note that for a long time, we self-referred with the short-hand “The Hub.” This was of course long before another site was launched a few years back also called The Hub. So we try NOT to refer to ourselves using that short form, as it may be confusing.

However, the slogan still applies: North America’s Gateway to Financial Independence. That’s because both our readers and content providers are in Canada and the United States. Given the population differences, though, we are disproportionately Canadian.

From the start, the aim was to publish at least four blogs a week, and often five. In fact, as of this writing, we had published 2,931 blogs: just shy of 3,000. That’s roughly 300 blogs a year.

As we explained a few weeks ago, generally we don’t schedule Wednesday blogs far in advance, in order to leave that slot open for any late-breaking developments. It also allows us to shuffle the schedule when necessary.

The future

So what of the future? Well, my personal financial life is more or less an open book, between what I write here and what I write every month in my Retired Money column at MoneySense.ca.

As I disclosed earlier this year, I am now 71 and therefore enter the magic land of RRIFs as of the end of this year and into January 2025. At some point, I may retrench blog frequency down to three blogs a week instead of four or five: aiming for Monday/Wednesday/Friday. Happy to hear reader and sponsor feedback on that though. I’m also open to partnering suggestions.

Certainly I would like to thank the registered users who have hung in this far, as well as our advertisers who make it possible to provide this content at no charge to readers. Continue Reading…

My latest MoneySense Retired Money column looks in-depth at a new “Decumulation” offering from Sun Life, unveiled late in September. You can find the full column by clicking on the highlighted headline: What is Sun Life’s new decumulation product?

As you can see from image below taken from MyRetirement Income’s website, the emphasis is on providing regular income to last to whatever age a retiree specifies. That income is not, however, guranteed as a life annuity would be.

The Globe & Mail’s Rob Carrick first wrote about this shortly after the Sun announcement. My column adds the opinions of such varied Canadian retirement experts as author and finance professor Moshe Milevsky, retired actuary Malcolm Hamilton, Caring for Clients’ Rona Birenbaum and Trident Financial’s Matthew Audrey, as well as Sun Life Senior Vice President, Group Retirement Services, Eric Monteiro.

Some of the more cynical takes are that this is a way for Sun Life to continue to profit from client financial assets gathered during the long accumulation phase, rather than seeing them migrate to other solutions, such as annuities provided by either one of its own life insurance arms or that of rivals.

Aiming for Simplicity and Flexibility

As Sun’s Eric Monteiro told me in a telephone interview, the company’s preliminary research found that rival products that were first on the market (see full MoneySense column) were often perceived as complicated, and as a result uptake of some of these pioneering Decumulation products have been underwhelming. It sought to create a solution that was relatively simple and flexible.

In essence, it is not dissimilar to some Asset Allocation ETFs, such as Vanguard’s VRIF, which is 50% equities and 50% fixed income. But Sun’s product may and probably will have different proportions of the major asset classes. In fact, it lists 16 external global money managers who deploy up to 15 different asset classes, which include Emerging Market Debt, Liquid Real Assets, Direct Infrastructure, Liquid Alternatives and Direct Real Estate. Managers include BlackRock Asset Management, Lazard Asset Management, Phillips, Hager & North, RBC Global Asset Management and its own Sun Life Capital Management. Continue Reading…

Many Canadians are watching closely as their neighbour to the south prepares to hold a crucial Presidential election in November 2024.

Meanwhile, Canada’s federal election is still more than one year away. Canada continues to contend with economic, social, and political issues that are faced in varying degrees by its partners in the G7. These issues include managing immigration, aging populations, and housing affordability. Its central bank also seeks to strike a balance in monetary policy after raising interest rates to combat inflation.

In this piece, we’ll look at how the Canadian economy has fared over the past year. Moreover, we will look at an exchange-traded fund (ETF) that offers exposure to Canada’s great companies. Let’s jump in.

Where does Canada stand in the fall of 2024?

