This article has been sponsored by BMO Canada. All opinions are my own.

I’m on record to say that the vast majority of self-directed investors should simply use a single asset allocation ETF to build their investment portfolios.

What’s not to like about asset allocation ETFs? Investors get a low cost, risk appropriate, globally diversified portfolio in one easy to use product. It’s a fresh take on an old idea – the global balanced mutual fund – updated for the 2020’s using low-cost ETFs.

Investors don’t even have to worry about rebalancing their portfolio when they add or withdraw money, or when markets move up and down. Asset allocation ETFs automatically rebalance themselves regularly to maintain their original target asset mix.

This article looks at BMO’s line-up of asset allocation ETFs, which include a conservative (ZCON: 40/60), balanced (ZBAL: 60/40), growth (ZGRO: 80/20), and balanced ESG (ZESG: 60/40) option.

These BMO asset allocation ETFs are available for self-directed investors to purchase through their online brokerage account. Notably, these ETFs can be traded commission-free through BMO InvestorLine and Wealthsimple Trade.

What’s inside BMO’s Asset Allocation ETFs?

Launched in February 2019, BMO’s core asset allocation ETFs are made up of seven underlying ETFs representing various asset classes and geographic regions.

ZMU – BMO Mid-Term US IG Corp Bond Hedged to CAD Index ETF

Altogether these seven ETFs represent nearly 5,000 individual stock and bond holdings from around the world.

In terms of geographic equity allocation, the BMO asset allocation ETFs hold 25% in Canadian stocks, 25% in international stocks, 40% to 41.25% in US stocks, and 8.75% to 10% in emerging market stocks.

BMO reviews their portfolios quarterly and will rebalance any fund that is more or less than 2.5% off from its target weight. In reality, these funds are rebalanced regularly with new cashflows from new investors.

BMO’s Balanced ESG ETF (ZESG) is made up of six underlying ETFs, including:

ESGY – BMO MSCI USA ESG Leaders Index ETF

ZGB – BMO Government Bond Index ETF

ESGA – BMO MSCI Canada ESG Leaders Index ETF

ESGE – BMO MSCI EAFE ESG Leaders Index ETF

ESGB – BMO ESG Corporate Bond Index ETF

ESGF – BMO ESG US Corporate Bond Hedged To CAD Index ETF

The management expense ratio for each of the BMO asset allocation ETFs is 0.20%. There is no duplication of fees or additional charges for the underlying ETFs. Continue Reading…

Many investors have been saying for years that rates can only go up from here, rates can only go one direction, rates will eventually go up. Will they? This begs a question I get from readers from time to time given bonds pay such lousy interest:

Why would anyone own bonds now?

Today’s post shares a few reasons to own bonds including some counter-arguments why I don’t own any – at least right now.

Why own bonds?

Personally, I believe the main role of fixed income in your portfolio is essentially safety– not the investment returns and certainly not the cash flow needs. In other words, if all else fails per se, if/when stocks crash, then bonds should historically speaking offer a flight to safety for preserving principal.

So, they are there for diversification purposes.

As Andrew Hallam, a Millionaire Teacherhas so kindly put it over the years: when stocks fall hard, bonds act like parachutes for your portfolio. Bonds might not always rise when the equity markets drop. But broad bond market indexes don’t crash like stocks do.

Is that enough to own bonds in your portfolio? Maybe.

Here are a few reasons to own bonds in no particular order.

1. Bonds as a hedge for stock market volatility.

Call them parachutes or anchors or use any other metaphor you wish but bonds tend to do their jobs when stock markets tank. More importantly maybe, they provide a psychological edge to avoid tinkering with your portfolio and selling any stocks/equities when stock markets correct.

Many investors, dare I say most investors (?), have a hard time with market volatility. I’m certainly not immune to it. The ups and downs, especially the big market downs, can be gut-wrenching to live through. Owning bonds in your portfolio can help bring the overall portfolio volatility down a few notches through prudent asset allocation. It is however not always necessary to own bonds.

When you own bonds, my experience has been for the last 20+ years you are trading away long-term, more positive, generous equity returns for accepting less risk and less long-term returns.

If you don’t want to take my word for it, check out this page courtesy of Vanguard when it comes to long-term returns. Check out the “worst year” stats as well.

Sure, a 40/60 stock/bond portfolio has hardly done poorly for the last century. But overall, you are absolutely giving up (historically speaking) returns on the table when you own more fixed income in your portfolio. Will the future be the same?

Personally, I’ve tried to learn to live with stocksas much as possible for as long as possible. Depending on your goals, taking into account long-term potential reward against short-term price fluctuations, some investors may not be comfortable with a 100% equity or near-equity portfolio. That’s A-OK. If that’s your case, some bonds in your asset accumulation years could be right for you.

