A quick note to say Happy 2022 to all the Hub’s readers and supporters. We’ll be back to our regular blog-a-day rotation on Tuesday.

In the meantime, I’ll point readers to Dale Roberts’ excellent year-end market wrap for MoneySense, which was published Friday.

Click on the highlighted headline to access, but settle down with a coffee before you do: it’s quite a long read: Making Sense of the Markets: 2021.

It’s a thorough long read that looks at all the major market developments each month in 2021 and you’ll also see a number of prescient market calls made by Dale over the last few years, including an early call on Covid-19 itself, an early call on the Energy and Commodities recovery, and several others.

I’ve followed Dale for some years now: he famously tweets as @67Dodge and I now help edit his weekly MoneySense market wrap, seeing as I became MoneySense’s Investing Editor at Large a few months ago.

Don’t forget to contribute to your TFSA ASAP

Oh, while on the subject of MoneySense New Year’s content, I may as well point those to my own column that ran a few days ago: Why contributing to a TFSA is a good (New Year’s) resolution.

In normal years, I would move new money into the TFSA on January 1st but there’s probably no rush this year until Tuesday, Jan. 4, seeing as the Canadian market is closed Monday. (The US will be open that day though).

I’ve not decided exactly what to invest in but it will likely be inflation-related. Going back to Dale Roberts, you can glean a few ideas from his 2021 market wrap: things like short-term TIPS ETFs, or the Purpose Real Assets ETF, or energy/commodity plays.

Personally, I’ve been researching Ray Dalio’s All-Weather portfolio (google it for videos and articles, or try this Seeking Alpha link on it). I’ve concluded that our own family has sufficient US equity exposure but not enough in commodities or TIPS [Treasury Inflation Protected Securities] plays.

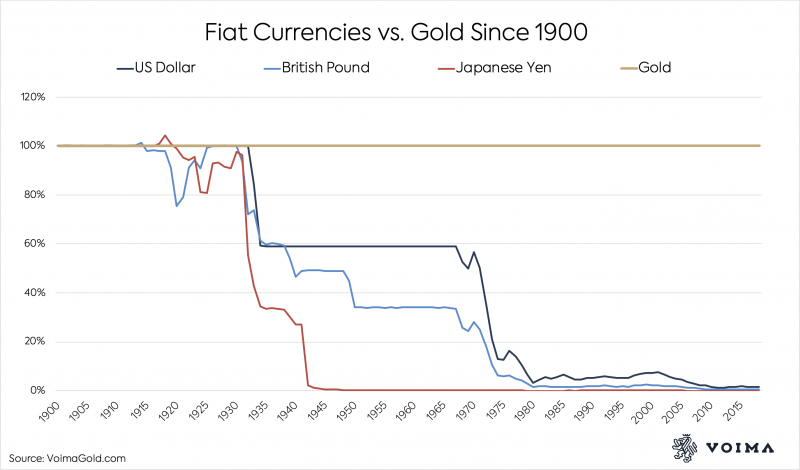

Dalio is a bit heavier on fixed-income than most, with a mix of long-term and short-term bonds. His recommended equity exposure is a bit lower, and he suggests 7.5% commodities and 7.5% in gold. Readers may therefore find Friday’s Hub article on gold of interest: A perfect storm for gold.

Every case is different of course. IF I were looking to boost US equity exposure, I’d certainly be considering the new Canadian Depositary Receipts (CDRs), more on which you can read on the Hub early in the new year. If we didn’t already own Berkshire Hathaway, I’d be tempted to add to it with the CDR version of Berkshire, seeing as it pays no dividends and would be a good value counterbalance to high-priced US tech stocks.

So by all means get your $6,000 (if available) into your TFSA early in 2022 but take a few days to figure out how to invest it.

The wild card is certainly Omicron. If you’ve not yet gotten your booster, I highly recommend it.

So again, have a happy, healthy and profitable 2022!