By Dale Roberts

By Dale RobertsIn October I penned this blog post, The Balanced Growth Portfolio. The Investor’s Sweet Spot. A Balanced Growth model with typically be in the area of 70-80% in stocks and the remainder in bonds. It’s a growth portfolio, but with a modest allocation to bonds to reduce the price risks. As I often write, those bonds work like shock absorbers through market volatility or market corrections. They help smooth out the ride.

I’d call this model the sweet spot as it might offer the best balance of very good total return potential with less risk compared to an all-stock portfolio. It many periods it will deliver the best risk-adjusted returns.

In fact, in many periods the Balanced Growth portfolio model can deliver the same returns as an all-stock model, while taking on less risk. Stock market corrections become the great equalizer. The pure equity model will certainly outperform in a long bull market run, but then the stock market corrections come along and bring the stocks down to earth while the Balanced Growth model then moves into the lead. They might play a game of tortoise and the hare for many years or decades.

See my above post link for charts on that comparison.

Let’s look at the ETF holdings of Canadians

Industry statistics are published by the Canadian ETF Association. You can access the December 2018 report and commentary here.

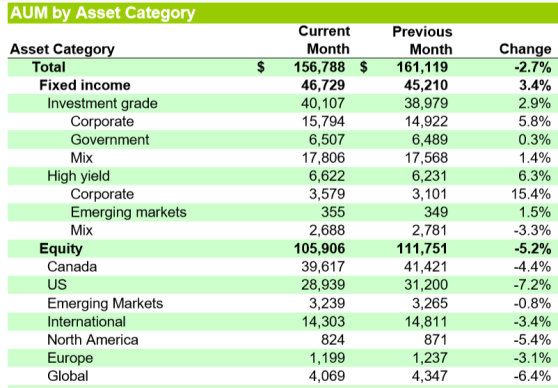

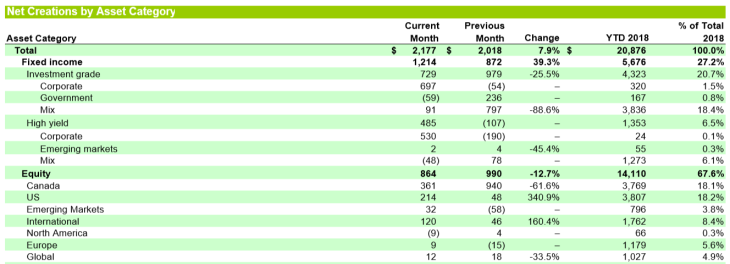

The chart at the top of this blog shows the monthly breakdown of assets held in ETFs. Current Month is month’s end December 2018, Previous Month is November, of course. Keep in mind that the assets will be affected by the total inflows and outflows (purchases and sells) and also the market variance. The stock markets fell in December and that will bring down the total stock assets number.

We see that Canadian ETF investors are in that sweet spot of near 70% equities and 30% bonds. And the good news is that while the stock markets were pulling their little December hissy fit, investors were adding new monies to their ETFs: both Fixed Income and Equities. And you’ll see that Canadian ETF investors are acquiring within the Balanced Growth band.

We see that investors did respond to the stock market price risks and moved more monies into the fixed income side of the ledger in December. No problem there. Sometimes Mr. Market gives us a little love tap and reminds us that markets can go down in a hurry. We get a very considerate warning shot across the bow. On that here’s my Seeking Alpha article from one year ago Mr. Volatility is Asking You, Taunting You – So You Wanna Go?

Many of us might be getting a little flabby with respect to our risk taking ability. We have not been tested much in the last decade coming out of the Great Recession. We should always remember that markets can be volatile and they can fall by some 30%, 40% or 50% or more in a major market correction. I reminded readers of those risks in my first post to the Tangerine Forward Thinking blog with Why You Might Still Want Bonds In Your Investment Portfolio.

Ensure that you know your risk tolerance level and that your portfolio is best matched to you risk tolerance level. Have a more than solid investment plan but consider that emotional risk. From that Seeking Alpha article and offered by the most ferocious heavyweight boxer of all time, Mike Tyson …

Everyone has a plan until I punch them in the face.

Yes, Mr. Market may punch you in the face one day. Are you ready? I can take a punch in the market and in the boxing ring. I grew up with a boxing ring in the backyard so that my older brother could practice punching someone in the face as he prepared for and kept in fighting shape for playing Junior ‘hockey’. He only ever lost one hockey fight. Me and my face take full credit. Mr. Market has thrown a few punches too.

All said, be prepared.

How are Robo-Advised Canadians putting monies to work?

Keep in mind that many investors will create their own ETF Model Portfolios through their discount brokerage. But of course there’s a massive move to the Canadian Robo Advisors, where investors can access digital and human advice that will then lead to the recommendation of risk-appropriate ETF portfolios. That risk assessment is key. Continue Reading…