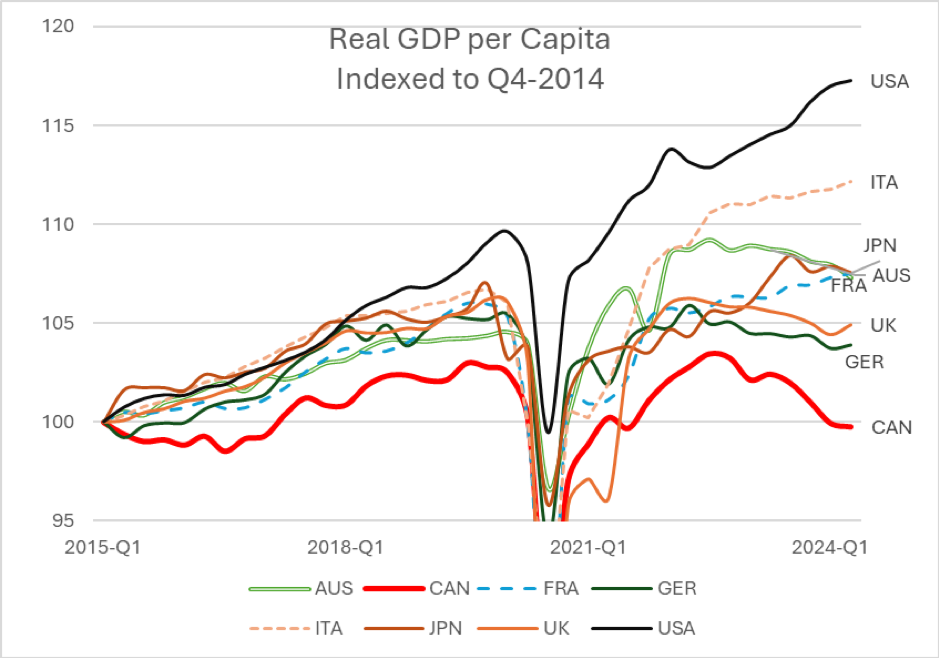

From an economic standpoint, Canada finds itself in a difficult predicament. The OECD chart below illustrates that Canada has fallen behind many of its peers in the post-COVID-19 pandemic era.

Source: Organization of Economic Cooperation and Development (OECD), 2024 Household Dashboard, accessed October 6, 2024.

Canada’s Real GDP per capita ranking compared to its peers, especially stand outs like the United States and Italy, has been abysmal. This is coupled with dismal employment statistics that have shown rising unemployment. Even positive jobs data is skewed by government hiring in some cases.

Indeed, unemployment in Canada has climbed from a low of 5% in 2022 to 6.5% in its latest reading. Royal Bank of Canada Deputy Chief Economist Nathan Janzen recently stated that unemployment would continue to rise to 7% by early 2025. That is nearly a percentage point higher than pre-pandemic levels.

The Bank of Canada (BoC) is in a tough spot as it battles a weak economic environment and a housing supply shortage that has kept prices elevated. Now, the BoC finds itself in a position where it will need to employ further interest rate cuts. However, in doing so, it runs the risk of re-inflating the housing price bubble.

Why should you trust Canadian companies?

Canada has been in a rut economically in recent years. However, the forward price-to-earnings ratio difference between the S&P TSX 60 and the S&P 500 show that publicly traded Canadian companies still offer attractive value at this stage. Continue Reading…

To Hedge FX Risk, or Not to Hedge: Currency markets are notoriously difficult to call but can meaningfully impact portfolio returns. ETF Strategist Bipan Rai provides a detailed framework for investing outside the Canadian market.

Image Getty Images courtesy BMO ETFs

By Bipan Rai, BMO Global Asset Management

(Sponsor Blog)

Admittedly, using a spin on a famous Shakespeare quote to start a note on currency hedging1 is verging on trite. Nevertheless, if Hamlet were running a portfolio of overseas assets, his primary concern would have to be the “slings and arrows” of currency markets — which are notoriously difficult to call but can meaningfully impact portfolio returns.

For Canadian investors, looking abroad provides several benefits. The most important is diversification, whether it’s through access to other regions that are less correlated with Canadian markets or to other products that aren’t available domestically.

However, investing abroad also means taking on foreign exchange risk given that international assets are priced in currencies other than the Canadian dollar (CAD).

