For the first 30 or so years of working, saving and investing, you’ll be first in the mode of getting out of the hole (paying down debt), and then building your net worth (that’s wealth accumulation.). But don’t forget, wealth accumulation isn’t the ultimate goal. Decumulation is! (a separate category here at the Hub).

Director, Financial Planning Centre of Expertise, RBC

(Sponsor Content)

If you’re like many Canadians, with 2022 around the corner, you’re likely thinking about what you would like to achieve in this new year.

You can begin by having a good look at your current financial situation and the steps you can take to stay on top of your money.

As we consider what this year will bring, here are five areas of personal finances you can focus on to get 2022 onto solid financial footing:

• Make sure your financial plan still works for you

As the economy continues to recover and we look toward whatever this year holds, having a financial plan can help you take stock of where you are and what you need to do to continue to work toward your financial goals.

A financial plan can help strengthen your confidence when it comes to managing your money, both now and in the future. Taking the time to build a plan that works for you and your unique financial situation is a good start. Use your plan to identify your goals and objectives, evaluate your finances and put steps in place to achieve your financial goals. It’s also important to revisit your plan regularly, especially as your finances or priorities change.

• Stay on top of your cash flow

As inflation continues to impact Canadians’ purchasing power, cash flow will become an even more important part of managing personal finances in 2022. Here’s where having a budget, to complement your financial plan, is a huge help. A budget will give you a good picture of the money you have coming in and going out.

If you already have a budget, it’s a good time to review and update your expenses to account for rising costs: from gas and groceries to utilities and activities. This will help you see what you may have left over to put into savings.

Managing any debts and how you plan to pay them off is also an important part of managing cash flow. A piece of advice here: Don’t worry about paying all your debts at once. Instead, focus on taking care of higher interest rate debts first. This will have a good impact on your overall financial health, to help you worry less and save more.

New digital tools, like NOMI Budgets and NOMI Forecast can also help you stay on top of your money and avoid unnecessary expenses. Available to RBC clients through the RBC Mobile app, NOMI Budgets simplifies the budgeting process by taking a close look at your spending and recommending a personalized monthly budget based on your habits. NOMI Forecast learns from your past transactions and uses predictive technology to provide a rolling forecast of your expenses for the next seven days.

• Be prepared for the unexpected

One important lesson the pandemic has taught us is that the unexpected can happen at any time. It also has reinforced the importance of having an emergency fund that you can rely on to help cover the costs of unexpected expenses like loss of income or repairs to vehicles or flooded basements.

Setting up an automatic savings plan can make it easier to save regularly. Using a digital savings account like NOMI Find & Save can also help, as it finds extra money in your cash flow it thinks you won’t miss and automatically sets it aside. If a payment or transfer is due to come out of your linked chequing account, the money is automatically transferred back to ensure you have what you need to cover those transactions.

• Look past the headlines when investing

It can be tempting to do ‘emotional investing’ – reacting to negative headlines and market volatility by altering a well-designed investment plan. While selling off your portfolio may make you feel better, this decision could mean lost opportunities and not achieving your long-term investment goals. Continue Reading…

Wine investing in North America is hitting the mainstream.

Historically, the wine investment category has been perceived as only for the wealthy or wine experts.

Although traditional HNW [High Net Worth] investors have been investing in portfolios of fine wine for years, it is still a new asset class for some.

However, new specialist services are opening up the fine wine investment universe. Cult Wines, whose story began in London, England in 2007, recently expanded into North America with offices in Toronto and New York. Known as ‘The Americas,’ our task is to build the awareness of fine wine and accessibility to the asset class. In addition, Cult Wines recently introduced a new platform, new product structure and new technology to better serve our clients.

Our expension into The Americas is helped by fine wine’s strong track record of consistent returns and low volatility. Currently, the asset class is enjoying a sustained rally with year-to-date returns over 13.7% through the end of October, as measured by the Liv-ex 1000, an index of some of the most sought-after investment wines from around the world.

