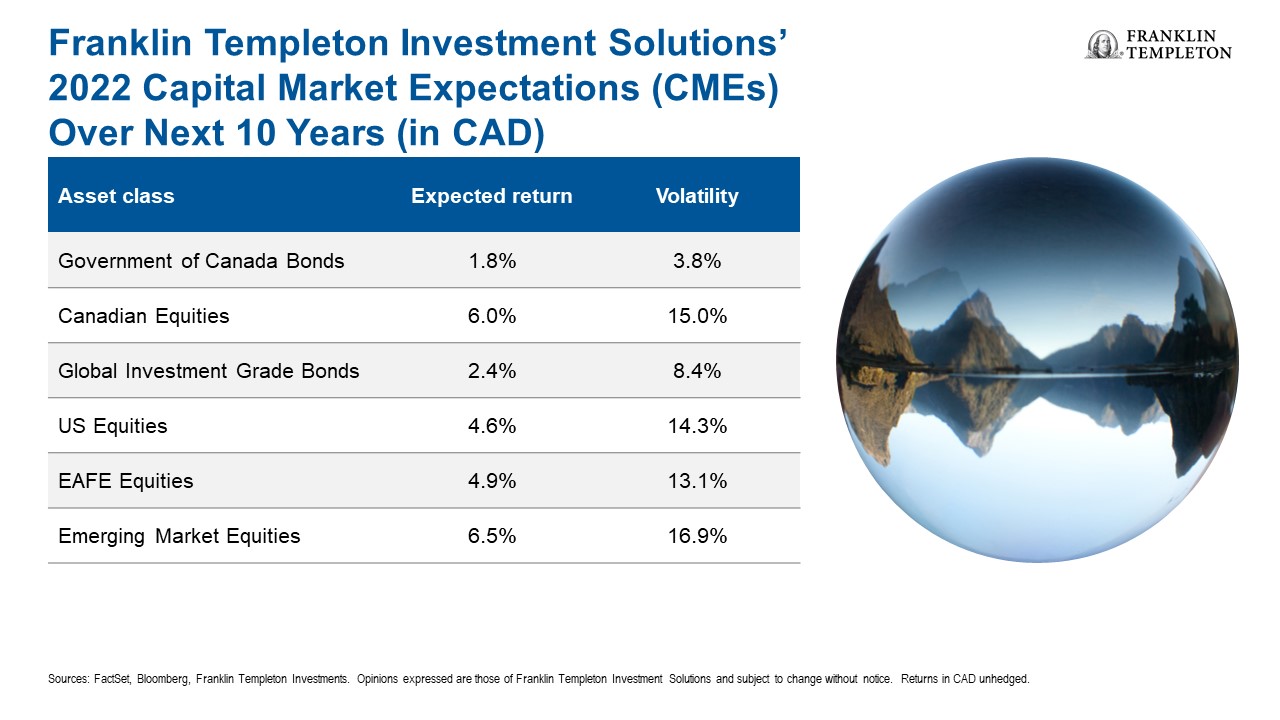

Investors should expect North American and international equities to continue to outperform bonds over the next ten years, according to senior portfolio managers for Franklin Templeton Investment Solutions. As the accompanying chart illustrates, expected returns for equities the next 10 years range from a 4.6% for US stocks to a high of 6.5% for Emerging Markets stocks. Canadian stocks are expected to do almost as well, at 6%, and EAFE equities will also outperform US stocks, with retiring expectations of 4.9%.

Returns for bonds are more modest: Franklin Templeton projects 1.8% return for Government of Canada Bonds and 2.4% for Global Investment Grade Bonds. The chart shows the volatility, topped by Emerging Markets at 16.9% and Canadian equities at 15%.

The forecasts were provided Tuesday at a virtual webinar at the Franklin Templeton 2022 Global Investment Outlook.

3% Global Growth should keep pace with Inflation

Over the next 7 to 10 years, the firm expects 3% annual global growth, roughly keeping up with inflation, said CFA William Yun, executive vice president for Franklin Templeton Investment Solutions. Over that time, equities should outperform fixed income and non-US equities should outperform US equities, he said.