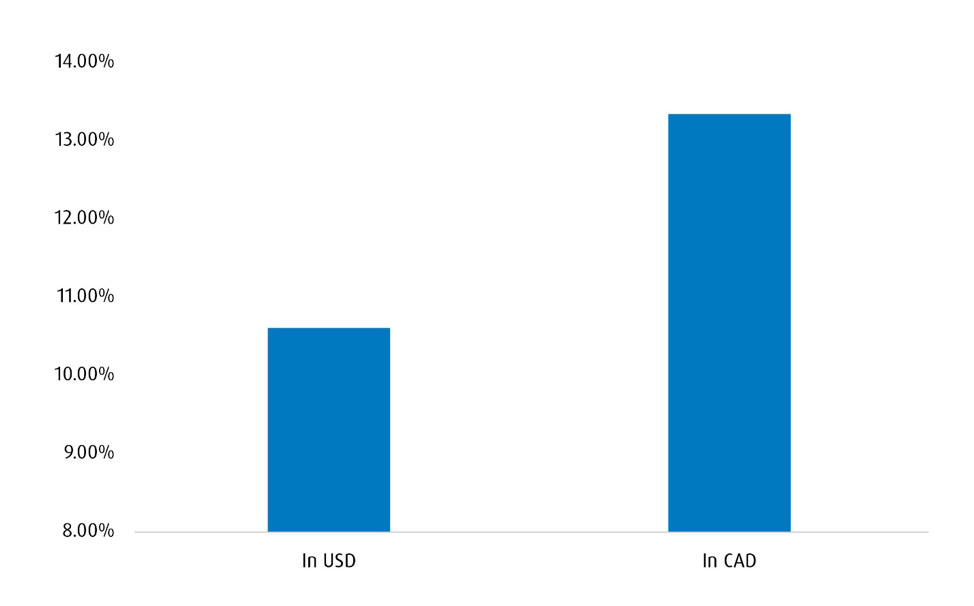

For illustrative purposes, consider Chart 1, which shows the total return for the S&P 500 in U.S. dollars (USD) and in CAD terms for Q1 of this year. In USD terms, the index was up 10.6% over that time frame, but since that period also corresponded to weakness in the CAD relative to the USD (or USD/CAD moved higher) the index outperformed in CAD terms (up 13.3%). That means that Canadian investors would have fared much better leaving their USD exposure unhedged ex ante.

Chart 1 – S&P 500 Total Return for Q1 2024

Source: BMO Global Asset Management

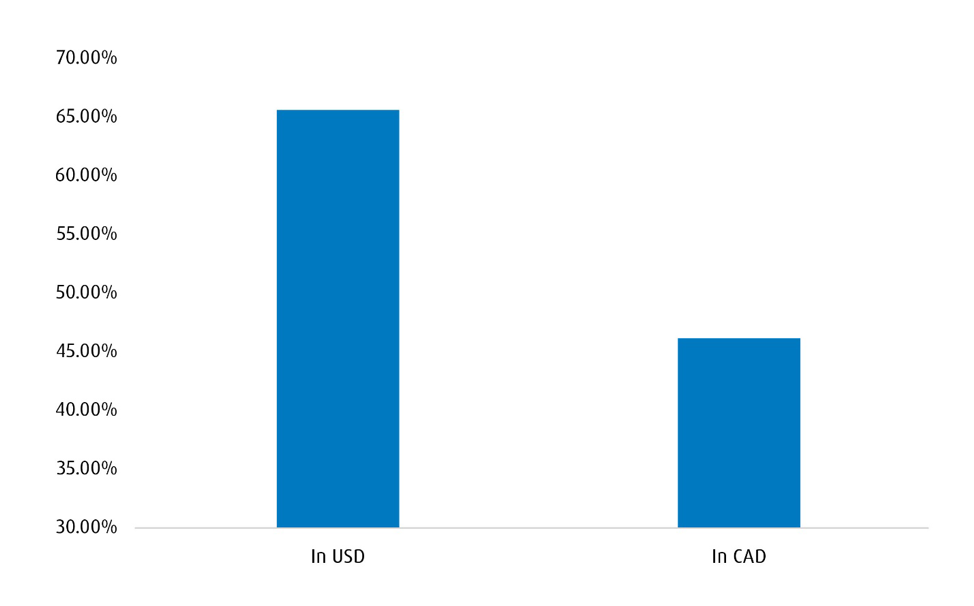

Now let’s look at an alternative period in which the CAD strengthened against the USD. Chart 2 shows a comparison of the total return for the S&P 500 from April 2020 to April 2021 (in which USD/CAD was lower by over 11%). During that period, the total return index outperformed in USD terms by close to 20%. In this scenario, an investor who had hedged their FX risk would have been in the optimal position.