The U.S. is the world’s largest Wine market

The US, the world’s largest wine market, is a natural fit for wine investment. 49% of Americans drink wine and 431 million cases of wine were sold in 2020. The US has been making some investment grade wines for decades and to the end of October, the California 50 wine index is the third best performing wine region globally with a year-to-date return of 16.5%. Continue Reading…

Almost since the Hub’s inception in 2014, the principals behind the popular RetireEarlyLifestyle.com have provided in-depth coverage of global travel and the tips to achieve early Financial Independence they used themselves to “retire” in their early 30s.

The following email interview was between myself and Billy and Akaisha Kaderli. Our intention is to publish it on both sites. Here’s the link to their version, which ran Dec. 14th.

So without further ado:

JC Q1: Akaisha and Billy, you are about the same age as myself and my wife Ruth and apart from being American and Canadian, we appear to have several things in common: we both run sites focused on Financial Independence, have written some books on same, and continue to be working at least on our own terms even though we have achieved Findependence years ago: more than 30 in your case, seven in ours. One difference is you travel a lot more, while we are content to stay in our Toronto home near Lake Ontario and take just a few weeks abroad, preferably if it’s a business expense. So let me start with the provocative statement that I think travel is expensive and over-rated. I have no doubt you can rebut that!

A&B: First, let us clarify that the time we spend on our website is what we consider to be our volunteer time. Yes, there are products that we sell, but 99% of our information is free because we are passionate about teaching financial literacy to those who want to learn.

In regards to your comment about travel being expensive and over-rated, it depends.

We think that there are differing styles of travel. There are tourists, visitors and travelers. There is no one-right-way to journey around, and we love it that people get out and about, expanding their minds.

Tourists tend to go on vacation for a week or two, spending a good deal of money on lodging, transport, entertainment and meals. Every day must be “perfect” and if the weather doesn’t cooperate or if service is not great, then there is this sense of disappointment. They tend to go to resorts or even exotic locations, but the lodging and amenities have a sense of Disneyland unreality, and are often over-priced.

Sure, there might be a water buffalo in some rice fields, with “workers” wearing a “traditional clothing uniform” but the real locals are miles away. Tourists will pay $10 or more for a beer that the residents of the area would purchase for about a buck.

Also, Tourists might like the idea of a vacation or might not. Mostly, they like the comfort and routine of home, and a vacation is an interruption in their experience of the familiar. Many times, it borders on the feeling that “this is a waste of time. I’d rather be home.” They don’t know any local phrases in a foreign language except maybe Yes, No, Thank you, Bathroom and Beer. Tourists have more of a passive approach to their excursion and want to be entertained. Then they rate their experience with their friends when they return home.

In order to go on this vacation, they stop their mail, perhaps have a house sitter or family member/friend water their plants or watch their pet. They have probably cleaned out their refrigerator and have to stock up once again when they return home. And it all seems to be a hassle. “Would have been easier to just stay at home in the first place. Plus, now we have this credit card bill and all these souvenirs to give to friends.”

Visitors on the other hand stay in a location for a bit longer – maybe even a month or so. They know some survival phrases in the local language and choose lodging that is more middle range than a resort option. About half the time, they will eat outside of big chain restaurants with well-known names and take a chance on a local restaurant.

They are a bit more self-guided in their entertainment choices, perhaps utilizing Google maps or a local tour of the area to become familiar with their surroundings. They may select local transportation or hire a driver to go from archaeological ruins and museums or they might take a self-directed walking tour.

Using a daypack, they bring their own drinking water and perhaps some snacks to munch on as they go from place to place in their day.

Traveling for them is not necessarily a “vacation” but more of an experience, or a sabbatical. They could take cooking classes, language classes, painting courses and the like and they interact with the local people.

After their time away from home, their lives have altered in some way, perhaps expanding their perspectives or dropping an outworn routine. They look forward to their next adventure.

Then you have Travelers.

Billy and Akaisha at Chacala Beach, Nayarit, Mexico

These are the people who go from place-to-place with no itinerary other than their own style of meandering. They usually buy only one-way tickets, figuring out how to return – if they do – at another time. They communicate with the native inhabitants in their own language, purchase food, clothing and travel equipment from markets in the area and will often eat street food or dine in local restaurants.

These people travel for months, sometimes years at a time and rent apart-hotels, AirBnBs, house sit or bargain for a hotel room for a monthly rate. They may or may not have a home base for when they return from their wandering.

