As an everyday person taking a fast read of the title of the new book – Promoting the Health of Older Adults: The Canadian Experience– you wouldn’t exactly get the sense of what to be surprised by or expect what content would be covered within. In the first place, unfortunately, it’s not likely that this book will make it into the hands of everyday people any time soon.

You might ask, what are we promoting, what’s so specific for older adults – eat a nutritional diet of foods, exercise to stay fit, keep your brain active and get your proper sleep? Isn’t that what anyone through their life course should be doing? Yes, maybe. But that’s not at all exactly what you will get here.

Appreciating focus, as the writers in the preface state, the book’s main purpose is for knowledge building on issues related to older adults and their care, primarily for target audiences such as, “undergraduate and graduate students in gerontology and aging, health promotion… and other fields….” and the five groups identified include, educators, learners, policy makers, researchers and practitioners and leaders working with older adults in civic society organizations.

While that may sound too academic, after reading this book my belief is that the general public of everyday people, older adults and others younger, will also benefit greatly from an education presented here on this important subject. If you do flip through this 600-plus page tome, you might think of it at first as “insider dialogue” on health promotion; but not so fast, don’t put the book down.

Serving to heighten knowledge & awareness to engage in social health dialogue.

Choose as many words as you want; for me, Promoting the Health of Older Adults is a social health dialogue, inclusive for all Canadians – interconnected subject areas, holistic, comprehensive, diverse. The arrival of this book is timely, to promote conversation with friends and family, considering our collective journey through the COVID world to date has heightened our awareness of the workings of our own health and our social and healthcare systems.

Briefly, on the structure of this book; it certainly is more of a study text book on over thirty topic areas in seven well laid out parts. However nothing I’ve read talks over the heads of readers, and if facilitated well in a real time group discussion format, there is a set of critical thinking questions at the end of each chapter that would further serve to heighten knowledge and awareness of readers, enough to make you want to be a more engaged in this social health dialogue. Continue Reading…

Over time, most investment dealers have implemented misguided policies that will negatively affect their clients’ investment portfolios and their ability to achieve a secure retirement.

There are two main policies that have negative impacts on investors’ portfolios. One is restricting investments to a client’s original Risk Tolerance in the Know Your Client application form (KYC). When opening an account, the client will advise the dealer of their Risk Tolerance. Most clients will indicate that they are medium risk. On March 8, 2017, the Ontario Securities Commission (OSC) implemented risk rating rules that require all mutual funds to rate their fund according to 10-year standard deviation. In 2018, I published an article entitled New Mandatory Risk Rating is Misleading Canadian investors.

Prior to the OSC’s implementation of the risk rating rules, on December 13, 2013, the OSC issued CSA Notice 81-324 and Request to Comment – Proposed CSA Mutual Fund Risk Classification Methodologyfor Use in Fund Facts. My comments on this policy were submitted to the OSC on March 12, 2014, along with comments from 50 other industry experts.

A better, more accurate methodology would have used downside standard deviation or the Sharpe or Sortino ratios which measure risk adjusted returns. Nevertheless, the OSC implemented risk rating rules requiring all mutual funds to rate the risk of their funds according to 10 year standard deviation.

As a result, if investments in a client’s portfolio exceeded the risk tolerance as indicated in the original KYC, the client was forced to redeem those investments, by the advisor’s compliance department. A number of BMG’s clients were forced to redeem their positions since our funds had a medium-high risk rating according to the OSC formula, and the clients’ KYC indicated medium-risk tolerance. A number of clients wanted to change the KYC in order to allow them to maintain ownership of our funds but were advised that, unless there was a significant change in their financial circumstances, they could not change their KYC.Continue Reading…

Becoming a first-time homeowner is an exciting prospect. It’s a chance to have a place you can call your own, where you can make memories for years to come.

With that said, proper planning is necessary, or your dream can become a financial nightmare. The fact is that there are many unavoidable and potential expenses that could occur over time, and if you don’t understand the realities or you don’t save appropriately, then you could be in for some hard times.

To help you out, we have compiled a list of common expenses that most first-time homeowners will experience and how to prepare accordingly.

1. Closing Costs

As you are looking at potential homes and comparing your financial situation, you will want to keep in mind that there are some upfront expenses that you will want to consider, especially closing costs, which may amount to 3-6% of the total loan value. It is important that you have those funds fluid and ready to go when you sign your new mortgage.

If you are short on funds, then consider creating an agreement with the seller to share these costs or look into government programs if you are short.

2. HVAC Issues

No matter where you live, yyour HVAC (Heating, Ventilation, and Air Conditioning) units will likely need to be repaired either soon or down the road. While most units can last 10 to 15 years, if you run your heat or AC all day, every day, then you could be looking at a repair sooner than later, especially if you bought a home with an existing unit.

