By Sean Cooper

Special to the Financial Independence Hub

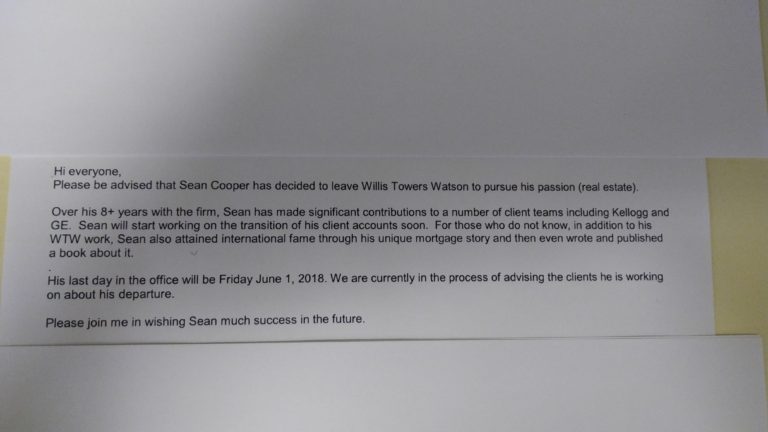

If you follow me on Instagram, you may have already heard the big news. After 8 years, I’m quitting my full-time job at the pension consulting firm. I gave my employer plenty of notice. I handed in my resignation 2 months ahead of time. June 1st will be my last day in the office. To celebrate this big career milestone, I’ve booked a weeklong trip to New York City and Boston.

I always planned to quit my full-time job. I just didn’t think it would happen so soon. I’m at a crossroads in my life. I’m 33 years old and not getting any younger. It’s time to make some tough “adult” decisions. I can either take the easy road and keep working for a company where I’m comfortable, or take the hard road and become a full-time entrepreneur. I chose the latter.

Keeping a promise to myself

A promise I made to myself after I burned my mortgage in September 2015 is that I’d slow down and get a better work-life balance. Unfortunately, that just wasn’t happening.

I’m someone who’s super ambitious. So, 6 weeks after burning my mortgage papers, I started writing a book. With the success of my book and speaking career, I’m finding myself busier than ever. I’m probably working harder now than when I was paying down my mortgage (no joke).

I’m still putting in the 80+ hour workweeks, waking up at 6:30AM and working until midnight or 1AM most days – and for what? I’m mortgage-free. I don’t have to work this many hours, but the problem is I love what I do. I enjoy my side hustle as a personal finance journalist, money coach and speaker more than my full-time job. I couldn’t keep working at this insane pace forever. I was tired all the time. Something had to give.

So with mixed emotions, in early April I made the difficult decision of choosing my budding career as a personal finance expert over my full-time career. It wasn’t an easy choice, but I was ready to make the jump.

Taking a risk

This was probably the most difficult decision I’ve ever had to make. It wasn’t easy to walk away from a steady, full-time job with benefits and a defined benefit pension plan. It was especially difficult for someone as risk adverse as me (I did after all pay off my mortgage in record timing in 3 years).

When I shared the big news with those closest to me – friends, family and coworkers – I didn’t know what to expect. Thankfully everyone has been supportive of my decision. Saying goodbye to my coworkers will be especially tough. My coworkers are like family to me. They were there when I burned my mortgage and launched my book.

It’s going to take me a while to get up and running. Luckily I have time and money. My house is paid off. I also (still) rent out the main floor of my house. The rental income alone can support me. I also have savings to last me for the years to come.

From a personal standpoint, it helps that things are less complicated. I’m single (I’m half joking when I say I’m still looking for a frugal girlfriend). I don’t have a spouse or children to look after. (Although this is a double-edged sword since I don’t have a spouse’s income to rely on either.) I’d probably hesitate to do the same thing if my circumstances were different and I was married with children.

You’ll never get rich working for someone else