Travelers are more flexible mentally and are willing to have their routines interrupted. If the weather pattern is not to their liking, they might move on, or hunker down till the cold, heat, or rain stops. They do not live their traveling life as in “Today is Tuesday so it must be Belgium.” They speak with other travelers to get insight into their possible next stop.

Travelers employ digital equipment and apps to communicate with family and friends. They utilize email, sending digital photos or videos taken of their experiences, and they travel lightly. They throw their daypacks onto a bus or carry them on an affordable inter-country flight. Getting their cash in the currency of the country they are living in, they work the ATMs with a debit card that pays the withdrawal fee back.

They manage their lives online and have been receiving paperless mail for a long time. Photos are placed up in the cloud and they take care of business via Skype, WhatsApp or Signal, benefitting from medical tourism for their health care.

Travel does not cost them “more.” In fact, if they were spending their time “at home” they would still have a baseline of expenses – lodging, food, transport, entertainment for instance. But now they have incorporated these same expenses along with globe-trotting which creates memories for a lifetime and stories to share.

In general, travel has broadened their minds, giving them a unique perspective of the world and a confidence and self-reliance that pervades daily living.

We think it’s important to know one’s traveling style and enjoy who you are. There is not a one-size-fits-all, and we recognize that travel isn’t for everyone.

Someone has to stay home, attend the roses and mow the lawn!

Hub CFO Jonathan Chevreau

How does extensive travel differ from short vacations from full-time employment?

JC Q2: To clarify, we enjoy travel too; was just playing devil’s advocate. Before we switch to Findependence, do you think there’s a big difference between the expensive two-week vacations many salaried employees take, and actually renting a house or suite abroad for 3 or 4 months at a time in Semi-retirement?

A&B: Yes, there is a big difference, actually.

When one is still working, vacations are stress busters. Work hard, play hard.

These holidays tend to be results of pent up demand for luxury; things we have denied ourselves during our working life like splurging on fine meals out, visiting an exotic place far from home, a ski vacation, or a safari. Continue Reading…

While most business executives are and should be approaching Financial Independence, there is a little-known threat to their financial well-being: addiction/substance abuse.

In fact, according to the SAMHSA [Substance Abuse and Mental Health Services Administration], around 11.4% of management employees (example business executives and managers) are diagnosed with a Substance Use Disorder every year.

If the addiction is not managed in a timely fashion, abrupt dismissal could torpedo any long-term goals for financial freedom.

As an aspiring business executive or someone who is serious about their financial education, it’s good to be aware of addiction and its possible ramifications.

So in this post, we look at why business execs should take addictions seriously. We also discuss different treatment options available for business executives to overcome SUD.

Help is Available

Anyone can suffer from drug addiction, including those in white-collar, executive positions who juggle a lot of responsibilities. In fact, it could be more difficult for them as they may be tempted to avoid/delay treatment so their career or work doesn’t suffer due to the required time off.

That’s where executive addiction-related treatment centers come in. These treatment centers are equipped with high-end tools, services, and necessary amenities so that patients can maintain active personal and professional lives while also achieving sobriety.

Often the main highlight of these programs is the luxury setting and amenities given to the professionals and a distraction-free comfortable environment.

Addiction Treatments available for Business Executives

Medical Detox

Often the first phase of most recovery programs; medical detox aims at the cessation of drug usage. In the absence of medical aid, the patient may experience myriad unpleasant withdrawal symptoms.

Executive treatment facilities, such as detox centers in California, deploy safe and medical procedures to make the detox process as comfortable and less painful as possible.

Psychotherapy

Often the therapeutic phase of the program begins right after the detox is successfully over. Inpatient rehab centers in Los Angeles for example, use it in individual and group settings. Psychotherapy mainly aims to recognize the psychological reasons that are causing or triggering the drug usage.

After that, it teaches several relapse prevention mechanisms and coping techniques to deal with tough situations without resorting to drugs. Continue Reading…

Returns on the traditional 60% stocks/40% bonds balanced portfolio are expected to be roughly half of what investors realized over the last decade, according to the Vanguard Group’s 2022 Economic and Market Outlook, which is being released today (Monday, Dec. 13).