When preparing for the expenses associated with a damaged air conditioner, you will need to decide if you can have your unit repaired or if it will need to be completely replaced. The first thing you should do is get a quote from a professional to see if the cost to repair is almost as much as the cost to replace. If it is, consider getting a brand new unit because you know it will last a long time and work at high efficiency. Also, consider the fact that if your AC had to be repaired once, it will probably require maintenance again. Include these considerations in your final decision.

3. Appliance Lifetimes

Whether you are moving into a home with existing appliances or you are buying them brand new, you must realize that all appliances have their expiration date. For instance, refrigerators often last about 10 years, and even if they are still usable after that time, their efficiency will begin to dwindle. As far as other appliances:

Washers and dryers typically last about 10-13 years.

Dishwashers have about 10 years.

Microwaves typically last around seven years.

Knowing these dates is important so you can begin to budget accordingly to pay for a replacement.

As a new homeowner, an expense that you may want to incur is the cost of a home warranty. Many of these programs cover a portion of the price of the service calls necessary to fix your appliances, and your annual fee will also help with the cost of a new unit. As soon as you move into your home, look for home warranty programs and find one that suits your needs and financial situation.

4. Roof Damage

The roof is arguably one of the most important aspects of your home, and if it is damaged by weather or general wear and tear, then you will want to have it inspected and repaired immediately. Typical roofs built with asphalt shingles will last about 20 years, so if you have a new home, you may be good for a while, but if you bought a used home, then you will want to see how much time is left. Continue Reading…

Most investors do not like volatility. They do not like looking at their investment account balance observing that they’ve ‘lost money.’

Of course, you have not lost money until you buy an asset at a certain price and then sell at a lower price. You’ve then just realized your losses. You have not lost money when your portfolio value goes down. And in fact, swings in portfolio values are just par for the course. Stocks and bonds and real estate change in price (with wild swings at times) in regular fashion: it’s normal behaviour. If the stock markets have you spooked, there is a simple and timeless plan of action.

With this strategy, you can ‘win’ if stocks go up. You can win if stocks go down. It’s a strategy that worked during the worst period in stock market history: the Great Depression of the 1930s .

The answer of course is adding money on a regular schedule. In the investment world they call it dollar cost averaging; we can abbreviate that to DCA. There is no need to guess about which way the market is going to go today, next week, next month, next year, or even the next five years. We simply expect or hope that the markets will go up over longer periods, as they have throughout history.

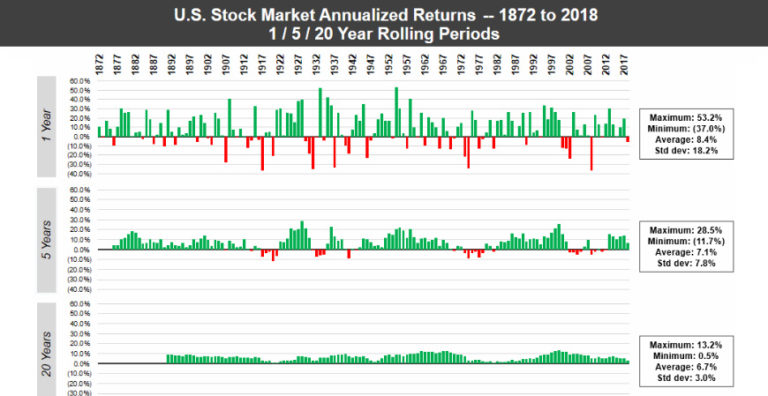

Stock market history

U.S. stocks, S&P 500

You can see that there is lots of green on the board. Stocks mostly go up. It is those pink years (on the table) that usually trip up many investors

The key to long-term wealth building is being able to invest through those down years. And in fact, adding money in those years is quite beneficial as the stocks go on sale.

But keep in mind that stocks can stay under water for extended periods.

Dollar cost averaging

Now this is a consideration for those who have very little exposure to stocks, or who have been out of the markets for quite some time. That event is not as rare as you might think. Many investors have left the markets, though they recognize that they need to be invested to reach their financial goals and enjoy a prosperous retirement. They also want their wealth protected from inflation.

Here’s the demonstration: investing through the initial stages of the Great Depression.

In the above charts we see equal amounts invested, but the dollar cost averaging strategy still delivered positive returns in a vicious bear market. Buying at those lower prices was very beneficial. Now keep in mind for the above to work, the markets have to go up over time. They have to recover. And historically they have.

Time reduces risk

Here is a wonderful graphic that demonstrates the returns over various periods. Our odds increase as we lengthen the time period that we remain invested.

And a table that frames the probabilities of positive returns.

