Bitcoin continues on the path to greater mainstream acceptance as a core portfolio asset. Last week, Fidelity added modest bitcoin exposure to their all-in-one asset allocation ETFs. The bitcoin weighting is at 1%, 2% or 3% depending on the portfolio risk level. These ETFs might be a way to dip your toe into some bitcoin exposure. You will see the effect over time. Historically it did not take much for bitcoin to have a very positive effect on balanced portfolios. And of course, bitcoin is highly volatile and rebalancing is key. Fidelity is adding bitcoin to balanced portfolios on the Sunday Reads.

Chris Pepper, vice-president of corporate affairs at Fidelity, said that, subject to regulatory approval, the all-in-one balanced fund will have an allocation of approximately 2% to the Bitcoin fund, while the growth fund’s Bitcoin allocation will be around 3%. Fidelity is filing prospectus amendments in the next 10 days, he said.

Of course, this is not advice. Do your own research and decide if you want an allocation to bitcoin. I’m in for the long haul. That said, on Twitter I suggested …

My MoneySense weekly column

In Making Sense of the Markets for the past week we have the earnings season halftime report, inflation is up, up and away, and we’re also building a more recession-resistant portfolio.

Dale Roberts is the Chief Disruptor at cutthecrapinvesting.com. A former ad guy and investment advisor, Dale now helps Canadians say goodbye to paying some of the highest investment fees in the world. This blog originally appeared on Dale’s site on Feb. 13, 2022 and is republished on the Hub with his permission.

My latest MoneySense Retired Money column looks at the dilemma many retirees and would-be retirees face these days: that with sky-high stock prices and interest rates seemingly bottoming and headed up, there’s no such thing as a truly “safe” investment. Click on the highlighted headline for full column: Is the All-Weather portfolio the answer to the shortage of “safe” investments?

Even supposedly safe bonds, bond funds or ETFs largely suffered losses in 2021 as interest rates seemed poised to rise: now that various central banks are starting to hike rates, such pain seems destined to continue in 2022 and beyond.

Yes, short-term bank savings accounts and GICs seem relatively safe from both stock market meltdowns and precipitous rises in interest rates, but then there’s the scourge of inflation. Even if you can get 2% annually from a GIC, if inflation is running at 4%, you’re actually losing 2% a year in real terms.

But what about those Asset Allocation ETFs that have become so popular in recent years. This site and many like it are constantly looking at products like Vanguard’s VBAL (60% stocks to 40% bonds) or similar ETFs from rivals: iShares’ XBAL or BMO’s ZBAL.

The nice feature of Asset Allocation ETFs is the automatic regular rebalancing. If stocks get too elevated, they will eventually plough back some of the gains into the bond allocation, which indeed may be cheaper as rates rise. Conversely, if stocks plummet and the bonds rise in value, the ETFs will snap up more stocks at cheaper prices.

But are these ETFs truly diversified?

True, any one of the above products will own thousands of stocks and bonds from around the world. They are geographically diversified but I’d argue that from an asset class perspective, the focus on stocks and bonds means they are lacking many other possibly non-correlated asset classes: commodities, gold and precious metals, real estate, cryptocurrencies, and inflation-linked bonds to name the major ones.

The Permanent Portfolio and the All-Weather Portfolio

I’ve always kept in mind Harry Browne’s famous Permanent Portfolio, which advocated just four asset classes in four 25% amounts: stocks for prosperity, long-term bonds for deflation, gold for inflation and cash for recessions.

