Some investment rules of thumb will help your portfolio, while others will cost you money. Here’s how to tell the difference.

TSInetwork.ca

You can find numerous investment rules of thumb that aim to tell you when to buy or sell. Most are based on chart-reading or technical analysis. All these work at times, but none work consistently. When they fail, the profits you miss out on are likely to overwhelm any risk they help you avoid.

Meanwhile, one of the top investment rules of thumb — that does work — is that you can cut way down on times when you really need to sell by consistently buying well-established, high-quality stocks.

These stocks can still drop sharply when the economy falters or bad news strikes, of course. But these are the stocks that snap back quickest and most reliably when the trend reverses and bad news comes less often. That’s why it generally pays to hold on to stocks like these through market setbacks.

Here are successful investment rules of thumb to help bring profits to your portfolio

Avoid portfolio tinkering, especially when it comes to selling stocks that have gone up too far and too fast

Diversify across industry sectors

Avoid buying too many stocks in the broker/media limelight

Build a balanced portfolio

Utilize proven strategies for compound interest

Keep fees low with traditional ETF picks

Look for hidden assets

Look for dividend-paying stocks

One of the best investment rules of thumb is to stay out of new stock issues

Companies sell new issues (also called Initial Public Offerings, or IPOs) to the public when they feel it’s a good time to sell. That may not be, and often isn’t, a good time for you to buy.

In addition, the underwriting brokerage firms try to spark publicity about the new issue, and they pay extra commission (as much as double the regular rates) to spur their salespeople to sell the new issue to their clients. This tends to create a high-water mark in the price of the new issue. Unless the new company can follow up with business success, the price of the new issue may languish for months or years.

Some new stock issues — so-called “hot new issues” — depart from this pattern. They begin moving up as soon as they hit the market. Some even “gap upward” on their first day of trading: that is, their first public trading takes place well above the new issue price.

This possibility attracts buyers who fail to appreciate how rare it is. In addition, the underwriting brokers can generally tell when this is going to happen, by judging the reaction of their biggest clients (who of course get first pick on their new issues), and the media. They reserve most of their allotments of hot new issues to their biggest and best clients. Continue Reading…

Investing in Exchange-Traded Funds (ETFs) can be a smart move for many investors, but it’s crucial to have a clear understanding of the costs and fees associated with these investment vehicles. In this blog post, we will decode the various expenses and provide valuable insights to help you make informed decisions.

Expense Ratio: Unveiling the Components

The expense ratio is a fundamental factor to consider when evaluating ETF costs. It encompasses several elements, including:

Management fees: ETFs charge management fees for the professional management of the fund.

Operating expenses: These expenses cover administrative costs, custody fees, and legal fees.

Trading costs: ETFs incur costs associated with buying and selling the underlying assets that make up the fund.

Taxes: ETFs may also be subject to taxes including, interest, dividend, and capital gains taxes, which are passed on to investors.

The expense ratio is typically expressed as an annual percentage of the total assets under management (AUM) and is deducted from the ETF’s net asset value (NAV). For instance, if an ETF has an expense ratio of 0.50% and an NAV per unit of $100, the annual cost to investors would amount to $0.50/unit.

Exploring Other Cost Considerations

Tracking Error: Although ETFs aim to replicate the performance of an underlying index or asset class, certain factors such as fees, market conditions, market timing, currency, and tracking methodology can lead to a difference between the ETF’s returns and the index it tracks. This disparity is known as tracking error.

Bid-Ask Spread: The bid-ask spread represents the difference between the highest price a buyer is willing to pay and the lowest price a seller is willing to accept for an ETF. Liquidity, market conditions, ETF characteristics, trading volume, and market maker activity influence the bid-ask spread. Narrower spreads are generally observed with higher liquidity and trading volumes, while wider spreads are prevalent with lower volumes and niche markets. Investors should consider bid-ask spreads, as they can affect transaction costs and overall investment returns. To mitigate these costs, investors can use limit orders to specify their desired price and potentially minimize the impact of wider spreads.

