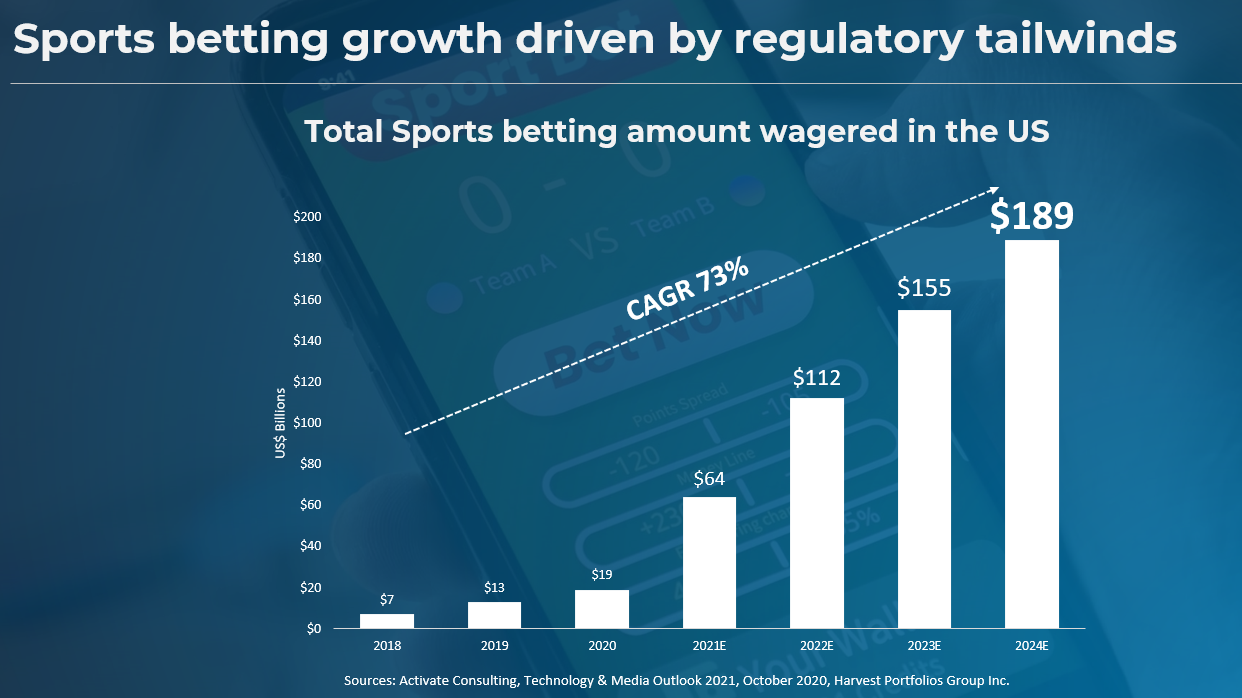

My latest MoneySense Retired Money column, just published, looks at the commonly held dream of many in the FIRE community (Financial Independence/Retire Early): that of geo-arbitrage and retiring outside Canada to an exotic location with a much lower cost of living. Click on the highlighted text for the full column: Has the Pandemic ended the dream of Retiring Abroad?

My latest MoneySense Retired Money column, just published, looks at the commonly held dream of many in the FIRE community (Financial Independence/Retire Early): that of geo-arbitrage and retiring outside Canada to an exotic location with a much lower cost of living. Click on the highlighted text for the full column: Has the Pandemic ended the dream of Retiring Abroad?

As I note in the piece, places like Mexico, the Far East or parts of Europe have such a relatively low cost of living that average Canadians might be able to retire early just on the strength of CPP and OAS. Add in any employer pensions and registered or unregistered savings and that would be gravy.

The column looks in particular at two locations in Mexico that are quite popular with both American and Canadian expatriates seeking nicer weather and a lower cost of living. One is Lake Chapala, the subject of a new edition of a book by regular Hub contributors Akaisha and Billy Kaderli. The book, pictured on the left, is titled The Adventurer’s Guide to Chapala Living.

“Chapala isn’t the only town/city where living in Mexico is wonderful. There are so many from which to choose,’ Akaisha told me via email, “ We believe retiring abroad is still feasible, without a doubt.”

At one point my wife and I seriously considered leaving the Land of Snow and High Taxes (aka our Home and Native Land) for Mexico. We took one trip to Chapala and nearby Ajijc, and a few years later the more inland and mountainous San Miguel de Allende, more on which below.

However, as the years went by and we neared our Findependence Day (i.e. Semi-Retirement), we concluded that there was too much crime in Mexico for our liking and that we are for the most part quite content to live in our current home in Long Branch, Ontario, just steps from Lake Ontario.

Even so, and as the MoneySense column relates in more depth, we do know a couple who actually took the plunge and sold their Toronto home to start a new life in San Miguel de Allende. Five years ago, the Hub recalled that trip and how we ran into a former Financial Post colleague of mine, Dean Cummer, and his partner.

They visited Toronto recently and I got the chance to catch up over lunch with Dean, who became one of the main sources for the MoneySense column: my editor wanted to know whether the dream of Retiring Abroad is still alive in the Covid era. Continue Reading…