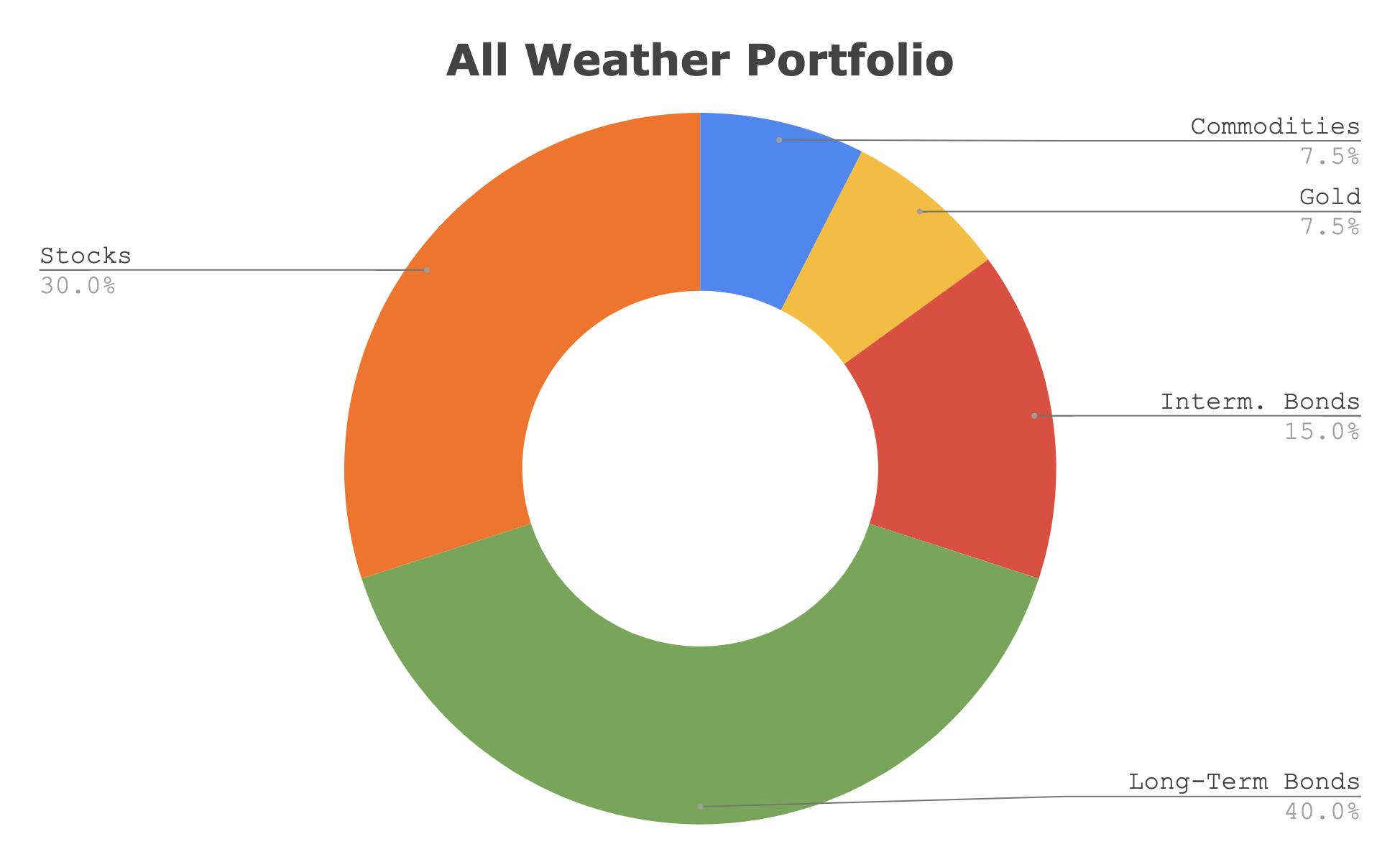

A bit more complicated is the more recent All-Weather portfolio, from American billionaire and author Ray Dalio, founder of Bridgewater Associates. You can find any number of variants of this by googling those words, or videos on YouTube.com. There’s a good book on this, Balanced Asset Allocation (by Alex Shahidi, Wiley), which makes the All-Weather portfolio its starting point. Continue Reading…

Various people have asked me to weigh in on our inflation situation with a particular focus on what central bankers should do about rates going forward.

The ‘what to do’ elements include queries about when to hike, how much, how often and to what end.

I like to use metaphors and the one that fits here is one of having someone you care about climbing a ladder. In this scenario, the ‘friend’ is a mashup of the economy and markets (specifically, both the stock market and the real estate market), the ascension up the ladder is the seeming inexorable climb of prices and valuations, and the decision to tip the ladder over is the decision to raise rates. Here’s the problem …

Let’s say someone you care about is climbing a ladder and you have been given the task of holding the ladder steady, stable, and firmly rooted on the ground while that person climbs. In this case, “price stability” equals “ladder stability.” It’s a tall ladder and conditions are becoming increasingly perilous. As your friend ascends, it eventually becomes clear to you that communication has been lost: your friend is now so far up that they cannot hear your pleas to reverse course. It’s dangerous. You know it, but your friend keeps climbing higher.

Central bankers caught in a dilemma

In this scenario, you know that if you were to tip the ladder over, your friend would be seriously hurt. Conversely, you could do the ‘responsible thing’ and not tip the ladder over, but if you did that and your friend ended up falling from an even higher position, the consequences could be deadly. Central bankers are caught in the horns of a dilemma. Continue Reading…

A quick note to say Happy 2022 to all the Hub’s readers and supporters. We’ll be back to our regular blog-a-day rotation on Tuesday.

In the meantime, I’ll point readers to Dale Roberts’ excellent year-end market wrap for MoneySense, which was published Friday.

Click on the highlighted headline to access, but settle down with a coffee before you do: it’s quite a long read: Making Sense of the Markets: 2021.

It’s a thorough long read that looks at all the major market developments each month in 2021 and you’ll also see a number of prescient market calls made by Dale over the last few years, including an early call on Covid-19 itself, an early call on the Energy and Commodities recovery, and several others.