Looking to Canada, Canadian stocks should have slightly higher expected returns, albeit with greater volatility, said Senior Vice President Ian Riach. The outperformance will be because of lower “more reasonable” valuations for Canadian stocks, he added. “We are quite positive on the Energy and Financial Services sectors.” Continue Reading…

The old joke is that opinions are like noses – everybody has one. The other thing everyone says about opinions is that we’re all entitled to them. If we’re speculating about how things that have never happened in the past might play out in the future, there’s also a bit of fun involved. Friends can rib each other about which among them is the better prognosticator. Adam Grant’s latest book, Think Again, encourages readers to rethink what is already known, which might just mean ‘what they believe.’

Grant says we should beware the “I’m-not-biased” bias: recognizing the flaws in other people’s thinking, but assuming you’re immune. He says the less biased you think you are, the less likely you are to catch yourself. To paraphrase: “If knowledge is power, then knowing what you don’t know is wisdom.” It might also be handy to keep a mirror handy and question your own beliefs more often.

The next Bear market

I’ve recently completed an exchange with a friend about one of the most common financial advisor narratives and how those might play out if there was to be a prolonged and severe bear market. To begin, although I personally think such an outcome is probable in the near term (which created a sense of urgency for the thought exercise), the important thing is to game out what we think and why we think it before the event happens. Other than reading my thoughts into the record for posterity, the timing is inconsequential. We may not have a large enough drawdown in the next 20 years, so we may not be able to test which hunches are closer to the mark during my career.

This exercise is especially interesting when we think of the lack of reliable counterfactuals. Basically, advisors say they do a good job of keeping people invested in bear markets and naturally want to take credit for doing so. The questions abound:

What would clients have done if they hadn’t worked with the advisor?

If the advice was consistent to hold and (say) 95% of clients held, is there culpability for the 5% who sold?

What if (say) 85% of the clients would have held if left to their own devices, anyway?

Combining the two hypothetical points above, the changed behaviour is felt for only 15% of clients, 10% who held when they would have otherwise sold; 5% who sold despite being advised to hold. Would that justify a narrative of ‘advisors adding value through behavioural coaching’?

If the drop is bigger and lasts longer, clients might behave differently, so what does this mean for advisor accountability? Taking or foregoing credit or blame regarding client conduct might change if one offered the same advice but got different outcomes as the situation dragged on.

Here’s a fun one: If an advisor gets credit for encouraging a client to hold through a 30% drop and then the market drops a further 30% and the advisor still encourages the client to hold, but the client sells, would it have been better for the advisor to have allowed the sell to have taken place sooner? If yes, is that advisor ‘worse’ for not allowing the client to sell sooner?

My concern in this exercise is a sort of first-derivative optimism bias. I have a view that advisors are optimistic in general. Continue Reading…

On Friday, the Hub republished the first part of a two-part Question-and-Answer session between finance professor and author Dr. Moshe Milevsky and Gordon Wiebe of The Capital Partner [TCP]. This is the second and final instalment:

TCP: I wanted to turn to your Book, Longevity Insurance for a Biological Age. Your thesis is that we should be looking at our biological age and using that to calculate and project our income and how much we should be drawing from our savings.

M.M. And, more importantly than that, making decisions in our personal finances, right?

You know, somebody is trying to figure out at what age they should take C.P.P. Should I take it at 60? 65? 70?I don’t think they should use their chronological age to do that.

Trying to figure out when to retire? Stop using your chronological age.

I mean there’s a whole host of decisions that you have to make based on age and I’m saying we’re using the wrong age metric. It should be based on your biological age.

Now, at this point, biological age sounds like this funny number that comes out of some website, but sooner or later we’ll all have it. And, it’s going to be faster than you think. Your watch will tell you your biological age. And, then in a couple of years, people will stop associating themselves with their chronological age.

They will just stop using it.

And you’re going to sit down with your antiquated compliance driven forms that say, “I need to know my client’s age. Oh, you’re 62.”

