By Mike Brown

By Mike Brown

Special to the Financial Independence Hub

LendEDU’s fourth annual lottery spending report analyzed the most recent U.S. Census data to see what the average American is spending on the lottery, which states spend the most, and how each state spends its yearly lottery revenue.

In the United States, the lottery offers one of the quickest routes to the American Dream; for just a few dollars, you could become a multi-millionaire in a matter of minutes.

Yet, the odds of that happening are incredibly slim, and the money spent on lottery tickets can quickly become substantial.

For the last three years, LendEDU has analyzed U.S. Census Bureau data on annual lottery spending by state to find how much the average American spends, in addition to each state’s lottery expenditure per capita.

Our fourth annual lottery spending report brings you those same statistics and some new ones. This year, we also broke down how each state spends its annual lottery revenue and what each state’s lottery expenditure per capita is as a percentage of its median household income.

Average Lottery Spending by Americans Hits Recent High

The U.S. Census Bureau releases its lottery spending data on a two-year lag, so the data that was released on January 31, 2020 reflects lottery spending data from 2018.

The U.S. Census Bureau releases its lottery spending data on a two-year lag, so the data that was released on January 31, 2020 reflects lottery spending data from 2018.

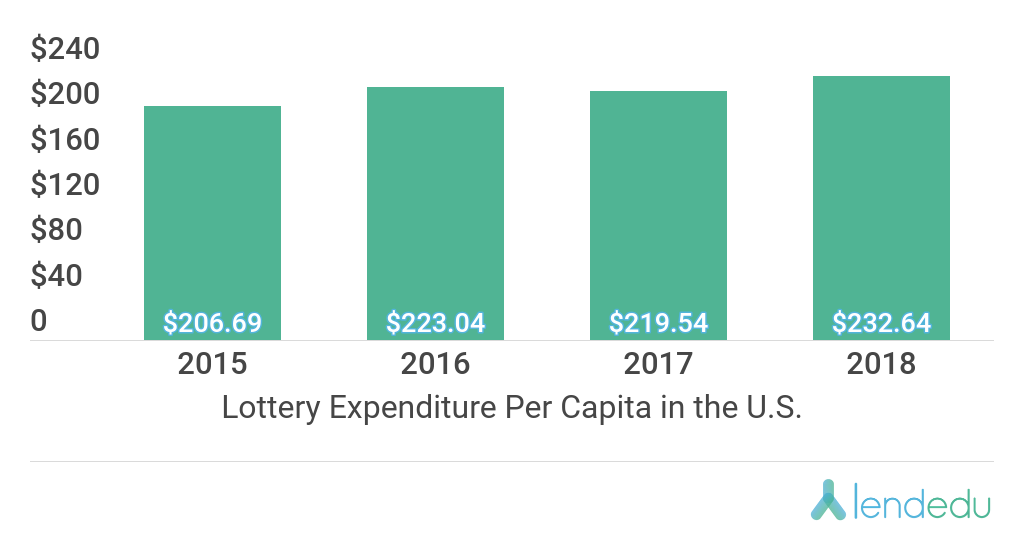

Since LendEDU started doing this report, lottery spending per capita in the U.S. hit a recent high in 2018.

In 2018, Americans spent a combined $76,362,627,000 on the lottery, while the most recent U.S. population estimate from the Census is 328,239,523.

This puts the lottery expenditure per capita in the U.S. at $232.64, which is up $13.10 compared to 2017’s figure.

Massachusetts spends the most on the Lottery

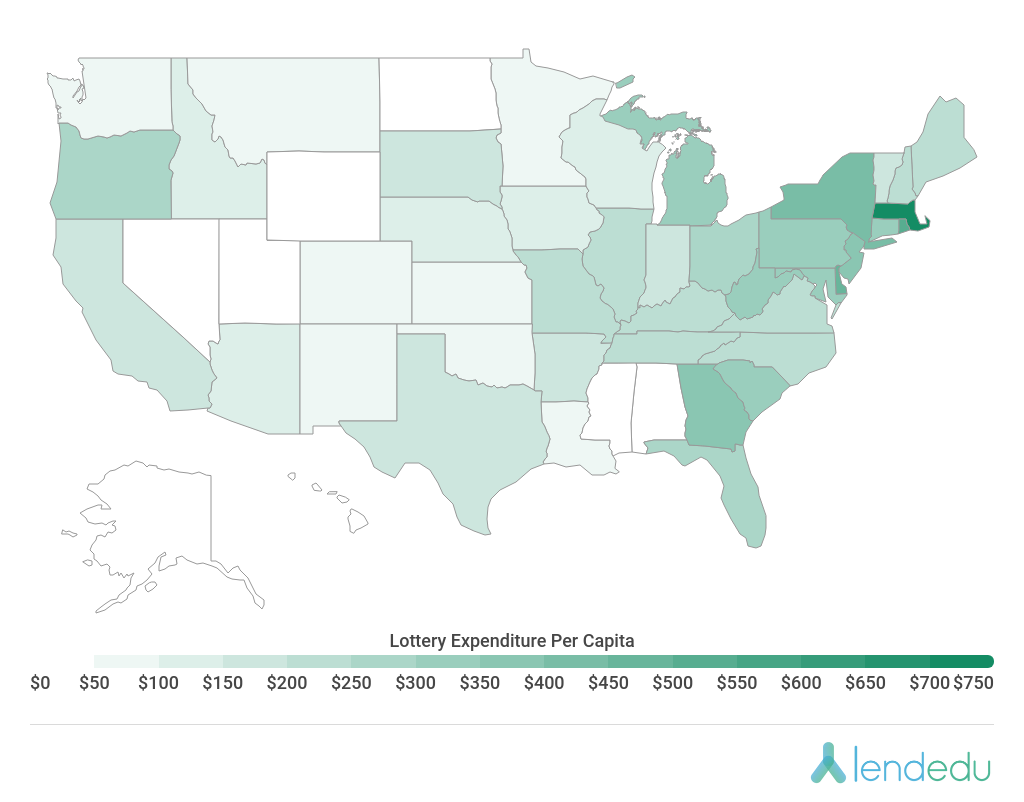

By taking each state’s total lottery expenditure from 2018 and dividing it by the most recent population estimate, we put together a map that breaks down state lottery spending per capita.

And once again, lottery players from Massachusetts spent the most on the lottery in 2018, $765.90. This figure is up from the state’s number from last year, $737.01. In comparison, North Dakota once again had the lowest expenditure per capita, going from $34.68 in 2017 to $30.32 in 2018.

For reference, six states do not offer a lottery: Alabama, Alaska, Hawaii, Mississippi, Nevada, and Utah. Washington D.C. does offer a lottery but does not report any official figures to the U.S. Census Bureau, therefore they have been excluded from this report.

State-by-State Lottery Expenditure Per Capita From 2016 to 2018

Below, you will see how each state’s lottery expenditure per capita has changed from 2016 to 2018 according to each state’s lottery revenue and population from each year. Continue Reading…