2. Bonds can be used to rebalance your portfolio.

Even though I’m not a huge fan of bonds myself, this might be one of the most compelling reasons to own bonds at any age.

When the stock market sells off, that’s ideally the time you want to dive in and buy your stocks on sale. However, unless you are very comfortable with leveraged investing – you need money to buy such stocks on sale. That can come from cash savings for sure but for many investors, that can also come from bonds within your portfolio.

Mind you, some levels of diversification don’t work very well if you don’t have any asset allocation targets in mind. The process of rebalancing is a systematic way to buy low and sell high; sell your bonds when markets are tanking and sell-off some stocks when markets are euphoric.

In our portfolio, because we’ve largely learned to live with stocks, we tend to buy more stocks when they come on sale and/or we buy stocks periodically during the year to increase our equity holdings. More specifically, to help me gravitate away from my bias to Canadian dividend paying stocks for income we’re owning more low-cost U.S. ETFs for extra growth over time.

Instead of selling bonds to buy our stocks, I use cash savings. I tend to save up cash during the year and make a few lump-sum stock or equity ETF purchases instead.

I will continue to use cash savings to make more equity purchases as I enter semi-retirement.

Last month, I had the privilege of meeting legendary investor Larry Hite.

Larry was born into a lower middle-class family, had a major learning disability, did poorly in school, and was completely blind in one eye and half blind in the other. In his own words, “I was not handsome. I was not athletic. Whatever I did, I sucked at it badly.”

In 1981, after dabbling as a music promoter, actor, and screenwriter, Hite founded Mint Investments. Mint was a true pioneer, eschewing human judgment and instead basing its investment decisions on a purely systematic, rules-based approach rooted in statistical analysis.

By 1988, Mint registered average annual compounded returns of over 30%. In its best year, Mint registered a gain of 60% (1987, the year of the stock market crash), and in its worst year, it produced a gain of 13%. By 1990, Mint was the biggest hedge fund in the world, with a record-breaking $1 billion under management.

When it awarded Larry the Lifetime Achievement Award, Hedge Fund Magazine wrote:

“Larry Hite has dedicated the last 30 years of his life to the pursuit of robust statistical programs and systems capable of generating consistent, attractive risk/reward relationships across a broad spectrum of markets and environments and has inspired a generation of commodity trading advisers and systematic hedge fund managers.”

Although Hite began his investing career in the early 1980s, his philosophy of markets and approach to investing are remarkably similar to our own, which are summarized below.

Failure: A Foundation for Success

Hite maintains that his early failures were instrumental in his eventual success. He believes that accepting that failure is sometimes inevitable led him to develop an investment strategy that would limit losses.

In his book, The Rule, he wrote:

“I believe the success I’ve had arrived because I always expected to fail big. Solution? I engineered my actions so that a failure could not kill me. I won because I expected to lose. Failure became my advantage. Once you understand your potential for failure – that is, there are times you can’t win – you know when to fold your cards and move on to the next. You will do this more quickly than others who stay in the game too long, hanging on and hoping that their losing bet will turn around.”

It’s not all about Being Right

Many investors focus on being right as much as possible – on maximizing their ratio of winning vs. losing investments. On its face, this seems like a good idea – all else being equal, if you win more than 50% of the time, then over time you will make money.

Hite takes a different approach. Whereas he has no issue with trying to be right as often as possible, he is far more focused on maximizing the average magnitude of his winning positions relative to that of his unsuccessful ones, asserting that:

“Becoming wealthy and successful isn’t simply about being right all the time. It’s about how much you win when you are right as well as how much you lose when you are wrong…. The Mint trading system did not prioritize being right all the time. We prioritized not losing a lot when we lost but winning big when we won. But as a result, we were frequently wrong. We understood and expected this and taught our clients the wisdom too.”

Risk: A No Fooling Around game

Hite places a greater emphasis on risk management than on generating profits, claiming that mistakes regarding risk can lead to catastrophic results. He asserts that, “Risk is a no fooling around game; it does not allow for mistakes. If you do not manage the risk, eventually it will carry you out.”

His approach to investing clearly reflects his respect for risk. Specifically, Hite divulges that “We approach markets backwards. The first thing we ask is not what we can make, but how much we can lose. We play a defensive game.”

One of my favorite anecdotes regarding risk is Hite’s reflection on a conversation he had with one of the world’s largest coffee traders, who asked, “Larry, how can you know more about coffee than me? I am the largest trader in the world. I know where the boats are; I know the ministers.” Larry responded, “You are right. I don’t know anything about coffee. In fact, I don’t even drink it.” The coffee mogul then inquired, “How do you trade it then?”, to which Larry answered, “I just look at the risk.”