Chart 2 – S&P 500 Total Return Between April 2020 – April 2021

Source: BMO Global Asset Management

As these examples show, currency risk is a key consideration for any investor who wants to look beyond Canada for diversification. That risk can cut both ways, which amplifies the importance of hedging decisions. In our minds, the decision to hedge foreign exchange (FX )risk (including the degree to which foreign exposure is hedged) comes down to the following:

An investor’s view of the underlying currency pair

Whether the currency pair is positively or negatively correlated2 with the underlying asset

In this note, we’ll make a brief comment on the first point but focus largely on the second one. as we feel that should be given more weight for hedging decisions.

FX Markets are Tough to Call

Taking a view on the underlying currency pair is easy to do — but difficult to capitalize on.

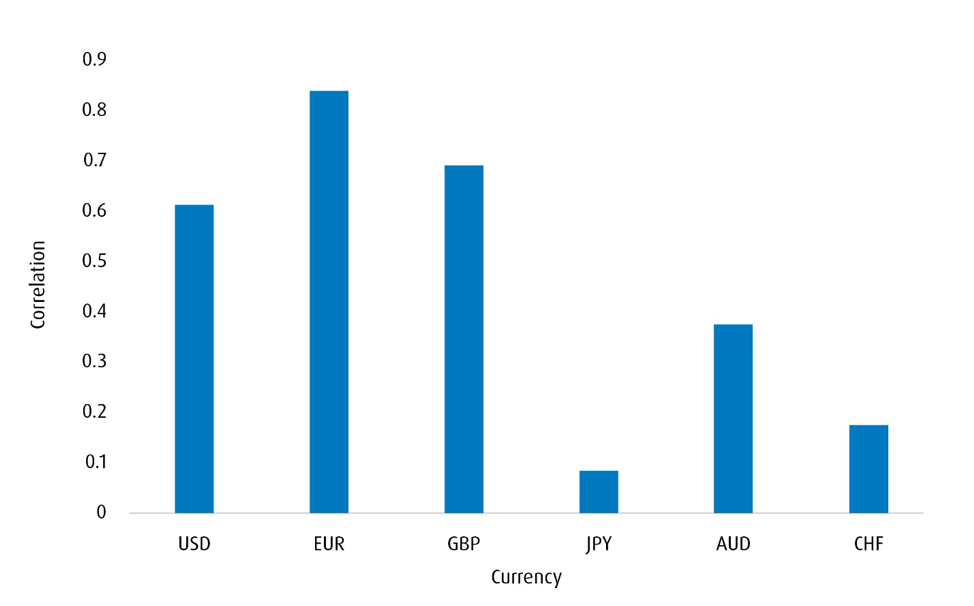

Indeed, foreign exchange markets are notoriously fickle. One reason why is the relationship between predictive factors and currency pairs is rarely stationary. For instance, a lot of market participants tend to use front-end (2-year) yield spreads as a proxy for central bank divergence in the spot FX market. Chart 3 shows the current correlation between those spreads and the different CAD crosses, and as expected, the relationship isn’t consistent from a cross-sectional perspective.

Chart 3 – Correlation Between Two-Year Spreads and the CAD Crosses

* * Correlation window is 2 years. The CAD is used as a base currency for this analysis. The spread is tabulated by subtracting the foreign 2-year yield from the CAD 2-year yield. Source: Bloomberg, BMO Global Asset Management.

We can also see this by looking closer at the relationship between a factor and a currency pair over time. Chart 4 shows the rolling 100-day correlation between USD/CAD and the price of oil (proxied by the prompt WTI contract3) going back ten years. Note how frequently the strength of the correlation (as well as the sign) changes over time. Continue Reading…

Top investment executives told a webinar held Wednesday morning that investors should not mix Politics and Investing. Even so, while market observers at Franklin Templeton view the upcoming U.S. election as essentially a “toss-up” they seem to believe that a victory or sweep by the Republicans’ Donald Trump would be more positive for stocks than a Kamala Harris win.

Grant Bowers, portfolio manager and Senior Vice President for Franklin Equity Group, said “it’s a 50/50 tossup for the presidential winner. Both candidates are well known so it’s not surprising” there’s been little market volatility in the runup to the November 5th election. Generally, he’s bullish no matter the outcome. The economy did well in Trump’s first term while a Harris victory would be a continuation of Biden policies. The real differences are on tariffs, fiscal policy and regulation. “The most likely outcome is a split government” but there would be more volatility if there is a sweep by either party.

