By Mark Seed, myownadvisor

Special to Financial Independence Hub

Some time ago…yours truly wrote a controversial post about the intent to live off dividends and distributions from our portfolio.

Well, a great deal of time has passed on that post by my thinking and goals remain the same – as least in part for semi-retirement!

Read on to learn why my approach to live off dividends remains alive and well this year in this updated post.

Why my goal to live off dividends remains alive and well

First, let’s back up to the controversy and offer a list why some investors couldn’t care less about my approach and why dividends may not matter at all to some people:

- The trouble with any “live off the dividends” approach is that you’d need to save too much to generate your desired income. Fair.

- Dividends are not magical – there is nothing special about them. Sure.

- A dollar of dividends is = a one-dollar increase in the stock price. True, a dollar is a dollar.

- Stock picking (with dividend stocks) is fraught with under performance of the index long-term. I’m not convinced about that.

- You can never possibly know long-term how dividends may or may not be paid by any company. Fair.

In many respects these investors are not wrong.

You do need a bunch of capital to generate income.

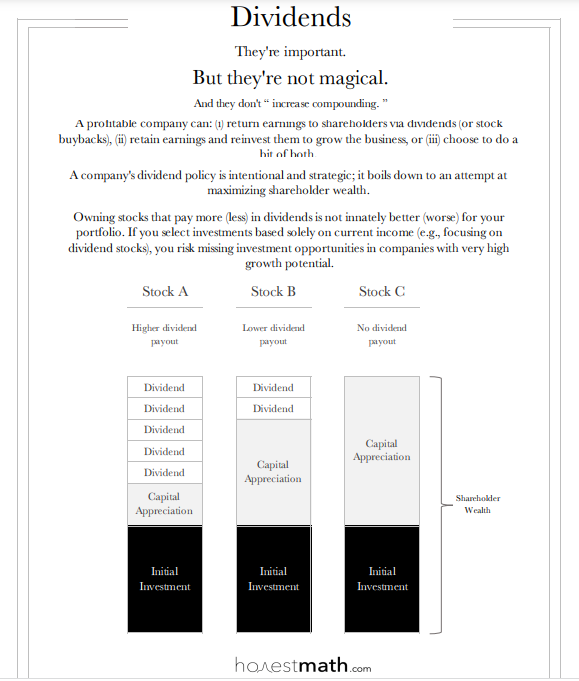

Dividends are part of total return. [See image at the top of this blog.]

Stock selection can open up opportunities for market under performance.

And the negativity doesn’t stop there …

Some financial advisors will argue your investing world starts to shrink if you demand 2% or 3% (or more) income from your portfolio, so dividend investing leads to poor diversification.

My response to this: I don’t just invest in dividend paying stocks.

Further still, some advisors will argue picking dividend paying stocks may lead to negative outcomes and too many biases.

My response to this: while I believe markets are generally efficient, I also believe that buying and holding some dividend paying stocks (while there could be market under-performance at times) does not necessarily mean I cannot achieve my goals. In fact, that’s the entire point of this investing thing anyhow – investing in a manner that keeps you motivated, inspired and helps you meet your long-term goals.

Consider this simple sketch art from Carl Richards, who is far more famous than I will be, and author of the One-Page Financial Plan and more:

Source: Behavior Gap.

From Carl’s recent newsletter in my inbox:

“Pretend you live in some magic fantasy world where all of your dreams (according to the investment industry) come true, and you actually beat an index every quarter for your whole life. Congratulations!

So here’s my question: You landed in Shangri La, according to the financial industry. You beat the index. But you didn’t meet your goals. Are you happy?

The answer is “No.”

Now let’s flip that scenario on its head. The worst thing in the world happens to you (again, according to the investment industry). You slightly underperform the index every quarter for your whole life. But because of careful financial planning, you meet every one of your financial goals. Let me repeat the question: Are you happy?

And the answer is obviously… “Yes.”

Stop worrying about beating indexes. Focus instead on meeting your goals.”

Amen.

Finally, some advisors will argue that dividends and share buybacks and other forms of reinvesting capital back into the business can be equally shareholder friendly.

My response to this: Well of course that makes sense. Dividends are just one form of total returns.

But you know what?

The ability to live off dividends (and distributions from our ETFs) will be beneficial for these reasons:

1. I continue to believe there are simply too many unknowns about the financial future. So, living off dividends and distributions will help ensure our capital remains hard at work since it will remain intact.

2. If we are able to keep our capital intact we don’t need to worry as much about when to sell shares or ETF units when markets don’t cooperate. We can sell assets as we please over time.

3. Living off dividends is therefore just one way I’m trying to reduce sequence of returns risks. See below.

Source: BlackRock.

As such, we’ll try to live off dividends and distributions in the early years of semi-retirement to avoid such risks.

4. I/we don’t necessarily believe in the 4% safe withdrawal rule. It’s impossible to predict next year, let alone 30 or more investing years.

5. I’m conservative as an investor. Seeing dividends roll into my account help me psychologically to stick to my investing plan.

6. Dividends is real money, tangible money I can spend if and when I choose without worrying about stock market prices or gyrations.

7. It is my hope dividends (and capital gains) can work together to help fight inflation. As consumer prices rise, as the cost of living rises, the companies that deliver our products and services will rise in price along with them.

8. I like dividend paying stocks for a bit of the “value-tilt” they offer.

9. Canadian dividend paying stocks are tax-efficient. With my RRSP growing more with U.S. assets, I tend to keep Canadian dividend paying stocks in my TFSA and inside my non-registered account.

In a taxable account Canadian dividend paying stocks are eligible for a dividend tax credit from our government. This means taxation on dividends are favourable, it is a lower form of tax; lower than employment income and interest income. This will help me in the years to come.

Will I eventually spend the capital from my portfolio?

Of course I will.

But with a “live off dividends” mindset I can sell assets or incur capital gains largely on my own terms during retirement. I plan to do just that.

Why my goal to live off dividends remains alive and well summary

This site continues to share a journey that includes how passive dividend income can fulfill many of our retirement income needs – whether that might be covering our property taxes, paying our utility bills, delivering enough monthly income to cover our groceries, fund some international travel or all of these things combined.

Here was one of my recent updates below.

We’re now averaging over $3,300 per month from a few key accounts.

(Hint: likely more next month!)

We’re trending in a great direction thanks to this multi-year investing approach and I have no intentions of changing my/our overall approach.

I firmly believe our focus on the income that our portfolio generates, instead of the portfolio balance, is setting us up to deliver some decent semi-retirement income.

Our goal to live off dividends and distributions remains very much alive and well for the years ahead.

I look forward to your comments.

Mark Seed is a passionate DIY investor who lives in Ottawa. He invests in Canadian and U.S. dividend paying stocks and low-cost Exchange Traded Funds on his quest to own a $1 million portfolio for an early retirement. You can follow Mark’s insights and perspectives on investing, and much more, by visiting My Own Advisor. This blog originally appeared on his site on March 27, 2023 and is republished on the Hub with his permission.