And, the client says, “Ha, ha. That’s chronological age. We don’t use that anymore, buddy. I use biological age. Sixty-two, that’s not my age.”

It’s about preparing people for the world in which age is not the number of times we circle the sun.

TCP: What metrics do you think we’ll lean towards to measure biological age? Telemeres? Others?

M.M. There’s a whole bunch of bio-markers that can be used. Some people use telomeres or something called “DNA methylation” or epigenetic clocks. There are about fifty of them, but eventually they’ll all coalesce into a number called “biological age.”

There will be a consensus on how to measure it and you’ll go to your doctor and your doctor will say, “your chronological age is 50, but your biological age is 62.” You’re doing something wrong.

Then a financial advisor will use that information differently when you build a retirement plan.

TCP: That makes sense, but trying to achieve a consensus and getting everyone to use the same metrics from a compliance standpoint or trying to get pension plans and policy makers to agree would be a challenge, wouldn’t it?

MM: It would be. In fact, that’s exactly where I’m headed now. I’m giving a speech in Madrid and that’s exactly what regulators from a number of different countries want me to talk about.

They want to know, “is this feasible? We want to implement this in our pension system. We don’t want wealthy people retiring at the age of 65, they’re going to live forever and bankrupt our system. We want people to retire at a biological age.”

TCP: Let’s talk about that a little more. Advisors typically use a 4% draw on savings as a benchmark withdrawal rate. But, if we use our biological age, there would then be a range. I assume somewhere between 3-6%?

Adjusting the 4% Rule

M.M. You’re absolutely right. That’s where I would go with this. You have to use your biological age and the 4% rule has to be adjusted.

But, what I’m saying is more than that. That rule has to change. It’s not just about the number or percentage. It’s how the rule is applied.

I really don’t like the idea of fixing a spending rate today and sticking to it for the rest of your life no matter what happens. Your spending rate has to be adaptable.

What you have to tell people is, “look, this year we can pull out 6.2%. Next year, it really depends on how markets behave. If markets go down, we may have to cut back. If markets go up, we can give you a bit more.”

I think the 4 per cent rule is really what I call a one-dimensional rule. It’s not that four is one dimensional. Any one number is one dimensional: just telling them a per cent.

It’s got to be at least two dimensional. Meaning, this is what it is now, but next year if this is what happens we’ll do that. ..

Three dimensional is to go beyond that is to go beyond that and say let’s take a look at what other income and assets you have.

“Oh! You’ve got a lot more income from guaranteed sources, you can afford more than four per cent, this year.”

TCP: It’s a dynamic scenario, a moving target.

M.M. That’s the key word, dynamic versus static.

The threat of rising Interest Rates

TCP: Canadian investors currently have over two trillion invested in mutual funds. Over half is invested in balanced funds or fixed income and we’re in a horrible position where fixed income is concerned. We’ve had declining rates for the past forty years. At best, bonds will stay flat. At worst, bonds could lose up to thirty per cent of their value.

You talk about the importance of the sequence of returns and how that affects income potential. Have you or your students run scenarios with higher interest rates and the impact it could possibly have?

M.M. I haven’t thought about it beyond what you’re noting. The obvious scenario is as interest rates move up, these things are going to take a big hit.

And, retirees who feel they’ve been playing it safe by putting funds in bonds will suddenly realize there’s nothing safe about bonds in a rising interest rate environment.

I think they’re confusing liquidity and safety with interest rate risk. It’s liquid and its safe. Government is not going to default but boy, can it lose its value.

We’ve become accustomed to this declining pattern. Anybody who is younger than forty doesn’t even understand what higher interest rates means. It’s never happened in their lifetime. They don’t believe it. Understand it. Never felt it. You show them graphs going back to the 1970s. That’s not how to convince them. They’re empiricists. They’ve never lived it themselves, they don’t believe you. Continue Reading…

Professor Moshe Milevsky wants us to re-think the metrics we use for retirement calculations. Instead of basing retirement income amounts on our age i.e., the number of orbits around the sun, Dr. Milevsky suggests we consider using our biological age. What is your biological age?