Charlie Bilello

Spread out that lump sum

If you are sitting on a large sum that you want to get invested you will have to have a plan. Over what time period should you get those monies into the market?

If you start investing and the markets keep going up, great. Mission accomplished. The money you’ve invested has increased in value. You are collecting dividends along the way.

But of course when we enter a stock market correction, your total portfolio value will decline. Though you might get enough of a head start so that your money invested remains in positive territory.

At that point when markets are declining, remember that lower prices are good. The stocks are going on sale. And of course, you do not have to invest in an all-equity portfolio. You can dollar cost average into a balanced portfolio.

I’d suggest that you spread the money out over 2 or 3 years. For example, If you are on the 2-year plan and have $100,000 to invest and you’re investing every month, you’d invest $4,167 per month.

You can’t time the markets

For those who already have substantial assets invested, you can’t move in and out of the markets. We don’t know when the corrections will occur. The most reasonable course of actions is still dollar cost averaging. That said, whenever you have money to invest, stock market history says get it invested. The sooner the better.

This is key. If you get scared and sell, you might lose money.

You might have to accept a lower-risk portfolio that is likely to earn less over time compared to a more aggressive stock-heavy portfolio or balanced portfolio. It’s also possible that you do not have the risk tolerance to invest (at all), even in a very conservative ETF portfolio. If that is the case you would have to stick with GICs and high-interest savings accounts. You might add to your real estate exposure for growth. In retirement, you might use annuities to boost your income.

For savings we use EQ Bank. 3-and 6-month GIC’s now 2.05%

To help gauge your risk tolerance level and the appropriate level of portfolio risk, please have a read of the core couch potato portfolios on MoneySense. You’ll find a table within that post that breaks it down.

If you are risk averse, you likely need a managed portfolio and advice. You might consider a Canadian Robo Advisor. These investment companies provide lower-fee portfolios at various risk levels. Advice is also included. A few of these firms also offer financial planning.

At Justwealth, you get access to advice and financial planning. In fact, you’ll have your own dedicated advisor.

They will do a risk evaluation to see if investing is right for you, and then you will be placed in the appropriate portfolio(s). And once again, you’ll be offered the greater financial plan as well.

Start investing

Preet [Banerjee] puts some of the above in video form [YouTube.com]. Preet also goes over how much you might market over various time frames, at different rates of return.

The key is to not be frozen on the sidelines. We might refer to that as ‘paralysis by analysis’.

Build wealth at your own comfort level, at your own pace. You will learn as you go. You can build up your comfort level for risk and volatility. It’s quite possible that you can increase your risk tolerance level over time. We develop risk callouses.

Thanks for reading. We’ll see you in the comment section. If you’re not sure what to do, feel free to flip me a note.

Dale Roberts is the Chief Disruptor at cutthecrapinvesting.com. A former ad guy and investment advisor, Dale now helps Canadians say goodbye to paying some of the highest investment fees in the world. This blog originally appeared on Dale’s site on Feb. 12, 2022 and is republished on the Hub with his permission.

Retirement planning used to be easy: you simply applied for your government benefits and your company pension at age 65. So, when did it get so complicated?

Things started to change in 2007 when pension splitting came into effect. While we did have Canada Pension Plan (CPP) sharing before that, not too many people took advantage of it. Then Tax Free Savings Accounts (TFSA) came along in 2009. At first you could only deposit small amounts into your TFSA, but in 2015 the contribution limit went to $10,000 (it’s since been reduced to $6,000 per year). Accounts that had been opened in 2009 were building in value, and the market was rebounding from the 2008 downturn. Registered Retirement Savings Plan (RRSP) dollars were now competing with TFSA dollars and people had to choose where they were going to put their retirement money.

In 2015 or 2016 financial planners suddenly started paying attention to how all of these assets (including income properties) were interconnected. There were articles about downsizing, succession planning, and selling the family cottage. This information got people thinking about their different sources of retirement income and which funds they should draw down first.

Of course, there is more to consider, such as the Old Age Security (OAS) clawback. When, where, and how much could this affect your retirement planning? People selling their business are often surprised that their OAS is clawed back in the year they sell the business, even if they’re eligible for the capital gains exemption. Not to mention what you need to do to leave some money behind for your loved ones. Even with all this planning, the fact that we pay so much tax when we die is never discussed, although the final tax bill always seems to be the elephant in the room. We just ignore it, and hope it’ll go away.

Income Tax doesn’t disappear at 65

Unfortunately, income tax doesn’t disappear at age 65, and you need time to plan ahead so you can reduce the amount of tax you pay in retirement. A good way to do this is to use a specialized software that takes all your sources of income and figures out the best strategy to get the most out of your retirement funds.Continue Reading…