Five years later, Larry heard that this magnate lost $100 million in the coffee market. Upon reflection, Hite states, “You know something? He does know more about coffee than I do. But the point is, he didn’t look at the risk.”

Larry Hite

Market Predictions, Storytelling, & Good Copywriters

Larry is skeptical that anyone can predict markets. He in no way bases his approach to investing on making predictions, which he believes is an exercise in futility. In his own words:

“I respect the sheer intelligence and devotion of economists who have attempted to develop a unifying theory of market dynamics. But I don’t believe any such theory will hold up to scrutiny in the real world of money on the line. When you start believing you have remarkable market predicting powers, you get into trouble every single time.”

Hite is also critical of Wall Street research reports, claiming that they possess little investment value and are designed to exploit people’s natural tendencies to listen to entertaining narratives, stating:

“Stories began at the dawn of human society to entertain and instruct the next generation. We are wired to learn from well told stories. And unfortunately, Wall Street preys off our basic human weakness to want stories.”

In his typically blunt and straightforward manner, he adds, “When you start following slick reports filled with predictions, you’re just finding out who has good copywriters.”

A Computer can’t get up on the wrong side of the bed in the morning

Larry was a pioneer in his exclusive reliance on a data-driven, systematic approach, using statistical analysis of historical data to develop trading rules, which are the basis of his investment decisions. When he launched Mint Investments in 1981, his goal was “to create a scientific trading system that would remove human emotion from buying and selling decisions and rely instead on a purely statistical approach built on pre-set rules.” Continue Reading…

Call me a nerd, but I love studying retirement statistics (for the record, I prefer to consider myself curious). When something as dramatic as COVID comes along, it really makes the numbers interesting.

If you’re curious like me, you’ll enjoy today’s post. A compilation of some fascinating retirement statistics I recently came across, including some graphs for those of you who prefer to view the charts.

If you’re interested in how you compare to “average,” you’ll also find today’s post of interest. Wondering what impact COVID has had on retirement confidence? We’ve got that covered, as well.

Curiosity-seekers, unite. This one is for you …

What’s retirement really like? What impact has COVID had? Today, a look at some fascinating retirement statistics.

Fascinating Retirement Statistics

A while back, as I was doing some research for my post titled The Mad Retirement Rush of 2020, I came across an article with some interesting retirement statistics and saved the link into a draft post (I do that a lot, with over 100 draft posts currently holding ideas for future posts). I wanted to do further research on retirement statistics to see how many I could compile for a dedicated post on the topic.

Today, I’m pleased to publish the resulting work and share what I’ve found during my research. A variety of fascinating retirement statistics, dedicated to all of the fellow retirement nerds in the house.

73% of retirees say their retirement was a “full-time stop,” with only 19% experiencing a gradual transition (e.g., fewer hours). Among those still working, half expect a gradual transition. Related, only 30% of retirees work for money in retirement, whereas 72% of workers expect to work for some pay in retirement. (Source: 2021 EBRI Retirement Confidence Survey)

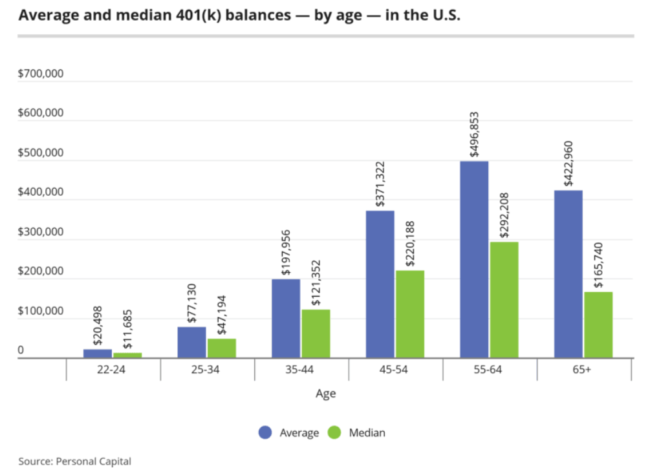

The average US household had $255,000 in their retirement accounts in 2019, a 5% increase from 2016 (Source: MagnifyMoney)

Among those with 401(k), the average balance by age is shown below: (source, Personal Capital as cited in MagnifyMoney)

