By Fritz Gilbert,

Special to the Financial Independence Hub

The market’s been a bit “wobbly” in the past few days, in case you haven’t noticed.

We shouldn’t be surprised, and we shouldn’t worry.

Today, I’ve chosen to talk about market volatility, and how we should think about volatility in terms of our overall retirement plans.

As I write these words, the S&P 500 was down another 2%, on top of a 3.3% decline yesterday.

Down 5% In Two Days. Yep, that’s volatility.

Here’s the 5-day chart:

Down … down … down.

But, it’s no big deal

Funny thing about markets, they’re volatile. As Ben Carlson wrote last Friday, the market has averaged a daily drop in excess of 3% three times per yearsince 1928. So, we should expect “Big Down Days” on a regular basis, even if we haven’t seen too many of them lately. One interesting note is that 80% of those “Big Down Days” occur during a market correction or bear market. Makes sense, but it can and does happen during Bull markets, as well.

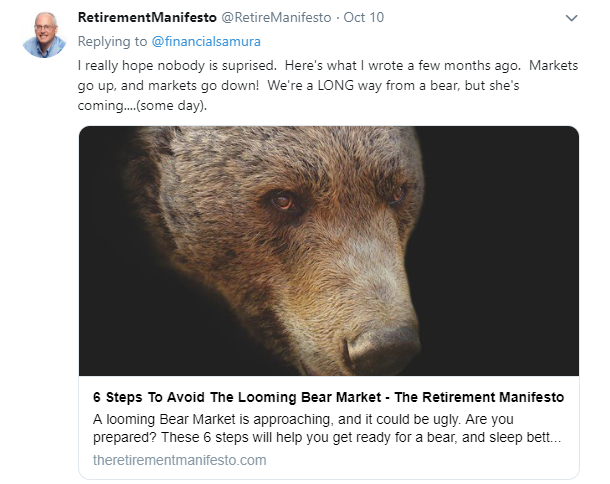

Here’s what I posted on Twitter after the Big Down Days last week:

I’ve no idea where things will go from here. In all honesty, I really don’t care. I know markets will go up, and markets will go down, and we’d be naive to assume otherwise as we plan for our retirement. I don’t check the market daily, and I don’t worry about daily volatility.

Let’s Be Real. The CAPE ratio continues at abnormal highs, which increases the likelihood of subpar performance over the coming years. I’m expecting it, and I’ve incorporated it into our retirement withdrawal strategy. As of October 16th, after two consecutive down days of 2%+ declines in the S&P 500, the CAPE ration remains at a level of 30.80, well above historical norms of 16.6, as shown below:

We’re being unrealistic if we expect the market to continue an uninterrupted upward trend, especially in light of today’s high valuations. Volatility is real, so make sure you incorporate it into your retirement plans.

One Day’s Decline = One Year Of Withdrawals

As I thought about the market’s move on October 10, I realized that the 3%+ move was equivalent to an entire year’s Safe Withdrawal Rate, and I sent the following Tweet:

Resilience In The Face of Market Volatility

Rather than worry about the volatility, Be Resilient. Think about volatility before you retire, and incorporate your strategy for volatility into your retirement planning.

As part of our retirement planning, we have to be realistic to the fact that markets will face volatility. They always have, and they always will. It’s the way the world turns, and we’re well advised to plan accordingly. It’s why I built my Bucket Strategy as my primary plan for Retirement Income, and it’s the reason I really don’t worry as the market ebbs and flows over any given day. In fact, I don’t even watch the market dynamics on a day-to-day basis.

On a long-term basis, it doesn’t really matter.

I don’t watch the market on a day-to-day basis. I know our Bucket Strategy will cover all but the worst Bear Market. Click To Tweet

Markets will be volatile.

It’s the nature of The Beast. Plan for it, and have sufficient funds to absorb a significant market downturn should it happen in the early years of your retirement.

Best to plan for the worst, and hope for the best.

Fritz Gilbert is the Founder of The Retirement Manifesto, a Plutus Award winning blog dedicated to helping people Achieve A Great Retirement. After 30+ years in Corporate America, most recently as a Commodity Trader, Fritz retired as planned in June 2018 at Age 55. He and his wife are looking forward to extended travel and “giving back” to their community through charitable work in retirement. This blog was published on his website on Oct. 16, 2018 and is republished here with his permission.

Fritz Gilbert is the Founder of The Retirement Manifesto, a Plutus Award winning blog dedicated to helping people Achieve A Great Retirement. After 30+ years in Corporate America, most recently as a Commodity Trader, Fritz retired as planned in June 2018 at Age 55. He and his wife are looking forward to extended travel and “giving back” to their community through charitable work in retirement. This blog was published on his website on Oct. 16, 2018 and is republished here with his permission.