By Ahmed Farooq, Franklin Templeton Canada

By Ahmed Farooq, Franklin Templeton Canada

(Sponsor Content)

Many advisors I speak with continue to struggle with the increasing complexities of today’s fixed-income environment and are looking for guidance. The combination of interest rate fluctuations, inflation threats, trade tensions and political upheavals is a challenging environment to make the right call for their clients’ portfolios. There is a real concern that volatility is on the horizon and fixed-income mandates will be needed to provide that cushioning to the overall portfolio.

Active management may be the best way for advisors to navigate this market. For advisors who want an expert’s opinion when it comes to managing future interest rates, credit quality or duration calls in their fixed-income allocation, I like to remind them that this is something that may be best left to a manger who can effectively deal with these factors and risks.

The trend towards active continues

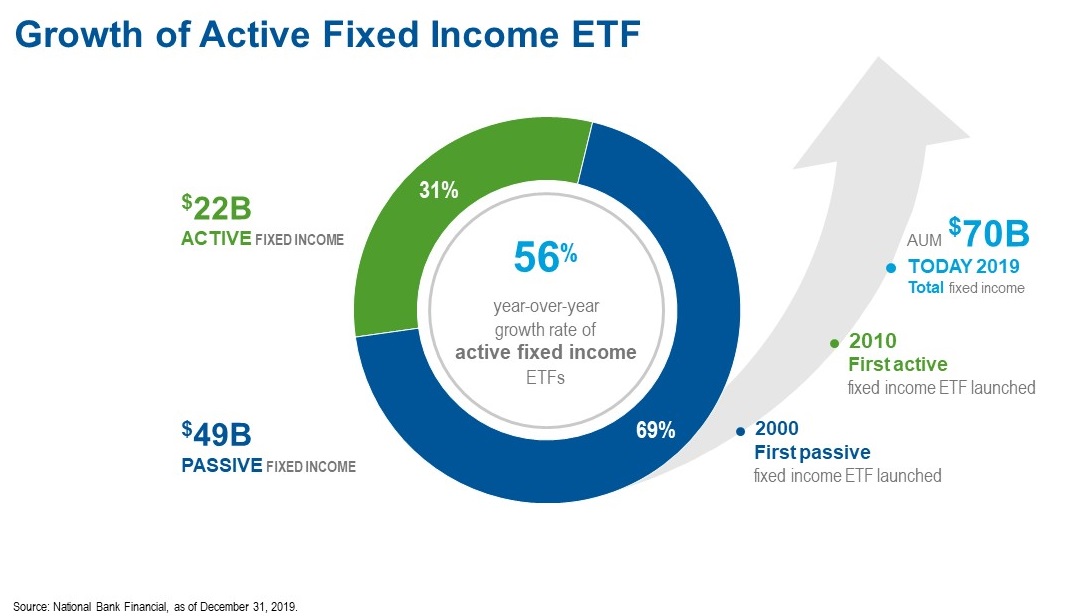

This trend of more advisors switching to actively managed fixed income solutions can be seen in monthly ETF inflow reports over this past year. Within the world of fixed-income ETFs, actively managed products have seen the biggest area of growth. For example, National Bank of Canada’s January 2020 ETF Research & Strategy Report showed that at the end of January, the total AUM of fixed-income ETFs was $73.4 billion in Canada. Of that $22 billion was put into actively managed funds, which now amounts to nearly a third of all fixed-income ETFs.

Active strategies seek to achieve a specific investment outcome

The goal of passive indexing strategies is to minimize tracking error to the index, maintain index exposure by either fully replicating the index or though a stratified sampling approach; one thing a passive investment cannot do is adjust to any type of market events. This can certainly be a headache for most advisors as the onus on making any changes to their portfolio will be on them. Further, with the vast number of options available, this headache is something that cannot be easily solved. Active managers can adjust to different type of market events, changes to monetary policy and yield curve, adjustment from geopolitical events, and duration management. Outsourcing your fixed income exposure to align with your client’s outcomes will provide relief in this ever-tougher fixed income environment.

Improving client portfolios

As more advisors look at their options within the active fixed income space, I think they will be pleasantly surprised by the pricing of active fixed income funds. Continue Reading…