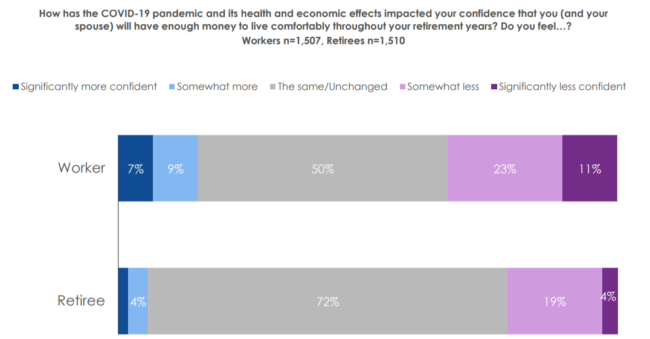

COVID’s Impact on Retirement Confidence

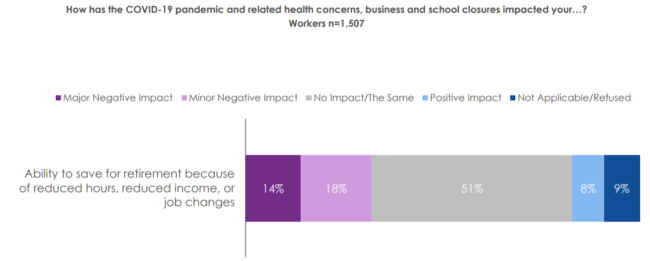

While the majority of workers are still confident of their ability to retire, 34% of workers are less confident in their ability to live comfortably in retirement than they were pre-COVID.

COVID has caused 1 in 4 workers to adjust their expected retirement date, with 17% now planning to retire later and 6% who plan to retire earlier.

32% of workers say COVID has negatively impacted their ability to save for retirement.

30% of Americans with retirement accounts reported making withdrawals from them in the first two months of the COVID pandemic. The average withdrawal was $6,757 (Source: Investment News)

Baby Boomer Statistics

Every day, 10,000 Baby Boomers turn 65 years old. (Source: Legaljobs.com)

8 in 10 retirees report that their overall lifestyle is as expected or better. Only 26% of retirees report spending is higher than expected. (Source: 2021 EBRI Retirement Confidence Survey)

Baby Boomer retirements increased significantly in 2020 vs. prior years. By September 2020, 40% of Baby Boomers were retired. (Source: Pew Research) Continue Reading…

Proactive Business Owners Can Manage Corporate Investments and Income for Optimal Tax Efficiency

As a small business owner, you no doubt have active interests in your bottom line. That’s why it’s worth knowing about some recent changes to the tax treatments on corporate passive income.

For those currently creating passive income through corporate investments, we’ll describe how this income might impact your small business tax planning, and offer some corporate tax strategies for keeping more of that money in your coffers.

Even if you are not currently generating corporate passive income, some of these same tax strategies remain sound. After all, smart tax strategies and sensible corporate tax planning is perennially popular. At the end of a busy work day, the more of any sort of income you get to keep, the better off you and your small business will be.

The Highlights: What has Changed about Corporate Passive Income and How Does It Impact You?

How have corporate passive income rules recently changed?

How do the changes impact your corporate passive income?

These changes brought good news and bad. Under the broader definitions for passive income, you may exceed the passive income limits to qualify for the coveted small business deduction (SBD). Corporate tax strategies that may have worked for you in the past may no longer be ideal for optimal tax integration. But with the tax rate changes, some applicable corporate tax strategies are even more powerful.

That’s the broad sweep. Now let’s take a closer look.

The Details: Small Business Tax Planning and Passive Corporate Income Changes

Small business owners typically manage two interests in their owner/individual roles. Rather than earning your keep by working for someone else, you create corporate wealth. You then decumulate that wealth by transitioning it from your corporation to yourself and your family. Once the dust settles, the goal is to retain as much wealth as possible by being deliberate and tax-efficient throughout the process. Broadly speaking, there are a couple of ways to take wealth out of your business for personal use:

If you take your annual CCPC income as a salary:

Your corporation takes it as a deduction, so no corporate tax is due on the income.

Instead, you pay personal tax on the income at your graduated personal tax rate.

If you take your after-tax CCPC income as a dividend:

Initially, your annual CCPC income will be subject to corporate tax.

That year or in the future, you can distribute the after-tax income as a dividend to yourself.

In the year you receive the dividend, you’ll pay personal tax on the distribution at your graduated marginal tax rates.

Which is better?

As you might expect, it all depends, and typically requires you to crunch your particular numbers to see how they compare. By design, how you take the money is supposed to end up being a tax-planning wash … at least as far as the CRA is concerned. However, the ability to tax-defer dividends to future years has often been beneficial as part of overall corporate tax-planning.

What’s changed?

The concern is, business owners in general, and small business owners in particular, may have had an unfair advantage over individual taxpayers. By deferring a salary or dividend payments while building up wealth within your corporation, you also can defer paying annual personal taxes, which are typically at higher rates … especially if you qualified for Small Business Deferral (SBD) rates. Continue Reading…

I’m on record to say that the vast majority of self-directed investors should simply use a single asset allocation ETF to build their investment portfolios.

I’m on record to say that the vast majority of self-directed investors should simply use a single asset allocation ETF to build their investment portfolios.