Global stocks are expected to outperform U.S. stocks bonds significantly over the next ten years while US and global bonds will be in the range of 1.3% to 2.4% annualized ,

Here are Vanguard’s 10-year annualized return projections:

Global equities: 5.2% – 7.2%

U.S. equities: 2.3% – 4.3%

Global bonds: 1.3% – 2.3%

U.S. bonds: 1.4%– 2.4%

The report issued by Valley Forge, PA-based Vanguard is titled Striking a better balance: ironic given its projections for performance of balanced portfolios.

“The road ahead for investors promises to be a challenging one,” said Joe Davis, Vanguard’s global chief economist and co-author of the report. “Global markets will test investors’ discipline as they navigate the risks of unwinding monetary policy support, slower growth, and rising real rates.”

In an advance webinar aired last Thursday, Davis said: “Wage inflation will dictates the pace of rate hikes in 2022.” He said the US Federal reserve is likely to raise rates to at least 2.5% this cycle in order to maintain price stability. As for stocks, we are in an era of “high valuations and low rates,” which creates a “fragile backdrop for markets ….[which] will chip away at future returns.” Better valuations are in developed markets outside the US, small-caps and Value. More stretched valuations are in Emerging Markets, the US, Growth and Large-cap, Davis said.

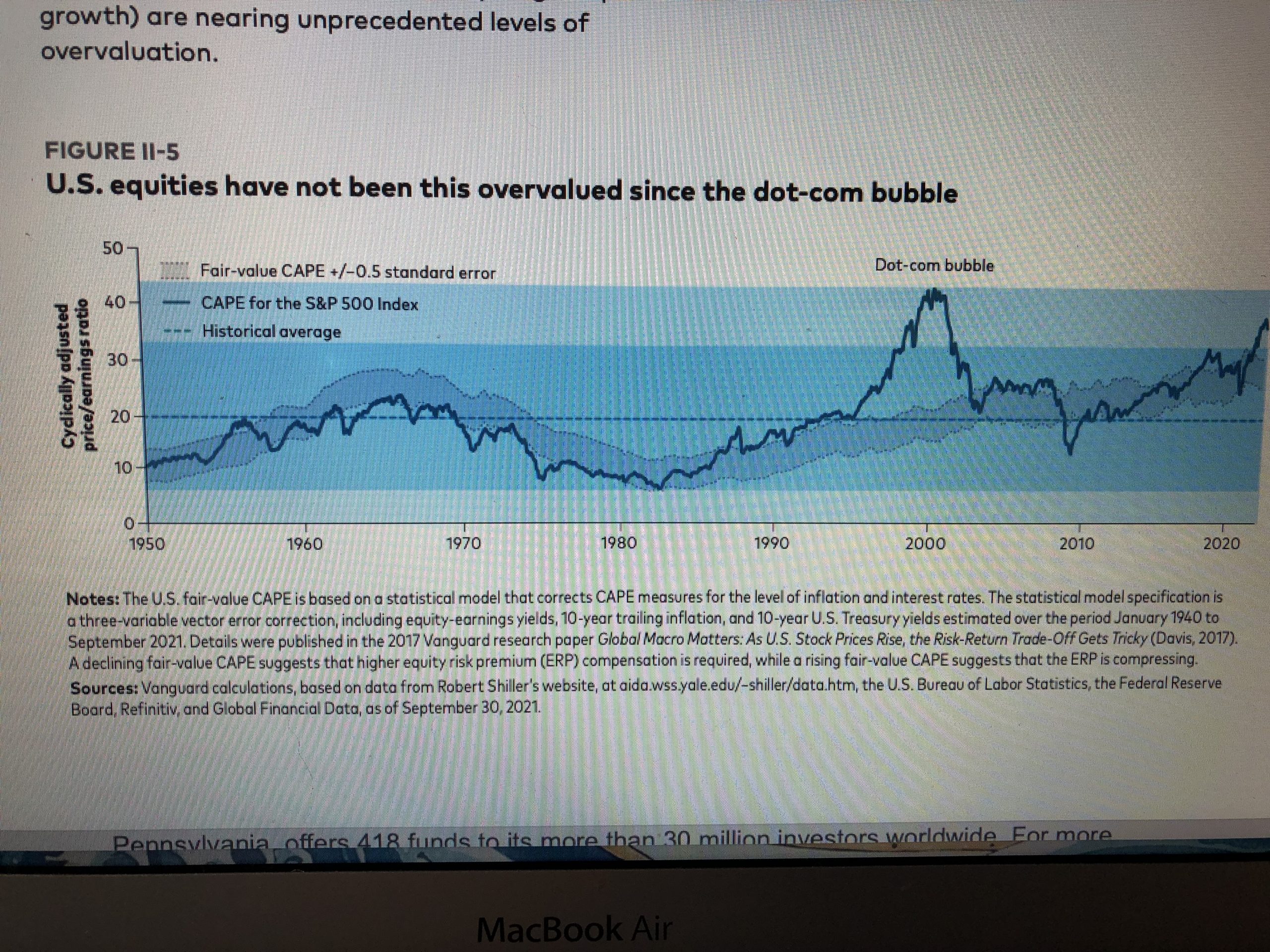

US equities have not been this overvalued since the dot-com bubble, Davis said, adding that a secular decline in rates has been three decades in the marking.

For Bond markets, best values is in TIPS and short-term treasuries. Most stretched are long-term treasuries, mortgage backed securities and international credit. In between are intermediate treasures and high-yield bonds.

Policy accommodations

In Monday’s press release, Vanguard said challenges are likely to be most evident with the unwind of monetary policy, a critical factor in 2022 as central bankers assess a rapidly evolving economic landscape. Inflationary pressures have sharpened the focus on monetary policymakers as these pressures may drive changes in central bank communications and actions. Vanguard projects that central banks will largely try to avoid sharp and unexpected shifts in the timing of policy changes, particularly of policy rate increases, but that conditions will force them to act in 2022 and quite possibly by more than markets are anticipating.

Economic outlook

With the global economic recovery expected to continue in 2022, Vanguard economists foresee the low-hanging fruit of rebounding activity to give way to slower growth, regardless of supply- chain dynamics. In both the U.S. and the Euro area, Vanguard expects economic growth to normalize to 4%. In the U.K., Vanguard expects growth of about 5.5%, and in China, expectations are that growth will fall to about 5%.