Currency Hedging: ETFs provide easy access to assets from different regions worldwide. Investing in non-Canadian assets expose investors to two potential sources of return: the return of the security and the return of the foreign currency relative to the Canadian dollar (CAD). Currency fluctuations can have either a positive or negative impact on your total return. Currency-hedged ETF solutions are available and aim to mitigate the impact of currency fluctuations, allowing investors to participate in global markets as if they were local. It is important to understand however, that there is a cost for currency hedging. At BMO ETFs this cost is minimal as we use forward currency contracts to hedge purposes which are very cost effective. Continue Reading…

An Interview with Brian Watkins by Billy and Akaisha Kaderli, RetireEarlyLifestyle.com

Special to Financial Independence Hub

We at RetireEarlyLifestyle love to bring you retirement stories of people we have met. There’s no one right way to get to Financial Independence, and we are happy to bring Brian’s adventure to financial freedom to you.

Thank you, Brian, for taking the time to answer all our questions!

Brian Watkins enjoying his last year of teaching

Retire Early Lifestyle: Could you tell us a little about yourself, and how old you are?

Brian Watkins: Hi, as of 14 months ago I quit my job as a teacher, a position I held for 22 years, and at 48 decided to travel and enjoy a different lifestyle. I wanted a life with more freedom and less obligation to debt. I had spent a lifetime accepting that debt was part of the American lifestyle and just wanted something different.

REL: What got you started investing and when?

BW: In my very first year of teaching, I was broke and struggling from month to month. At work I saw sign that read “Free Pizza….. in the Library.” Not sure what the rest of the sign said but I was down with free pizza, so I headed to the library. Little did I know that with a slice came some financial advice. By the time I left I was investing $100 a month in a 403B and only going to see a $70 difference in my check. The lesson: live on less and invest!

REL: When did you know you were ready to retire and what motivated you?

BW: At 46 both my mother and father passed within six months of each other. I really didn’t want to risk working till death. So at that point I started working on my exit plan.

REL: What do you do for income generation?

BW: When I turn 55 I will be eligible to withdraw from my pension. I have a 403B in place that will be eligible at 591/2 and I currently live off the sale of my condo. My overall goal has been to live off 4% of my total investments.

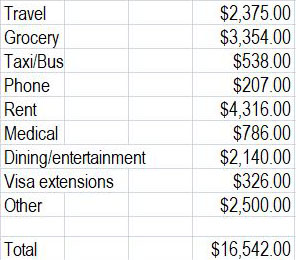

REL: What do you plan to budget annually for your retirement?

BW: I had an educated idea of what my expenses might be but purchasing your book and tracking my expenses helped me more than you’ll ever know. In my first 12 months I spent $16,542. Eight months of that was for two people. My annual budget broke down as follows:

REL: Can you share with us anything about how your portfolio is structured?

BW: My current portfolio is 75% equities, 25% bonds.

Puerto Galera, Philippines

REL: You are one of the new generation of Early Retirees who are well versed in a digital lifestyle. How have you used this technology to enhance your retirement?

BW: I have actually learned so much from the retirees who are digitally inclined. I use a Virtual Private Network (VPN) for those countries IP address that my bank blocks. I have a Google voice number so that I can call (or text) a U.S. number from Google Hangouts using wifi only.

The most important people to me have the Cash App and I can send or receive money on it and have it deposited for free (3 day waiting period) or for a fee same day. Continue Reading…

Our firm is a tax boutique with all kinds of clients and all kinds of tax issues. They may be corporations, individuals of high net worth, business people, and entrepreneurs running smaller enterprises. They can also be retired professionals.

One of our clients is a retired doctor from Alberta who owns several Canadian properties. He moved from Alberta to Ontario so he could be close to his sister, but he still owns that property in Western Canada. However, the Canada Revenue Agency is not satisfied that his Ontario residence is his primary residence – it is – and demands back taxes.

Unfortunately, the CRA often takes the view that one is guilty until proven innocent, which is why so many people require professionals like lawyers and accountants to help them in their tax dealings with the federal government.

We also have clients with stories that are heart-breaking. And make no mistake, the CRA is anything but a purveyor of mercy when it comes to taxes. It doesn’t matter if you are a multi-millionaire or a single mother with kids whom they deem to be in tax arrears.

Regardless who you are and your particular situation, one thing everyone has in common is that no one wants to be audited. According to the CRA’s Annual Report to Parliament, in fiscal year 2020-2021 the agency conducted 245,000 audits of individual tax returns and another 41,000 audits of small- and medium-sized businesses. Generally speaking, the CRA can only audit someone up to four years after a tax return has been filed. However, in some cases — such as in suspected fraud or misrepresentation — the CRA can go farther back and, in fact, there is no time limit for such a re-assessment.