Advances in science suggest our biological age is based on our actual physical shape or our personal physiology. Rock stars like Sting, Phil Collins and Ace Frehley were born in 1951. Their legal age is 70, but their actual condition may be substantially different from Mark Hamill (Luke Skywalker) or Dr. Jill Biden (U.S. First Lady) who also turned 70 in 2021.

The cumulative effects of genes, lifetime dietary habits, exercise, social conditions and stress levels for instance, could lengthen or decrease life expectancy and therefore provide a better indication of future retirement income needs. Recent scientific advances are helping make this information more available to seniors, advisors, researchers and policy advisors.

Background

TCP: From where does your passion for mathematics originate?

M.M. I guess it comes from my life as an undergrad. I was taking various courses including one on English literature and essay writing. I handed in an essay and received a bad grade. The professor said, “You really can’t write to save your life, you might want go into math.”

I did and I got an undergraduate degree in mathematical physics. Then, I went to graduate school and studied math and statistics, but I was really interested in gravitational physics. That was my thing, like how a golf ball moves after a drive, the arc that it makes, etc.

My thesis supervisor said, “Moshe, you’ll never find a job with that kind of specialty. You might want to go to business school.” So, I moved into business and finance and it’s where I’ve been for the past 25 years.

TCP: You also have a passion for financial history. Is there a period in history that strikes you as particularly innovative or ingenious?

M.M. There is. I’m interested in the 17th century, specifically 17th century Europe and the evolution of financial products, instruments, and economics.

Anything from the crowning of James II in 1685 until the ascension of George II in the mid-18th century.

TCP: I’m not that familiar with that era. Does it line up with the advances in math, probability, and statistics?

M.M. It does. There was this interesting alignment of people interested in mathematics and statistics and they developed the basics of probability theory, economics, and finance. It was an alignment of interests that led to many of the instruments we use today.

You know, nobody would say that 1690 was the origin of the i-Pad or the i-Phone or the laptop. But, many of the financial instruments we use, whether it’s pensions, annuities, stocks, bonds, mutual funds, they all kind of originated in the late 17th century. You can almost trace back a direct line. I’m fascinated by that. It interests me and I’ve spent a lot of time looking at history from that period.

TCP: Among other things, the pandemic has shown how segments of the population struggle with basic math principles. Are you surprised by the lack of financial literacy?

M.M. It is a problem the pandemic has brought home. I think it’s a problem that finance has brought home. A lot of people are incapable of mathematical reasoning and that’s not healthy in today’s very quantitative, data driven environment.

Thousands of years ago, you had to make sure to out run the dinosaurs and get home in time for dinner. What did your brain have to do? Nobody was asking you to solve calculus problems.

Now, we have to evolve to deal with these very quantitative issues and make decisions and I think the pandemic has brought that home very starkly. There’s some completely irrational decision making because of a misinterpretation of probabilities and the odds. Just look at Toronto.

There are 300 infections, and everybody is walking around like it’s Ebola and every other person has it. In some sense, you have to step back and say, “Wait a minute. What are the probabilities? Do you understand all of the things you’re sacrificing?” It’s all probabilities. Those things all come down to mathematical reasoning.

I do think the educational system should focus more on some of these statistical, data driven issues. I think financial literacy is an absolute must.

My bread and butter is teaching undergraduate students at the university. Undergraduate Personal Finance. That’s a course I’ve been teaching now for almost twenty years.

It’s basic personal finance. You know. What’s a tax return? What’s an insurance policy? How does a mortgage work? What’s an RRSP?

Why do I have to teach this to 22-year-olds? Why don’t they know this from high school? Why isn’t this covered before I see them? And, why are only the ones that I teach in Business School getting this? What about the rest of the students who are studying something else? Why is this not considered a national emergency? People are wandering into the world without the requisite tools.