I’ve followed Dale for some years now: he famously tweets as @67Dodge and I now help edit his weekly MoneySense market wrap, seeing as I became MoneySense’s Investing Editor at Large a few months ago.

In normal years, I would move new money into the TFSA on January 1st but there’s probably no rush this year until Tuesday, Jan. 4, seeing as the Canadian market is closed Monday. (The US will be open that day though).

I’ve not decided exactly what to invest in but it will likely be inflation-related. Going back to Dale Roberts, you can glean a few ideas from his 2021 market wrap: things like short-term TIPS ETFs, or the Purpose Real Assets ETF, or energy/commodity plays.

Personally, I’ve been researching Ray Dalio’s All-Weather portfolio (google it for videos and articles, or try this Seeking Alpha link on it). I’ve concluded that our own family has sufficient US equity exposure but not enough in commodities or TIPS [Treasury Inflation Protected Securities] plays.

Dalio is a bit heavier on fixed-income than most, with a mix of long-term and short-term bonds. His recommended equity exposure is a bit lower, and he suggests 7.5% commodities and 7.5% in gold. Readers may therefore find Friday’s Hub article on gold of interest: A perfect storm for gold.

Every case is different of course. IF I were looking to boost US equity exposure, I’d certainly be considering the new Canadian Depositary Receipts (CDRs), more on which you can read on the Hub early in the new year. If we didn’t already own Berkshire Hathaway, I’d be tempted to add to it with the CDR version of Berkshire, seeing as it pays no dividends and would be a good value counterbalance to high-priced US tech stocks.

So by all means get your $6,000 (if available) into your TFSA early in 2022 but take a few days to figure out how to invest it.

The wild card is certainly Omicron. If you’ve not yet gotten your booster, I highly recommend it.

So again, have a happy, healthy and profitable 2022!

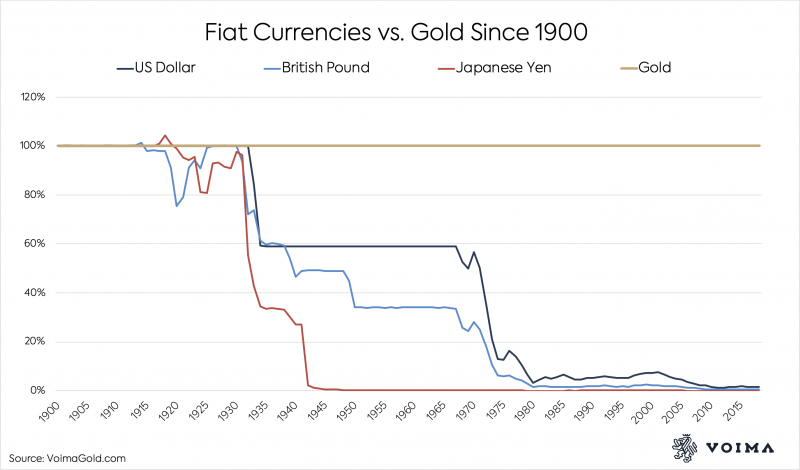

In December 1997, The Financial Times ran an article entitled “The Death of Gold.” Since then, the gold price in US dollars has increased 519% from $288 to $1,780. Today, after many political events and crises we have evidence of the continuous and in many ways spectacular growth of the gold price. This confluence of many current events is creating a perfect storm for gold to increase dramatically more than we imagined.

Currency Devaluation

Typically, currency devaluation is always at the heart of a rising gold price. This has been taking place in all of the major fiat currencies, resulting in an average annual price increase in gold of over 10% since 2000.

“For the naïve there is something miraculous in the issuance of fiat money. A magic word spoken by the government creates out of nothing a thing which can be exchanged against any merchandise a man would like to get. How pale is the art of sorcerers, witches, and conjurors when compared with that of the government’s Treasury Department.” — Ludwig von Mises

Since 1900, all major fiat currencies have been devalued by over 90%.

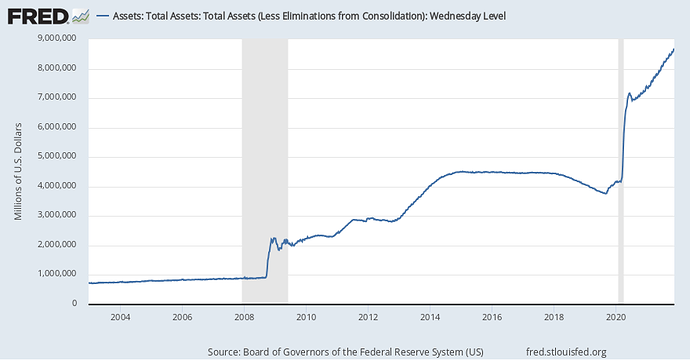

To understand currency devaluation, it is necessary to understand that all currency is created by governments issuing debt and then the central bank monetizing that debt by printing the currency. In 1960, the U.S. federal debt to GDP stood at 52.2%, whereas today it has grown to 125.9%. The Federal Reserve has increased its balance sheet by a historically unprecedented amount of over $7.5 trillion since 2008.