Of course, many of our clients are self-employed, but as mentioned we also represent professionals and businesses who are required to keep their own books, as well as clients who operate other cash-based businesses. It just so happens that these groups are usually audited more often than others. So, if you belong to a group that is already under some scrutiny, it’s important to audit-proof your business.

How do you do that?

Indeed, one of the most common questions we get asked is “How do we avoid audits by the CRA in the future?” Well, there is no simple way. It’s not like taking a pill. But I have compiled a list of ten tips that should help you to remain audit-proof. Let’s have a look at them:

Check and double-check your return after you complete it. This is especially true if you do the return yourself. Keep in mind where this return goes. It goes to the Canada Revenue Agency. If they discover a mistake – even if it’s an honest mistake on your part – they may conclude it was done for a reason. I have many examples of well-documented transactions being rejected due to the taxpayer’s failure to file a routine election. This is why it’s better to avoid mistakes as much as possible.

Keep detailed records. I cannot stress this enough. The fact is some expenses and deductions are audited more than others. I had a client recently who was reassessed vehicle benefits because he didn’t have a log book. It was a huge headache, but we got him his relief. Ensure that you keep meticulous records of all these expenses.

Make a point of filing correctly the first time. Amended returns can and often do draw scrutiny to your filing position. I have seen people forget to report a sizeable deduction. Once it was reported on an amended T2, the CRA conducted a full-scale audit. And this is a large public corporation.

Properly document any unusual changes to your filing position. What exactly does that mean? If you are suddenly earning double the income from one year to the next, or you are claiming an unusual capital expense, do not be afraid to explain it in your return.

Try not to claim unrealistic deductions. Home office expenses, especially these days in the post-Covid world, are often claimed. But if you are claiming half of all your home expenses, you may be audited. Likewise, if you ascribe 100% business use to a vehicle, you may be audited for that.

As much as possible, try to fly under the radar. In other words, do not make it easy for the CRA to single you out as a person or business that should be audited. Examples of not doing this could be things like excessive charitable donations, very low income while living in a mansion, or participating in tax shelters. All of these will raise red flags that may result in an audit.

File on time. This is pretty basic, but you would be surprised how many people and businesses file late. There really is no excuse not to comply. Late returns are never a good idea and opening the door to a potential audit is only one of the reasons to avoid doing this. It is always better to file on time. Continue Reading…

Investing in Dividend Kings (aka Dividend Aristocrats) has come back into style again in as we approach the mid-way point of 2023. After a decade of cheap money-fuelled growth for unprofitable tech stocks the market has now clearly shifted toward the free cash flow darlings that I prefer.Click here to jump directly to my 2023 picks.

After the first few months of 2023, the Canadian market has continued to quietly chug along relative to the more volatile numbers seen in much of the world. For dividend-focused investors, the day-to-day market gyrations are irrelevant.

Reliable (if small) long-term stock appreciation, combined with juicy dividends, are why Canadian dividend kings hold a sacred place in my portfolio. We may very well be in a “sideways” market for a while, and in that situation, holding stocks that spin off gobs of dividend cash is an excellent way to position oneself.

While it looks like inflationary pressures are beginning to ease, top line revenue numbers continue to look good for the vast majority of Canada’s dividend all stars. Real returns though are dependent on profit margins and the ability to keep costs controlled. So far so good for the major Canadian blue chippers on this dividend kings list.

With most of Canada’s best dividend stocks being part of long-time market oligopolies, we see that they have been able to maintain or even grow their profit margins – meaning more profit for shareholders.

With little-to-no news of dividend cuts (or even pauses), dividend-focused investors have likely found it much easier to navigate the stormy market waters relative to growth stock enthusiasts.

Top Canadian Dividend King Pick for 2023: National Bank

Our 2021 top Canadian dividend king pick was Enbridge. I simply felt that given the company’s track record of producing solid returns and rewarding shareholders, the valuation was substantially off.

The stock rewarded me with a capital gain of over 21%, plus the 8.1% dividend (at time of purchase) for an overall return of roughly 29.5%. That compares favorably to the overall return of the TSX (27%) and 25% for CDZ – the Canadian dividend aristocrats ETF.

For 2022 our Canadian dividend king was National Bank (NA).