TCP: Carrying credit card balances in perpetuity, putting 5% down on million-dollar homes …

M.M. Let alone, just verify that what they’re paying is correct, right? Nobody’s able to do that because it’s all coming from calculations that are being done by algorithms that nobody wants to or even knows how to verify. So, there are a number of things that worry me.

The Mathematics of Retirement Income

TCP: I haven’t had a chance to watch the movie “The Baby Boomer Dilemma,” yet. I’ve just seen the trailer.

M.M. Yes, that’s an interesting one. I’m not sure how I got dragged into that, but I now have an IMDb movie rating. I am now officially a Hollywood actor (chuckling). Go figure.

TCP: On the trailer you say, “what’s been happening over the last few years is our accounts have been growing. It looks like we are getting wealthier. But, the income that we can get from that sum of money is shrinking.” What did you mean by that? Continue Reading…

I was the first investment blogger to ‘jump on’ the investment risks that might be created by the coronavirus. In fact, when I first penned on the subject in February of 2020, the virus was not then known as COVID-19. And we were not yet in a global pandemic. New cases were just starting to move around the globe, and most felt that the strange new coronavirus would be contained. Today, I can’t claim that I knew it would result in the first modern pandemic. But I did address the risk, and I did offer some thoughts on how an investor might prepare, if they needed to protect their wealth. Let’s have a look, how did the pandemic portfolio perform?

That almost goes without saying. You don’t fix a ship in a hurricane offers our friends at Mawer Investments. If you have a solid investment plan, and you are investing within your risk tolerance level —

This suggestion is controversial to some, but to me it is common sense. Fear was mounting in February of 2020, and the stock markets were offering a minor hissy fit. It is safe to say that most investors are not safe. They are investing outside of their risk tolerance level. These market scares offer the opportunity to discover that you are investing outside of your comfort level.

The timing from February of 2020 to de-risk was still quite favourable.

That would have allowed an investor to move to their risk tolerance level before the market corrected by nearly 35%. While that move to a lower risk portfolio might create lesser returns over time, it can remove the greater risk of permanent losses. Investors are known to too-often sell out in fear near the bottom of the market declines. Of course that’s the complete opposite of – buy low and sell high.

And a typical balanced portfolio would have delivered about 21% to 22% to date, from February of 2020. That’s a greater return compared to the Canadian stock market from that date.

Pandemic portfolio construction

I had suggested that investors consider two of the greater risk-off assets. Risk-off will refer to the defensive investments that protect your portfolio. And typically, investors run to these assets in times of trouble. That influx of dollars can drive up prices.

Gold is known as a safe haven asset.

Gold was the lead image on the original post on how to prepare your portfolio for the pandemic. The precious metal did shine in the pandemic, when needed.

I had suggested that investors consider U.S. long term treasuries. They punch above their weight as risk mangers (keeping an eye on those unruly stock markets.

If an investor had shaded in some gold and long term treasuries, they would have experienced some greater returns, and would have been treated to better risk-adjusted returns.

The pandemic portfolio performance

For demonstration purposes I used the asset allocation offered on the ETF Portfolio page, for a balanced model. You certainly could have (successfully) held a conservative, balanced growth or all-equity model through the pandemic. But for those with a balanced model that holds some risk-off assets, the inclusion of gold and treasuries would have helped the cause. Continue Reading…

Investors should expect North American and international equities to continue to outperform bonds over the next ten years, according to senior portfolio managers for Franklin Templeton Investment Solutions. As the accompanying chart illustrates, expected returns for equities the next 10 years range from a 4.6% for US stocks to a high of 6.5% for Emerging Markets stocks. Canadian stocks are expected to do almost as well, at 6%, and EAFE equities will also outperform US stocks, with retiring expectations of 4.9%.

Investors should expect North American and international equities to continue to outperform bonds over the next ten years, according to senior portfolio managers for Franklin Templeton Investment Solutions. As the accompanying chart illustrates, expected returns for equities the next 10 years range from a 4.6% for US stocks to a high of 6.5% for Emerging Markets stocks. Canadian stocks are expected to do almost as well, at 6%, and EAFE equities will also outperform US stocks, with retiring expectations of 4.9%.