Because of this central bank policy, all western currencies are being devalued and this in turn leads to inflation.

“Nations are not ruined by one act of violence, but gradually and in an almost imperceptible manner by the depreciation of their circulating currency, through excessive quantity.”

— Nicholas Copernicus – 1525

“Fed Chairman Powell has pumped trillions of newly printed dollars into the system in order to prop up the financial markets, but in the process has unleashed a tsunami of inflation that is unlike anything we have seen since the 1970s.” — Michael Snyder

“For the first time in history, ALL the major central banks are printing money. One of two things will occur. If they continue to print, their respective currencies will lose their purchasing power, and we’ll have inflation or even hyper-inflation.”

As Currencies are Devalued, Price Inflation will inevitably follow

Inflation, as this term was always used everywhere and especially in North America, means increasing the quantity of money and bank notes in circulation and the quantity of bank deposits subject to check. But people today use the term ‘inflation’ to refer to the phenomenon that is an inevitable consequence of inflation, and that is the tendency of all prices and wages to rise.

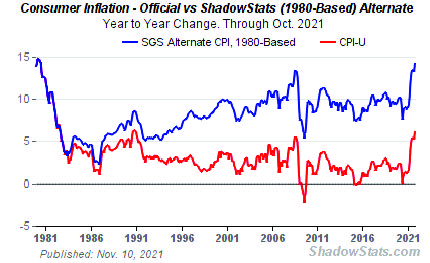

In October 2021, consumer inflation jumped to a four-decade high, the highest since the days of runaway inflation in the early 1980s. Headline year-to-year GDP inflation hit a 38-year-plus high of 4.53%.

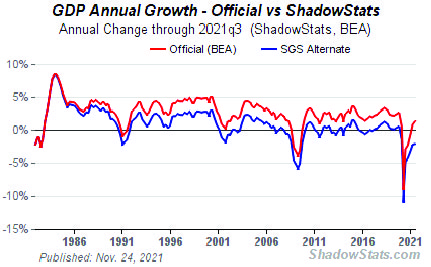

According to John Williams of Shadowstats.com, if inflation was calculated using 1980s methodology, the CPI would be nearly 15%. Since treasury yields are about 2%, the true inflation-adjusted treasury yield would be about -13%.

Gold Rises Fastest When Real Yields Go Negative

Inflation is destined to go even higher in 2022. Many of the biggest corporations have already announced price increases that will take effect in 2022.

Declining GDP — Stagflation

“The…economy is facing a period of stagflation in which both growth and inflation disappoint.” — David Walton, Goldman Sachs

Stagflation is worse than a recession. It’s because stagflation combines the bad economic effects of a recession (stock declines, unemployment increases, housing market dips) with inflated prices. When this is dragged out over the long term, it becomes a problem that can have a big impact on societal habits.

To make matters worse, we are already experiencing declining GDP together with increasing inflation. This is due to an unusual combination of supply chain disruptions and labour shortages due to COVID-19 policies that have been implemented in most western countries.

Supply Chain Disruptions

The COVID-19 pandemic impact and the disruptive government responses continue to have enormous negative impact on global supply chains. Beyond COVID-19, compounding profound governance incompetence, media bias, political conflicts, disintegration of society split by “Covid politics,” natural disasters, cybersecurity breaches, international trade disputes have negatively impacted supply chains leading to product shortages, distribution delays, and manufacturing disruptions. The lockdowns imposed in many countries have led to revenue declines and many bankruptcies, with many more to come. Making matters even worse is the implementation of vaccine mandates, causing over 4 million people to leave the workforce in the U.S. This will lead to other societal problems due to lack of first responders, nurses, firefighters, and police.

Some analysts expect that it will take years for the capacity constraints and backlogs to ease. Continue Reading…

Dale Roberts is the Chief Disruptor at cutthecrapinvesting.com. A former ad guy and investment advisor, Dale now helps Canadians say goodbye to paying some of the highest investment fees in the world. This blog originally appeared on Dale’s site on Feb. 13, 2022 and is republished on the Hub with his permission.

Dale Roberts is the Chief Disruptor at cutthecrapinvesting.com. A former ad guy and investment advisor, Dale now helps Canadians say goodbye to paying some of the highest investment fees in the world. This blog originally appeared on Dale’s site on Feb. 13, 2022 and is republished on the Hub with his permission.