Of course, it’s quite possible that investors won’t know the official outcome for several weeks. If the process of counting votes drags on and there are legal challenges like there were in 2020, investors can expect more protracted volatility.

Sonai Desai, Chief Investment Officer for Franklin Templeton Fixed Income said the U.S. economy is set to do “quite well. I agree there’s a reduced probability of Recession: that’s not our baseline for a while.” If there’s a Republican sweep and broader tariffs measures introduced by Trump, “that might limit the Fed’s appetite for massive rate cuts.” Her baseline is that even with a Republican sweep, there won’t be a literal imposition of tariffs: that didn’t happen in 2016, so “I don’t think we will get the full range of cross-the-board tariffs.” Either way, the mighty U.S. consumer will “continue to consume and I don’t see that changing with the Election.”

Clearbridge’s Jeffrey Schulze

In the very long run, of course, any short-term market volatility from elections is likely to be a blip, which is why Franklin Templeton tells clients not to mix investing and politics.

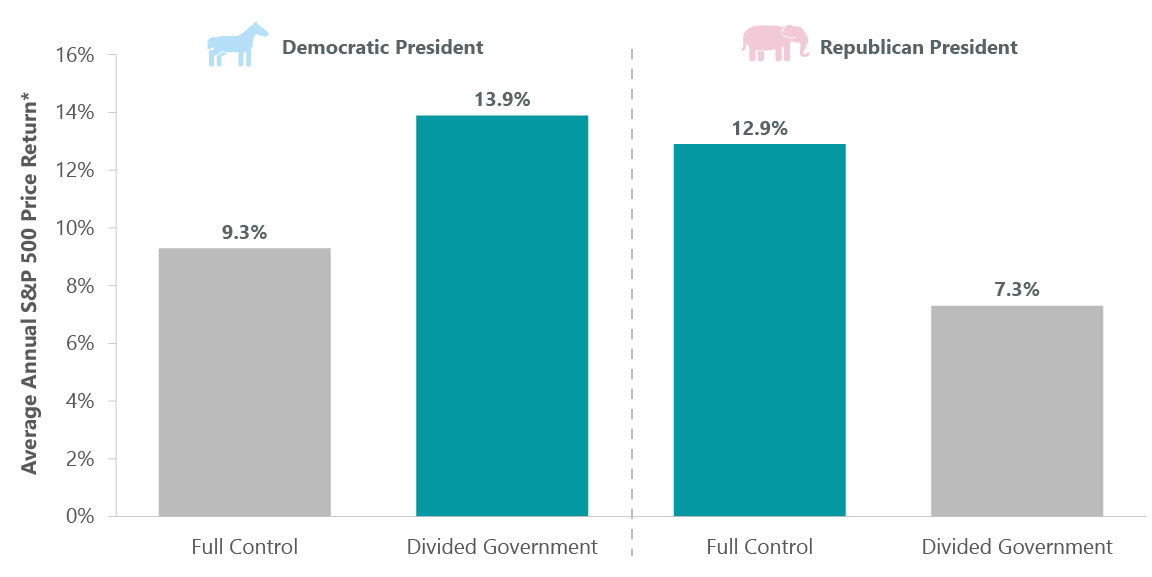

In an analysis released early in October, Clearbridge Investments Head of Economic and Market Strategy Jeffrey Schulze, CFA, showed the following annual returns for the S&P500, all positive for equities no matter which party wins and whether or not they get full control or are in a divided government. Based on that, the best outcomes for investors would be a Democratic president with a Divided Government or Full Control by a Republican president.

“We view a Trump win, likely coming in a sweep scenario, as net positive for equities as it preserves favorable corporate tax treatment and builds on tax elements that expired,” Schulze wrote in the October 1st update, “A Harris win, likely coming with a divided Congress, would be mildly negative due to fewer provisions of expiring tax legislation getting extended due to political gridlock.”

Trump win likely positive for Stocks

“In aggregate, we view a second Trump presidency under a sweep scenario as net positive for equities. The expectation is for a more favorable corporate tax regime and less of a regulatory burden, both of which should boost corporate profits. Conversely, there is the potential for increased tariffs and retaliation from U.S. trade partners … We view U.S. stocks as best placed under Trump, with banks and capital markets, as well as the oil and gas complex, well positioned due to lighter regulation. Aerospace and defense is also likely going to benefit as well as biopharmaceuticals. Areas that could see pressure are restaurants and leisure, due to the less availability of labor, as well as EVs, autos and clean energy producers.”