Inflation

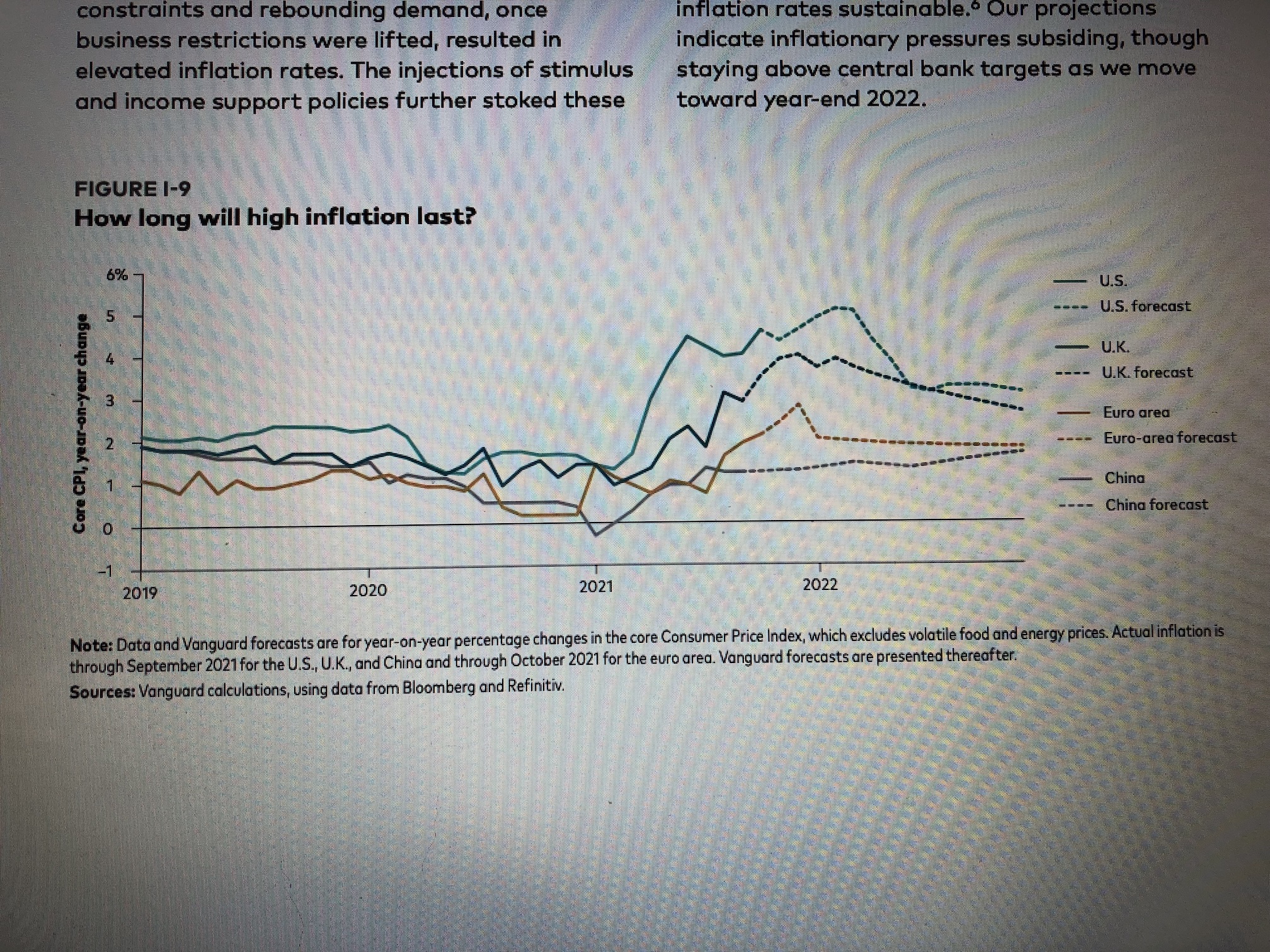

Vanguard expects labor markets will continue to tighten, with several major economies quickly approaching full employment. Vanguard estimates the cyclical effects of supply constraints will persist well into early 2022 and then normalize as the structural deflationary forces of technology and unemployment take hold again. These factors contribute to expectations that inflation will trend higher for some time before slowing in the second half of 2022.

Don’t fear a “lost decade” for US stocks but a lower-return one

Vanguard’s long-term outlook for global asset returns for 2022 and beyond remains guarded, particularly for equities where valuations are high and low real interest rates continue to act as a strong gravitational pull on future returns. Investors should not fear a “lost decade” for U.S. stocks, but rather, a lower-return one, it says. For fixed income, low interest rates mean investors should expect lower returns. However, because rates have risen modestly since 2020, Vanguard’s outlook is commensurately higher.

International equities will outperform US in coming decades

Given the differences in valuations between the U.S. and non-U.S. developed markets, Vanguard projects international equities will outperform U.S. equities in the coming decades and value stocks will outperform growth in the U.S.

It says investors are best served in a broadly-diversified portfolio, including international equities.

“While the economic recovery is expected to continue through 2022, easy gains in growth from rebounding activity are behind us, and policy will replace health as the leading consideration for investors,” Davis said, “Despite a potential low-return environment, we are still expecting a positive premium for bearing equity risk. Investors should continue to focus on what they can control, and if they have the patience to weather potential periods of underperformance, we believe accepting some active risk offers the opportunity to offset low future returns.”

Inflation: Transitory with a Twist

At the advance webinar, Vanguard America’s Senior Economist Roger Aliaga-Diaz projects inflation to be “Transitory with a Twist.” He foresees only a modest decline in inflation in 2022. Central banks, including the Fed, will have to normalize sooner than later. “We may see next week [i.e. this week: Dec. 13 to Dec 17] accelerating tapering but not likely to hike rates.” He expects “one or two” hikes in the second half of 2022. Inflation will be around 5% early in 2022 but this should be in the low 3s by the end of 2022. Continue Reading…