So… you might be surprised to learn that my Canadian dividend king pick for 2023 is (*drumroll*) National Bank!

Yes – I’m sticking with Canada’s fastest growing bank! I continue to believe in my investing thesis, the market just needs time to bear out the underlying fundamentals. So far so good, as National Bank shares are up nearly 11% year-to-date (and that doesn’t even take into consideration the juicy 4% dividend).

National Bank’s latest quarter earnings report saw a $2.35 EPS, and that represented a strong earnings beat. The Bank’s Canadian operations continue to hold impressive profit margins – and given the strength of Quebec’s regional economy (National Bank’s home base) I don’t see any reason why this won’t continue to be the case.

Out of all the Canadian banks, National bank has been the most generous with its dividend raises over the last 3- and 5-year periods – BUT even with all that dividend generosity, it still has a fairly low payout ratio. That bodes well for the long-term, and certainly means there is no dividend cut in store for 2023.

While Provision for Credit Losses (PCLs) will hold the banks a bit in 2023, I don’t see this as a significant headwind overall. I wrote more about the loan loss provisions that the financial institutions were setting aside in my investing in Canadian bank stocks article.

The banks should continue to benefit from the growing interest rate spreads, and their cautious building of reserves is the exact reason why they are such solid long-term investments.

My insights on National Bank – as well as the 2023 Canadian Dividend Kings list below – are based on my own research, but also relied heavily on the advice and tools provided by Dividend Stocks Rock.

DSR not only provides excellent written advice, but also a ton of free webinars, and ideal tools for analyzing both the Canadian and American dividend markets. Read my DSR review for an in-depth look at just why I’m such a big fan of what fellow Canadian Mike Heroux has put together.

Don’t just take my word for it, see what Mike Heroux has to say about National Bank after the latest round of bank earnings reports in 2023. Mike used to work for National Bank for many years, so if you’re looking for someone that understands all aspects of this company – it’s him!

Dividend Aristocrats and Dividend Kings Offer Stable Growth

In fact, many studies (such as Vanguard) have proven that dividend growers are likely to outperform the market and do it with less volatility. Dividend growers such as the best Canadian dividend aristocrats will continue to increase their dividend in 2023.

Canadian companies with a long history of dividend growth will generally show a strong business model and robust financials. They have gone through many recessions and never stopped increasing dividend payments. In times of confusion and fear, you can go back and look at how companies went through the past crisis and kept their dividend streak alive.

I use the dividend strategy for my leveraged portfolio, a significant portion of my RRSP, and our corporate portfolio. We currently collect a little over $73,000/year in dividends and if you are interested, you can follow my latestdividend update here.

In the past, I’ve written a number of articles on dividend growth stocks, I’ve never properly categorized them. Here are the most common dividend terms as they relate to the U.S. stock market:

A Dividend Achiever is a company that has increased its dividend at least 10 years in a row;

A Dividend Contender is a traded company that has raised dividends for 10 to 24 consecutive years.

A Dividend Champion is a company that has increased its dividend at least 25 years in a row (regardless if it is part of the S&P 500 or not);

A Dividend Aristocrat is a company that is part of the S&P 500 and that has increased its dividend at least 25 years in a row;

A Dividend King is a company that has increased its dividend at least 50 years in a row. The true cream of the crop.

Dividend Aristocrats and Dividend Kings in Canada

Here in Canada, we have a relatively small market and an even smaller list of quality dividend stocks. In a previous article about the top Canadian dividend growth stocks, you will see a number of dividend achievers (10 years+ ), a handful of dividend aristocrats (25 years+), but no dividend kings in Canada (although FTS (48) and CU (49) are getting close).

While I used the terms dividend achievers and dividend aristocrats for the Canadian stock market in the previous section, I must highlight that the official definition of the Canadian dividend aristocrat differs from the one established in the U.S.

In order to be considered as a S&P Canadian Dividend Aristocrat, the company must have increased its dividend payout every year for five years – Therefore, we are looking at stocks that have a good potential for raising its dividend but still pretty far away from 25 consecutive years.

Dividend Kings List

In a few years, we will be able to have a shortlist of Canadian dividend kings (including Fortis and Canadian Utilities). In the meantime, where do we find these elusive dividend kings? You’ll have to look at the biggest market in the world – the US! In the US, there are 30 dividend kings that have increased their dividend at least 50 years in a row. Continue Reading…