Harris win might be “mildly negative” for Stocks

A Kamala Harris win would be less positive for U.S. stocks, Schulze writes: “We see a Harris win as mildly negative to equities should she preside over a divided Congress. It will be more of a headwind to the markets should we see a Democratic sweep as she will then be able to implement higher taxes on corporations and high-income individuals, as well as push a more ambitious regulatory agenda. However, tax credits for low-income individuals would provide an offset, creating an economic boost to this segment of the economy.Tighter regulation could weigh on biopharmaceuticals, banks, capital markets, energy as well as mega cap technology. But again, we caution against basing investment or portfolio positioning solely on the regulatory environment. Areas to be bullish about under Harris would be consumer discretionary, specifically restaurants & leisure, home building and building products.”

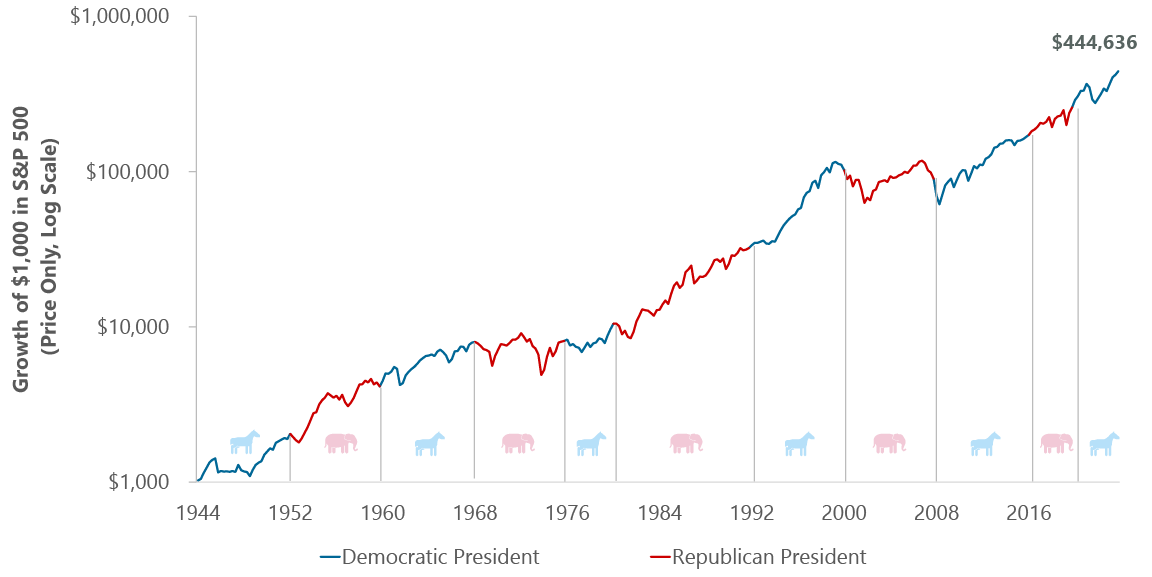

Generally, Franklin Templeton continues to advocate a “stay the course” stance for investors geared to the long term. The chart below shows that going back to 1944, the U.S. stock market has risen steadily over time regardless of which political party is in the White House.

Stephen Dover, chief market strategist and Head of Franklin Templeton Institute, acted as Moderator in Wednesday’s webinar, fielding audience questions. He also wrote a U.S. election update earlier this month, headlined “Uncertainty Reigns.”

He concluded back then that the election remains “too close to call. A divided government in Washington, DC, with no single party controlling the White House, Senate and House of Representatives is likely … Investors should gird themselves for uncertainty and potential bouts of volatility preceding and following election day. It is quite possible that the outcome for the presidency will not be settled until the December 17 certification deadline.”

Dover expects market uncertainty to continue well past November 5th, if not until January’s inauguration of the ultimate winner.”Legal challenges, some of which have already commenced, add to uncertainty. Re-counts, delays and disputes over certification of results, alongside courtroom litigation are virtually assured if state election outcomes are close. Various legal and procedural challenges are likely to endure until at least December 17, which is the deadline for state certification of the presidential election results and the official nomination of state electors to the Congressional certification on January 6, 2025.”

However, Dover says his basic investment conclusions remain unchanged. They are as follows: Continue Reading…